On 6th May 2024, Paragon REIT released their 1QFY2024 business updates. Year to Date, Paragon REIT’s gross revenue grew 3% year-on-year to S$73.8 million from S$72.0 million. In terms of tenant sales, Singapore grew 1.4% year-on-year to S$236.9 million while sales for the Australia market fell 0.3% year-on-year to A$238.5 million.

As of 1QFY2024, Paragon REIT’s portfolio remains unchanged with 3 retail malls in Singapore and 2 retail malls in Australia. In Singapore, the malls are Paragon, The Clementi Mall and The Rail Mall. These malls since my school days enjoy good visitor traffic throughout the day.

In Australia, the malls are Westfield Marion SA and Figtree Grove NSW.

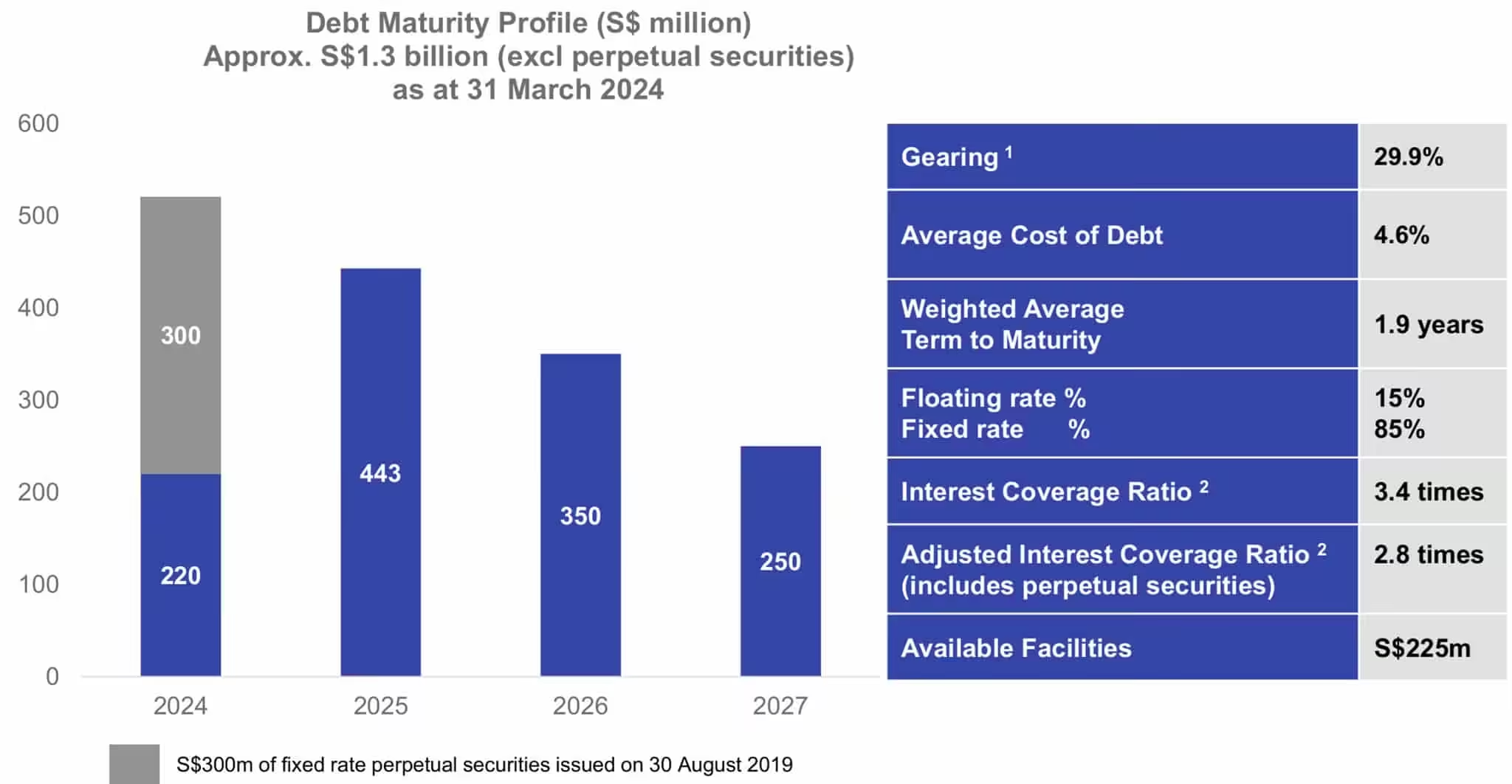

Debt

Paragon REIT’s debt level remains extremely low with gearing at 29.9%. 85% of Paragon REIT’s debt is hedged at fixed rates.

Paragon REIT’s Weighted Average Term to Maturity is short at 1.9 years. Weighted Average Term to Maturity, is a measure used to assess the overall maturity of a portfolio of debt securities. A longer Weighted Average Term to Maturity implies somewhat greater interest rate and credit risk compared to portfolios with shorter Weighted Average Term to Maturity.

Occupancy

Paragon REIT’s overall portfolio occupancy remains high at 98.1%. As you can see above, all the malls in Singapore (Paragon, The Clementi Mall, The Rail Mall) achieved 100% occupancy.

Weight Average Lease Expiry (WALE) by Net Lettable Area stood at 5 years. WALE represents the average remaining lease term across all tenants in a property or a group of properties. Paragon REIT’s long WALE of 5 years indicates lower vacancy risk.

Paragon REIT’s Current Dividend Yield

What is Paragon REIT’s share price and dividend yield? Based on Paragon REIT’s share price of S$0.84 and FY2023 full year distribution of 5.02 cents, the current dividend yield is 5.98%.

Summary of Paragon REIT 1QFY2024 Business Updates

As usual, I will summarize the pros and cons based on Paragon REIT’s 1Q FY2024 business updates.

If you are going to buy Paragon REIT, the pros are:

- Gross revenue grew 3% year-on-year to S$73.8 million from S$72.0 million.

- Extremely low gearing at 29.9%.

- High portfolio occupancy of 98.1%.

- Paragon, The Clementi Mall, The Rail Mall achieved 100% occupancy.

- Lower vacancy risk due to long WALE of 5 years.

- Current dividend yield is 5.98%.

The cons are:

- Underperforming Australia assets (Westfield Marion SA and Figtree Grove NSW) continue to be a drag.