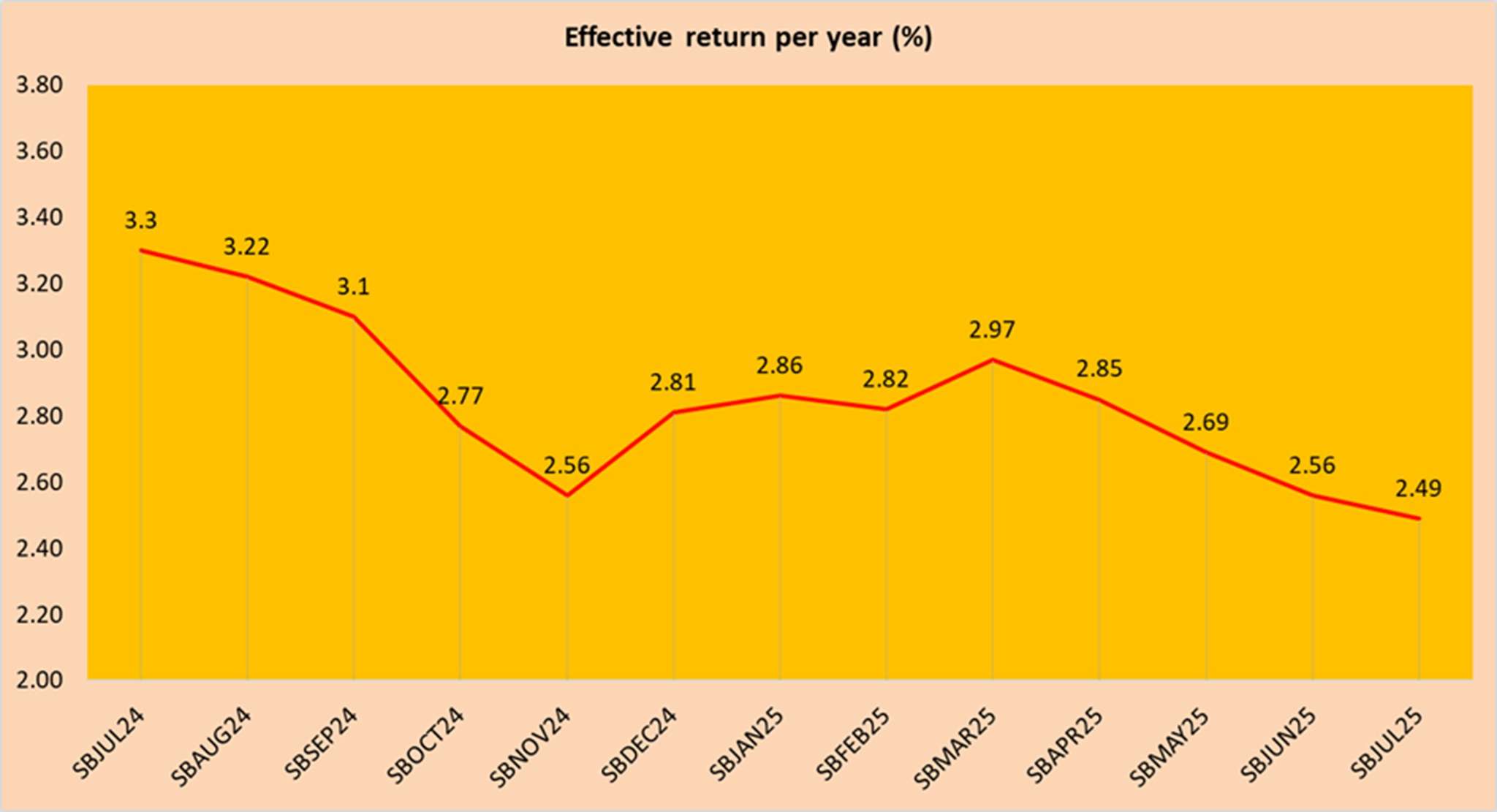

The effective interest rate for SSB SBJUL25 GX25070Z is 2.49% if you held it for 10 years. The interest rates for this month’s issue of the SSB (Singapore Savings Bond) continue to decline further by 0.07% from 2.56% offered by SBJUN25. If you decided to sell off it after holding it for 1 year, the return per year is 2.06%.

What are Singapore Savings Bonds? Singapore Savings Bonds are a type of government bond issued by the Monetary Authority of Singapore that offers individuals a safe and flexible way to save money. The “step up” feature of the SSB facilitates long term investment which means the return increases the longer you hold them for.

These bonds have a low minimum investment amount, starting at just $500, and offer a higher interest rate than traditional savings accounts. Investors can purchase Singapore Savings Bonds directly from the government and hold them for up to 10 years, earning regular interest payments along the way.

Why should you buy Singapore Savings Bonds? Singapore Savings Bonds are low risk investments, thus making them a popular investment option among risk-averse investors looking to grow their savings over time. The return increases as you hold them longer. The limit an individual can purchase is S$200,000 inclusive of both cash and SRS.

Singapore Savings Bonds SSB Calculator

Monetary Authority of Singapore (MAS) had come up with a Singapore Savings Bonds Calculator which you can use to calculate how much interest you would earn if you held Singapore Savings Bonds for 10 years.

Let us use an investment of S$10,000 as an example. If you purchase SSB Singapore (SSB SBJUL25 GX25070Z) and held it for 10 years, you will receive a total earning of S$2,517.00. Based on the SSB Calculator, you will receive an estimate of S$206 per year until maturity in July 2035 depending on the interest rate for that year.

Below is the interest per year for SSB SBJUL25 GX25070Z.

| Year from issue date | Interest % | Average return per year %* |

| 1 | 2.06 | 2.06 |

| 2 | 2.06 | 2.06 |

| 3 | 2.06 | 2.06 |

| 4 | 2.22 | 2.10 |

| 5 | 2.37 | 2.15 |

| 6 | 2.50 | 2.21 |

| 7 | 2.70 | 2.27 |

| 8 | 2.90 | 2.34 |

| 9 | 3.08 | 2.42 |

| 10 | 3.22 | 2.49 |

*At the end of each year, on a compounded basis.

How to Buy Singapore Savings Bonds

To buy Singapore Savings Bonds, you first need to have an individual CDP account with the Central Depository (CDP). You can apply for the bonds through ATMs of participating banks, internet banking services, or through the DBS/POSB, OCBC, or UOB websites. Simply log in to your bank account and follow the instructions to subscribe to the bonds.

The minimum amount you can invest in Singapore Savings Bonds is $500, and you can apply for up to $200,000 worth of bonds in each issue. The bonds are issued monthly, and the interest rates are adjusted every year. Once you have successfully subscribed to the bonds, you will receive your interest payments twice a year, with the principal amount being repaid at the end of the bond’s 10-year tenure.

For more details, refer to How to Buy.

How to Sell Singapore Savings Bonds

To sell Singapore Savings Bonds, you can do so through the ATMs of participating banks, such as DBS/POSB, OCBC, and UOB. Simply log in to your bank account through the ATM and follow the instructions to sell your bonds.

You can also sell your Singapore Savings Bonds through SRS Operator if you hold them under the Supplementary Retirement Scheme.

For more details, refer to How to Redeem.

How To Track Singapore Savings Bonds?

To track your Singapore Savings Bonds, you can visit the official website of the Monetary Authority of Singapore (MAS) where they provide regular updates on the issuance and performance of the bonds.

![]() I use Stocks Café to track my SSB Singapore purchases. If you like to know more about Stocks Cafe, please read up my previous review of Stocks Cafe.

I use Stocks Café to track my SSB Singapore purchases. If you like to know more about Stocks Cafe, please read up my previous review of Stocks Cafe.

Comparing SSB SBJUL25 GX25070Z with Best Fixed Deposit in June 2025

The best fixed deposit in June 2025 is offered by DBS Bank. DBS Bank is offering the highest fixed deposit interest rate at 2.45% per annum for a 12-months tenure. If you sell off SBJUL25 after holding it for 1 year, the return per year is 2.06%. Thus, DBS Bank 12-month fixed deposit is the clear winner here.

Tenure: 6 months

Interest Rate: 2.15% p.a.

Minimum Amount: S$1,000 to $$19,999

Tenure: 7 months

Interest Rate: 2.30% p.a.

Minimum Amount: S$1,000 to $$19,999

Tenure: 8 months or 9 months

Interest Rate: 2.35% p.a.

Minimum Amount: S$1,000 to $$19,999

Tenure: 10 months or 11 months

Interest Rate: 2.40% p.a.

Minimum Amount: S$1,000 to $$19,999

Tenure: 12 months

Interest Rate: 2.45% p.a.

Minimum Amount: S$1,000 to $$19,999

Comparing SSB SBJUL25 GX25070Z with SGS T Bill

The cut off yield of the latest issue of SGS T Bill (BS25111T 6-Month T-bill) sunk to 2.05% per annum. The difference in return offered by SBJUL25 and BS25111T 6-month T-bill is not significant.

As such, I would rather park my money with SBJUL25 given the 1-year return is 0.01% higher than BS25111T 6-month T-bill.

Comparing SSB SBJUL25 GX25070Z with GXS Savings Account

With effect from 30th May 2025, GXS will be adjusting their GXS Savings Account rates. The interest rate for Main Account will be adjusted from 2.08% p.a. to 1.68% per annum. The interest rate for Saving Pockets will be adjusted from 2.38% p.a. to 1.98% per annum.

This makes SBJUL25 more attractive than GXS Savings Account because if you sell off the current issue of Singapore Savings Bonds after 1 year, you receive 2.06% per annum. The return from Singapore Savings Bond is higher than the return of 1.98% per annum offered by GXS Digital Bank.

Comparing SSB SBJUL25 GX25070Z with UOB Stash Savings Account

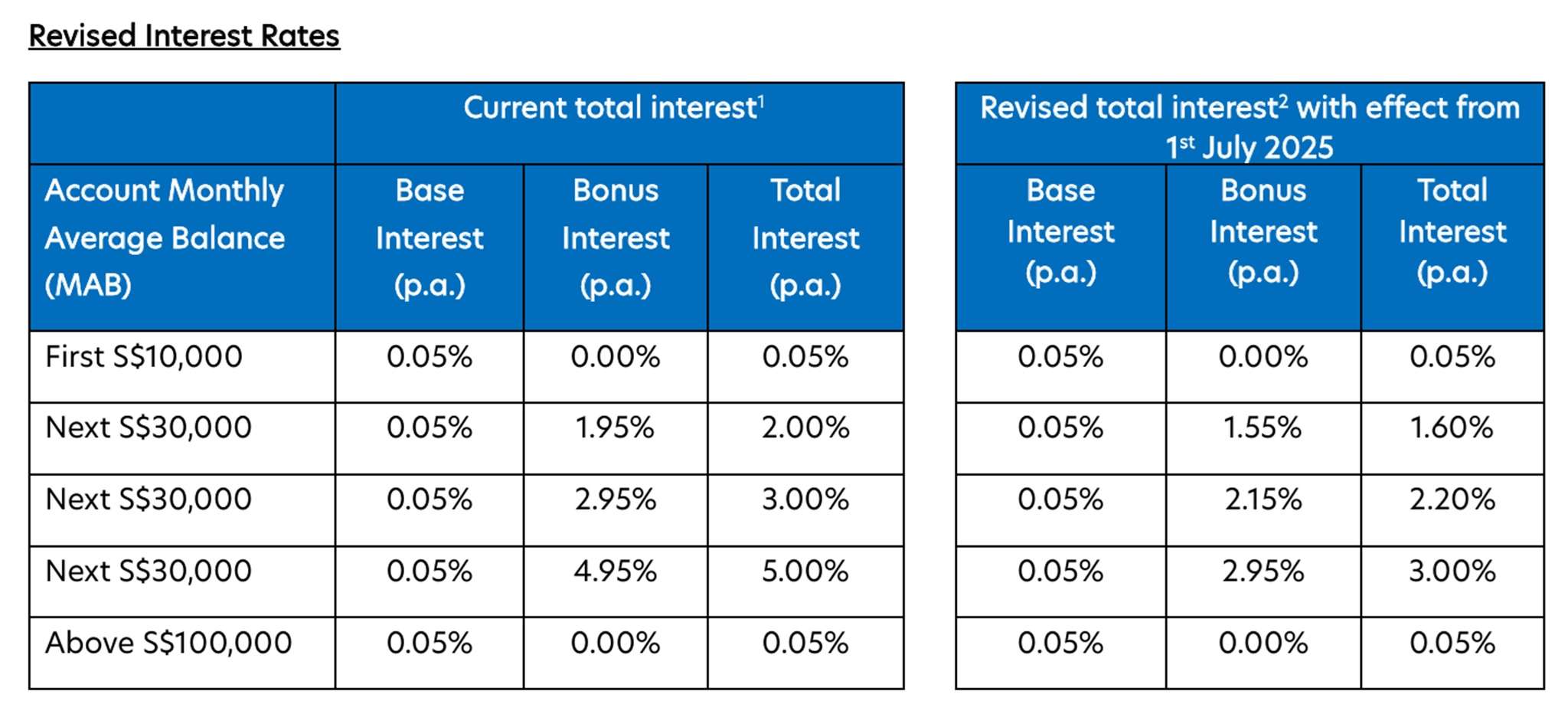

As shared earlier, UOB Stash will be revising their interest rates effective from 1st July 2025. With the revised interest rates, you can earn up to S$2,040 interest a year with a deposit balance of S$100,000 in your UOB Stash Account by simply maintaining or increasing your Monthly Average Balance (MAB) each month.

Based on the revised rates, UOB Stash Account interest rates work out to be estimated 2.04% per annum.

The return from SBJUL25 GX25070Z is also higher than UOB Stash Account!

Will I Consider SBJUL25 GX25070Z?

Based on the above comparisons against other financial instruments, this month’s issue of Singapore Savings Bond (SBJUL GX25070Z) is worth considering. The returns are slightly higher than T Bills and high yielding savings account such as UOB Stash.

Having said that, the returns still fail to beat DBS Bank 12-month fixed deposit rate at 2.45% per annum. If you are ok to lock down your cash for 12-months, go for DBS Bank 12-month fixed deposit. Otherwise, opt for SBJUL25 GX25070Z as you can redeem Singapore Savings Bonds anytime!

Always look for the best place to park your money!