How do we Retire Early in Singapore? On 4th March 2024, Minister for Manpower Tan See Leng announced that Singapore retirement age will be raised from the current 63 to 64 on 1st July 2026. The last time the retirement age was raised was in the year 2022 from 62 to the current 63.

According to Wikipedia,

Retirement is the withdrawal from one’s position or occupation or from one’s active working life.

With the Ministry of Manpower raising the retirement age to 64, it does not mean you have to work until the minimum age. This is where FIRE comes into play. FIRE is short for Financial Independence, Retire Early. For myself, FIRE is a major life goal as I wanted the luxury to be able to choose whether to work before the statutory retirement age.

To be able to retire early, it is important to

- Start planning early, be prudent in your savings and accumulate a larger nest egg for your retirement years.

- Estimate your monthly expenses during your retirement years. (Need versus Wants).

- Build multiple sources of passive income to mitigate against longevity and inflation.

How am I planning towards retiring early? Below are some of the ways that I have started years ago towards planning for my early retirement.

Start Planning Early – Open a Supplementary Retirement Scheme (SRS) Account (Minimum Age of 18)

The voluntary Supplementary Retirement Scheme (SRS) was introduced by the Singapore government in the year 2001 with the purpose of helping Singaporeans in retirement planning.

You may make penalty-free withdrawals from your SRS account over 10 years starting from the date of your first penalty-free withdrawal. When you make your first contribution to the SRS account, the retirement age where you can start withdrawal will be locked down. Any subsequent change in the statutory retirement age (e.g. up to age 65) will not affect you. For example, I can start making penalty-free withdrawals from my SRS account at the age of 62.

In my opinion, S$400,000 is the optimal amount of money you should accumulate in your SRS account for retirement as you will be able to withdraw S$40,000 each year for 10 years. During the 10-year window where you start withdrawing the money, only 50% of your withdrawals are taxable. This means that only $20,000 is subject to tax.

Estimate your monthly expenses – Need versus Wants

My current monthly expenses worked out to be 8 to 9K per month. This is because I am still servicing big items such as my car auto loan, housing mortgage etc.

I foresee that I may not drive after retirement. As such, I estimate that I need 3K per month for basic necessities.

Build Passive Income #1 – Singapore Savings Bonds (SSB)

To mitigate against longevity and inflation, we need to build multiple sources of passive income that will last during our retirement years. As we get older, we should consider opting for less risky investments such as Singapore Savings Bonds because there is very little leeway for us to earn back the capital if we make any mistakes in our investments.

Singapore Savings Bonds are fully backed by the Singapore Government. You can always get your investment amount back in full with no capital loss. The bonds are held for 10 years. Interest rate increases over time and you can exit your investment by redeeming the bonds in any given month. There are no penalties (except for the S$2 transaction fee).

As you can see from my stock portfolio, Singapore Savings Bonds make up 17.15% of my investment portfolio.

This month’s issue of Singapore Savings Bonds (SBAPR24) gives you a decent effective return of 3.04% p.a. over 10 years.

Build Passive Income #2 – Singapore Treasury Bills (T-Bills)

Another popular investment among Singaporeans is the Singapore Treasury Bills (T-Bills). Treasury bills (T-bills) are short-term Singapore Government Securities (SGS). They are issued at a discount to their face value. Investors receive the full face value at maturity.

The Singapore Government issues 6-month and 1-year T-bills.

As you can see from the chart that I plotted above, the highest cut-off yield ever offered was 4.2% (BS23100Z). In recent months, the cut off yield hovers between 3.70% to 4.00%.

Build Passive Income #3 – Fixed Deposits

Fixed deposits have been around for the longest time. They are a great way to save for retirement because the bank locks your money away and you cannot spend them. The interest is also guaranteed upon maturity.

By continuing to renew the principal and interest upon maturity, you should be able to stash up a hefty lump sum when you reach retirement age.

Having said that, please take note that money in fixed deposits are insured by the Singapore Deposit Insurance Corporation Limited (SDIC), up to S$75,000. Thus, do ensure you do your fixed deposit placements with a reputable bank.

I have done several fixed deposit placements with my favourite CIMB Bank for the below reasons.

- High interest rate

- Short tenor period

- Easy placement done via their mobile application (CIMB Clicks)

- Flexibility of auto renewal of principle and interest in fixed deposits or withdraw the principle and interest back to savings account upon maturity

Below is the fixed deposit interest rates for CIMB Bank which I think is pretty attractive.

| Tenure | PERSONAL BANKING ONLINE PROMO INTEREST RATE (%P.A.) S$10,000 AND ABOVE |

PREFERRED BANKING ONLINE PROMO INTEREST RATE (%P.A.) S$10,000 AND ABOVE |

| 3 months | 3.30 | 3.35 |

| 6 months | 3.35 | 3.40 |

| 9 months | 3.15 | 3.20 |

| 12 months | 3.05 | 3.10 |

Build Passive Income #4 – Invest in Dividend Paying Stocks

Most retired folks live off their savings that they have accumulated during their working days until their retirement savings get depleted. Since retirees are no longer paid a salary, they have no cash flowing in. Daily expenses continue to deplete their savings.

One of the ways to still have cash flowing into your bank account after retirement is to invest in dividend paying stocks. That is exactly what I am doing now. I am building a dividend paying stock portfolio that pays me dividends even after I retire. This is not difficult in Singapore as there are many quality REITs listed on the Singapore Stock Exchange (SGX).

If you want to know what are the dividend paying stocks, you can start off with looking through the list of REITs that pay dividends.

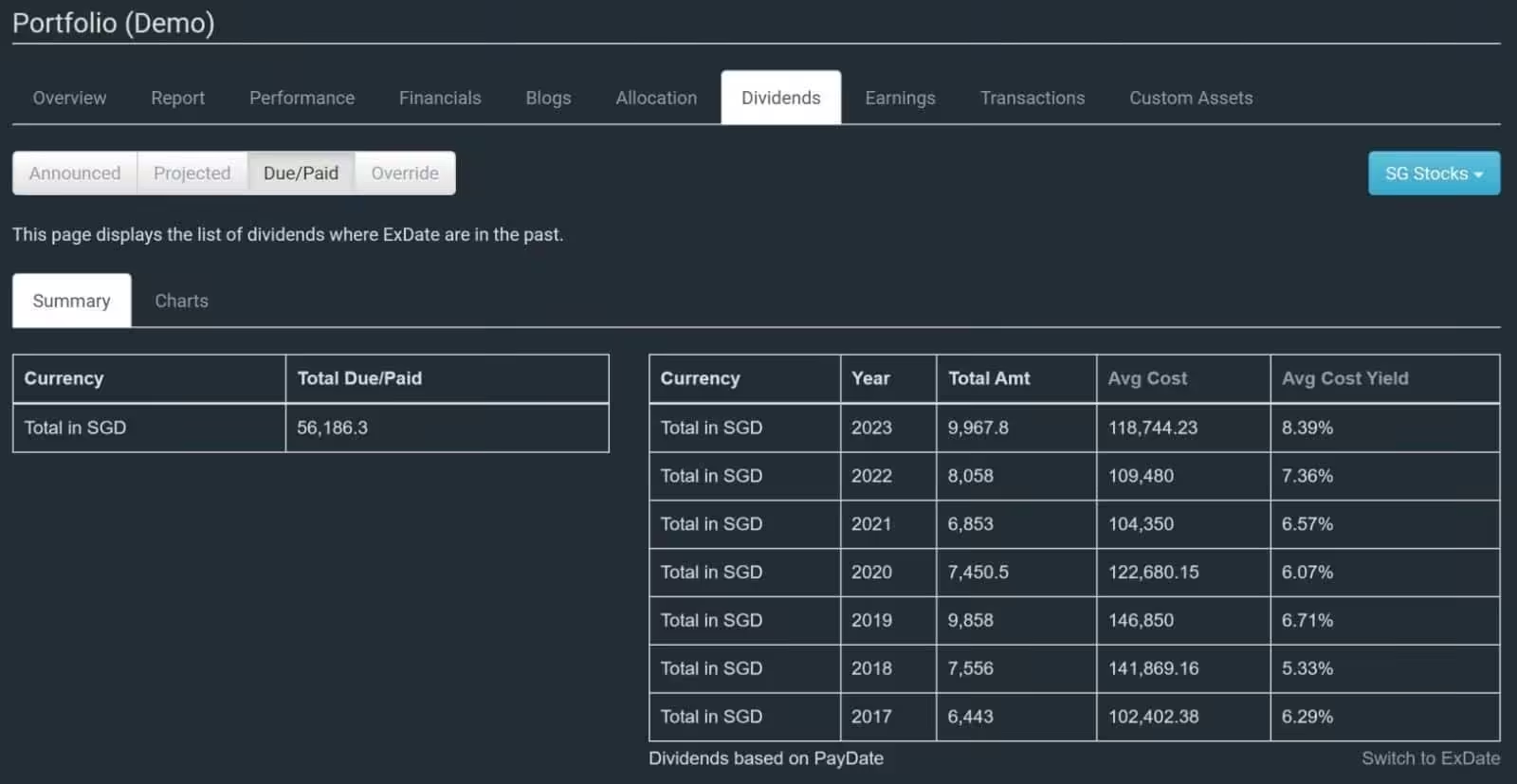

I also want to share that I use Stocks Café to keep track of the total value worth of my stocks. Stocks Café is my preferred tool for managing my stock portfolio. It is packed with tonnes of intelligent features such as portfolio monitoring and reporting, dividend tracking, stock screening. All these features are automated which means no manual entry is required.

Retire Early in Singapore?

Retire Early in Singapore is possible if you have been consistently practicing all the above methods. To be honest, I am least worried at the Singapore government raising the retirement age because I would have stash sufficient money and built multiple streams of passive income that allows me to retire early in Singapore.

Like I said, FIRE is not about stopping work but having the luxury to be able to choose whether to work before the statutory retirement age!