![]()

CapitaLand Commercial Trust catches my eye when I was researching on REITs that own car parks in their portfolio. If you didn’t know, Golden Shoe Car Park is one of the assets in CapitaLand Commercial Trust portfolio. But in general, CapitaLand Commercial Trust is similar to Keppel REIT which consists of mainly Grade A office assets.

Golden Shoe Car Park is undergoing a redevelopment which is due to complete in 1H2021. The car park will be redevelop into a commercial development in Raffles Place.

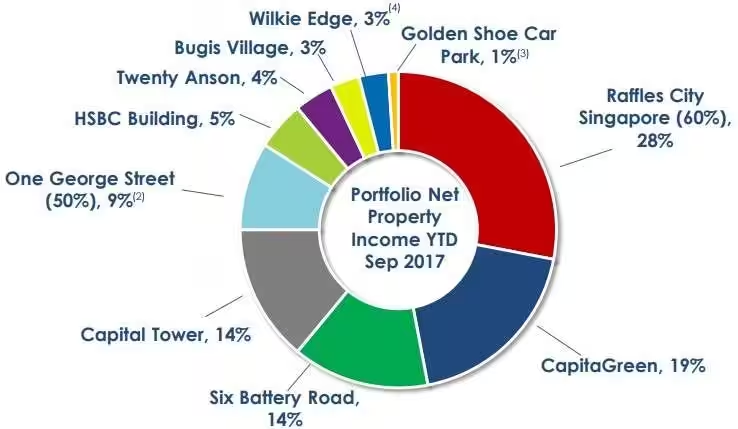

Portfolio

CapitaLand Commercial Trust has the following properties in its portfolio.

- Capital Tower

- CapitaGreen

- Six Battery Road

- One George Street

- Raffles City Singapore

- Twenty Anson

- HSBC Building

- Wilkie Edge

- Bugis Village

- Golden Shoe Car Park

Do take note that CapitaLand Commercial Trust has fully divested Wilkie Edge as of 11 September 2017.

It is also interesting to know that CapitaLand Commercial Trust has a 17.7% stake in MRCB-Quill REIT, a commercial REIT listed on Bursa Malaysia Securities Berhad.

Occupancy

Based on 3Q2017 financial results, CapitaLand Commercial Trust occupancy rate stood at 98.5%. This is lower than the occupancy rate for Keppel REIT which stood at 99.6%.

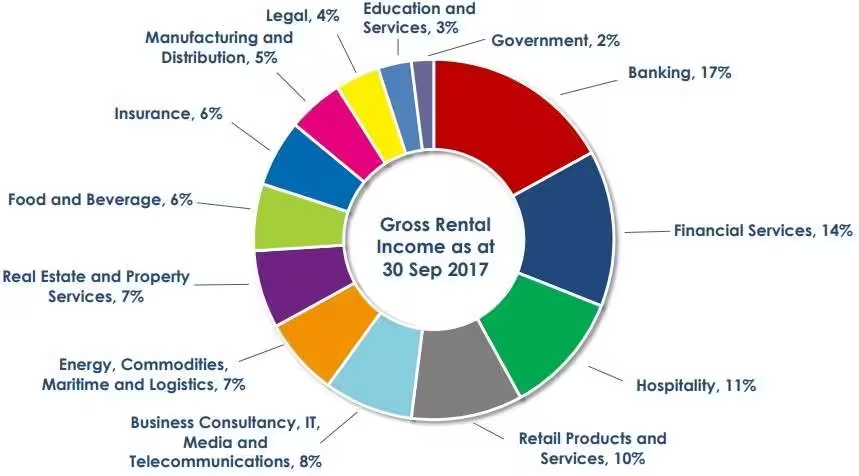

There is a good mix of tenant base however I noticed there is a higher concentration of tenants from the banking and financial industry which makes up a total of 31% of its portfolio. The concentration of tenants from the banking and financial industry is similar to Keppel REIT which has a concentration of 44% of its portfolio.

This means that in the event there is a downtrend in the financial sector and banks and financial services companies scale down and relocate to places with lower rent, this will have some impact on CapitaLand Commercial Trust.

Financial Summary

Gross revenue was slightly lower in 3Q2017 as compared to 3Q2016 however, Net Property Income, DPU seems healthy and is growing which investors are concern about.

| 3Q2017 (S$’000) |

3Q2016 (S$’000) |

Change | |

| Gross Revenue | 74,145 | 74,422 | (0.4)% |

| Net Property Income | 58,555 | 57,028 | 2.7% |

| Distributable Income | 73,109 | 68,296 | 7.0% |

| Distribution Per Unit (“DPU”) (cents) | 2.36 | 2.30 | 2.6% |

The YTD 2017 distributable income includes the income from the 50% divestment of One George Street and divestment of Wilkie Edge. DPU was higher YTD 2017 as compared to YTD 2016. If we take account into the recent rights issue, the adjusted DPU growth was estimated to be 4.8%.

| YTD Sep 2017 (S$’000) |

YTD Sep 2016 (S$’000) |

Change | |

| Gross Revenue | 251,165 | 208,851 | 20.3% |

| Net Property Income | 197,513 | 160,507 | 23.1 |

| Distributable Income | 213,868 | 198,229 | 7.9 |

| Distribution Per Unit (“DPU”) (cents) | 6.92 | 6.69 | 3.4 |

Debt

80% of CapitaLand Commercial Trust assets are unencumbered. The average cost of debt is 2.7% and average term to maturity is 2.9 years. 85% of the borrowings are fixed rate and thus it should have some form of cushion against future interest rate hikes.

Gearing ratio is 33.9%.

Management

Ms Lynette Leong is the current CEO of CapitaLand Commercial Trust. She was a a National University of Singapore graduate with a Bachelor of Science in Estate Management and a Master of Science in Real Estate. A search for her profile shows that she was once a Senior Loans Officer with Standard Chartered Bank, National Director with LaSalle Investment Management, CEO for Ascendas Korea and most importantly she has been the CEO for CapitaLand Commercial Trust for almost 10 years!

Current Valuation

Based on current price of S$1.74 and FY16 distribution of 9.08 cents, this translate to a dividend yield of 5.21%. This is comparatively non attractive given the nature of the business is an office REIT.

A fair value will be S$1.65 for a dividend yield of at least 5.5%.

Weakness

Low Distribution Yield At This Point

As I have mentioned above, at current share price, the current distribution yield is extremely not attractive at 5.21%. A good entry point will be at S$1.65 below. For office REITs, I am expecting the yield to be at least 5.5% and above.

Weak Market Rent

Grade A office rental has been weakening which means CapitaLand Commercial Trust also suffers the similar impact as compared to Keppel REIT.

Strength

Healthy Occupancy

Overall grade A office occupancy is at 99.2% which is above the market average occupancy of 91.6%. The portfolio occupancy is at 98.5% which is also above the market average occupancy of 92.5%.

Active Capital Recycling

If you have followed the news, CapitaLand Commercial Trust has recently acquired Asia Square Tower 2, kicked off the redevelopment of Golden Shoe Carpark, sold One George Street and Wilkie Edge. It is a good sign that the REIT manager is actively shuffling, redeveloping and managing their assets.

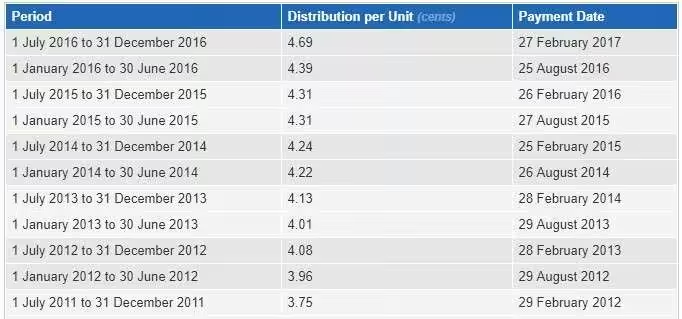

Increasing DPU

A quick glance at the distribution shows that the REIT manager is capable and able to increase its distribution payout year on year.

Redevelopment of Golden Shoe

The redevelopment of Golden Shoe car park can unlock opportunities (means higher DPU) if all turns out well. The redevelopment is expected to be completed by 1H2021 which is 4 more years down the road. I like Golden Shoe car park for its prime location within the CBD area.

vested in this too. The management has quite a good track record. worthwhile to continue to hold on =)

Hi My Investment Machine, CapitaLand Commercial Trust is in my watchlist but unfortunately I am not vested as at current price, the yield is too low for me to enter.