Starhill Global REIT has been in my watch list for a few months. The stock price fell as low as $0.73 when there was a rental dispute with Toshin in Ngee Ann City property. I did not rush in to buy as at that point of time, I didn’t do any analysis on Starhill Global REIT. Buying without doing my homework is purely speculation. Today, the stock price has went up to $0.79.

I managed to find some time among my busy work schedule and here is my research of Starhill Global REIT.

Portfolio

Starhill Global REIT owns mainly retail assets in Singapore (Wisma Atria, Ngee Ann City), Australia (Myer Centre, David Jones, Plaza Arcade), China (Renhe Spring Zongbei), Malaysia (Starhill Gallery, Lot 10), Japan (Daikanyama, Ebisu Fort, Harajyuku Secondo, Nakameguro Place).

Occupancy

Occupancy is not an issue for Starhill Global REIT. Given the current economic down cycle, Starhill Global REIT is able to maintain a high occupany of 95.6%.

Recently, Starhill Global REIT secures 5.5% rent increase for the Master Lease with Toshin In Ngee Ann City Property. Japan Food Town which occupies 20,000 square feet has also recently opened at Wisma Atria.

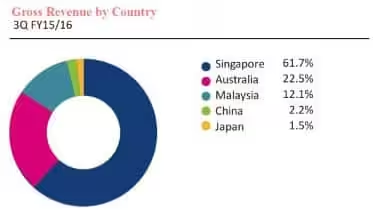

Gross Revenue

Gross Revenue has been increasing year on year for Starhill Global REIT.

Singapore, Australia, Malaysia, China and Japan contributes 61.7%, 22.5%, 12.1%, 2.2% and 1.5% of the gross revenue respectively. As you can see, asset from Singapore (Ngee Ann City, Wisma Atria) are the largest revenue contributor.

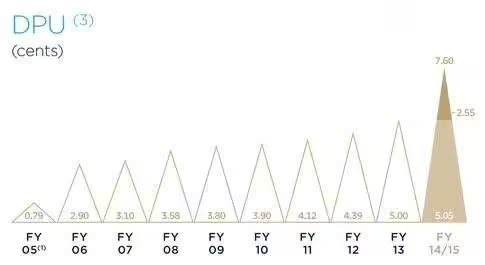

Distribution Per Unit

Distribution Per Unit (DPU) has been increasing year on year. In FY14/15, Starhill Global REIT achieves an all time high DPU of 7.60 cents. This is based on 18th months. Starhill Global REIT decides to change its financial year from 31 December to 30 June, thus DPU is actually 5.11 cents.

Dividend Yield

Based on the closing price on 30 June 2015 of 88 cents, the dividend yield for Starhill Global REIT will translate to (5.11/88) x 100 = 5.82%.

If we based on 22nd July 2016 closing price of 79 cents, this translates to a dividend yield of (5.11/79) x 100 = 6.47%.

As an income investor, any REIT or stock that yields above 5% is attractive for me. A high dividend yield could mean falling stock prices and low dividend yield could mean the REIT has grown expensive. Starhill Global REIT’s dividend yield of 6.47% strikes a balance between a high yield and low yield. However, we should not purely look at the dividend yield when selecting a REIT.

The annualized dividend will actually be known when Starhill Global REIT announce its 4th quarter and full year financial results on 29th July 2016.

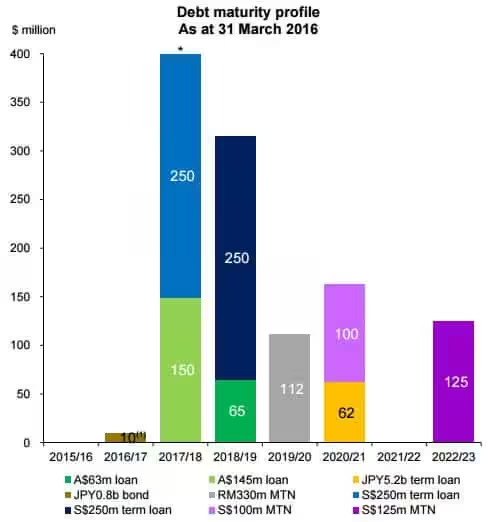

Debt

Gearing ratio stood at 35.4%. The weighted average debt to maturity is 3.3 years. Something I do not like is that only 73% of its assets are unencumbered.

There is little debt expiring in FY16/17 but I noticed majority of its debt are expiring in FY17/18.

The Management

Francis Yeoh Sock Ping is executive chairman of Starhill Global REIT. He is a Malaysian businessman and eldest son of billionaire Yeoh Tiong Lay. Mr Francis Yeoh is also the managing director of YTL Corp, one of the largest conglomerates in Malaysia.

Mr Ho Sing is the Chief Executive Officer of Starhill Global REIT. He is said to be the brother of Temasek Chief Executive Ms Ho Ching.

Cheap to Buy Now?

After some research, I came across an article where Gordon Growth Model was used to evaluate if Starhill Global REIT is cheap to buy now.

The Gordon growth model is used to determine the intrinsic value of a stock based on a future series of dividends that grow at a constant rate. – Investopedia

The Gordon Formula is as such:

Share Price = Expected Dividend Per Share One Year From Now / (Discount Rate – Dividend Growth Rate)

Using a discount rate of 8.48% for Starhill Global REIT.

0.79 = 0.0539 / (0.0848 – Dividend Growth Rate)

Dividend Growth Rate = 1.66%

The dividend is expected to grow at 1.66%. annually. I am expecting Starhill Global REIT to grow its dividend at a higher rate than 1.66 because based on historically DPU trend, the growth is at least 2.2%.

Thus, my personal conclusion is Starhill Global REIT is cheap to buy now at $0.79.

Any Alternatives?

Starhill Global REIT owns Ngee Ann City and Wisma Atria whereby both properties are located in Orchard Road area. If I were to do a comparison, Paragon Shopping Center seems to be the closest match and thus I compare the dividend yield of Starhill Global REIT with SPH REIT which owns Paragon Shopping Center.

Based on 4Q2015, the annualised dividend yield for SPH REIT is 5.70%.

My Conclusion

Within my limited knowledge and with all factors considered, I decided it is a buy call for Starhill Global REIT.

Are you vested?

How did you get the discount rate of 8.48%

Hi Dito, you can find that from fools.sg