Mapletree Logistics Trust has released their 3Q FY22/23 Financial Results on 19th January 2023. The REIT currently makes up less than 5 percent of my stock portfolio. Depending on the results, I may decide whether to continue accumulation of Mapletree Logistics Trust.

Mapletree Logistics Trust is undergoing active portfolio rejuvenation efforts with proposed divestments of three properties in Singapore and Malaysia. This should unlock some value and probably increase in Distribution Per Unit for unitholders given the divestments.

How has Mapletree Logistics Trust performed? Let us take a look at the long awaited financial results below.

Mapletree Logistics Trust 3Q FY22/23 Financial Results

Revenue grew 8.0% year-on-year. This was attributed to contributions from accretive acquisitions that were completed in 1Q FY22/23 and FY21/22.

The gain was offset by the depreciation of mainly JPY, KRW, RMB and AUD against SGD. The good thing is that such impact of currency fluctuations at the distribution level is partially mitigated through hedging.

Distribution Per Unit (DPU) grew 1.9% year on year to 2.227 cents. Mapletree Logistics Trust received the amount of income support for 3Q FY22/23 of S$616,000 on 13th January 2023. Excluding the income support, 3Q FY22/23 DPU would be at 2.214 cents.

| 3Q FY22/23 (S$’000) |

3Q FY21/22 (S$’000) |

Change | |

| Gross Revenue | 180,203 | 166,875 | 8.0% |

| Net Property Income | 157,194 | 146,443 | 7.3% |

| Property expenses |

(23,009) | (20,432) | 12.6% |

| Amount Distributable To Unitholders | 107,112 | 96,657 | 10.8% |

| Distribution Per Unit (“DPU”) (cents) | 2.227 | 2.185 | 1.9% |

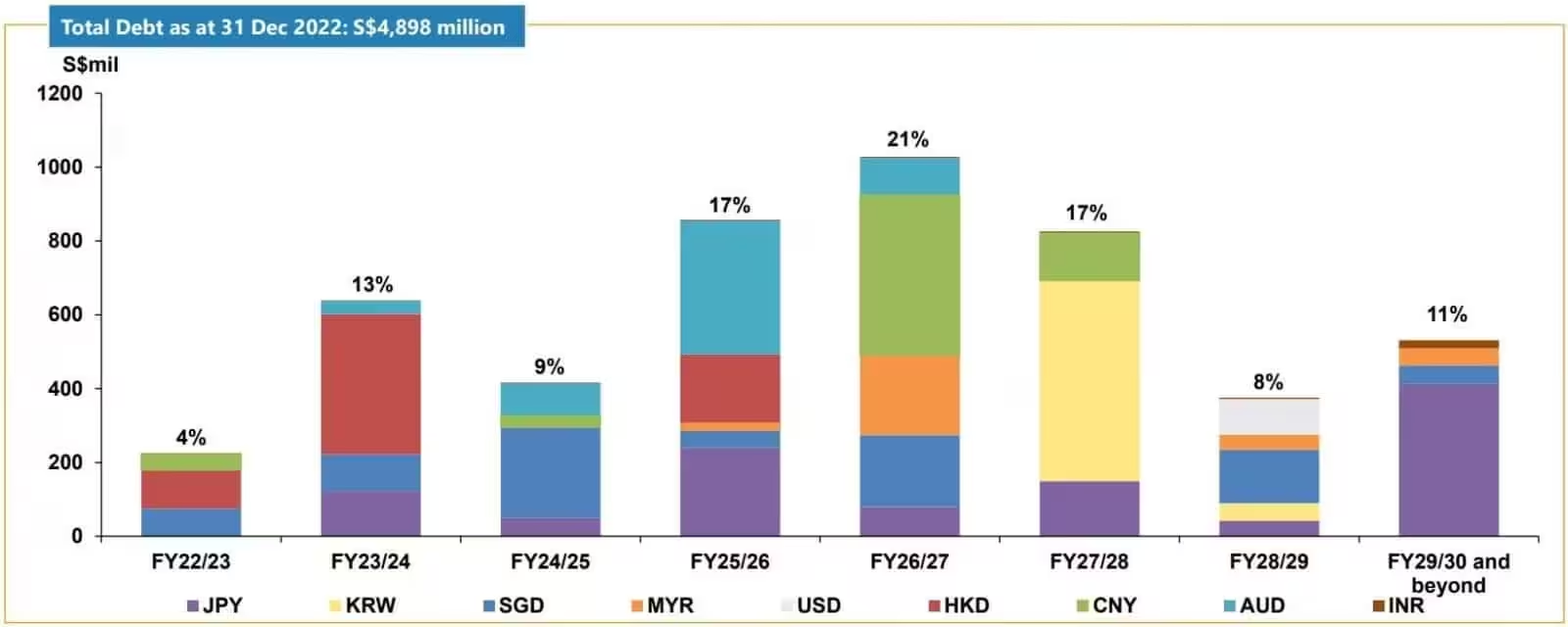

Debt

As of 31st December 2022, gearing ratio stood at acceptable range of 37.4%. This was a slight increase of 0.4% as compared to 37.0% in the last quarter.

Debt maturity profile remains well-staggered with an average debt duration of 3.6 years.

The manager shared that they have sufficient available committed credit facilities of S$1,181 million to refinance S$863 million (or 17% of total debt) debt due in FY22/23 and FY23/24.

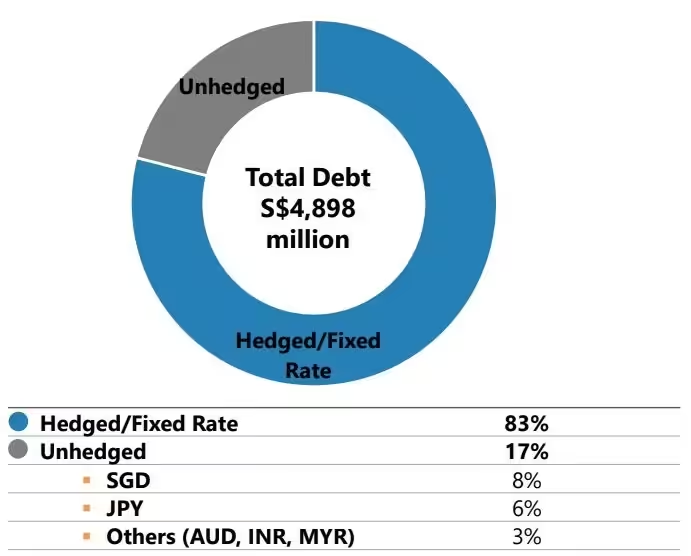

Under the rising interest rate and inflationary environment, it is important the REIT hedge their debt to mitigate against sudden interest rate hikes.

Every potential 25 bps increase in base rates may result in estimated S$0.52m decrease in distributable income or -0.01 cents in DPU per quarter. The good thing is 83% of Mapletree Logistic Trust’s total debt is hedged or drawn in fixed rates.

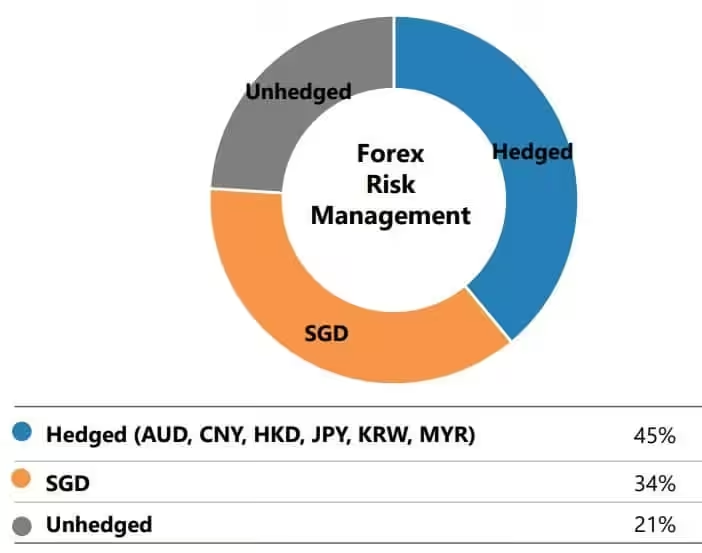

To mitigate against foreign currency fluctuations, about 79% of amount distributable in the next 12 months is hedged into or derived in SGD.

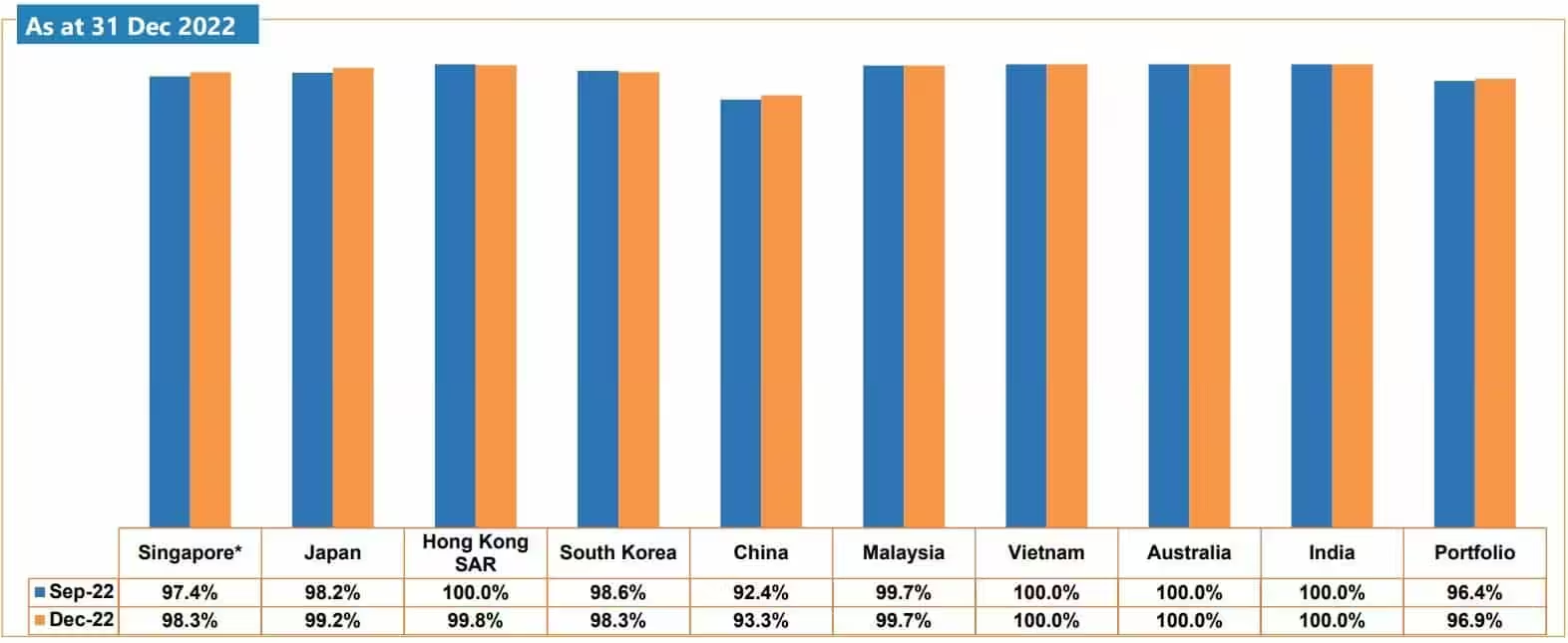

Occupancy

As of 31st December 2022, the overall portfolio occupancy stood at 96.9%.

The higher occupancy rates in Singapore, Japan and China (Guiyang, Tianjin, Wenzhou), partially offset by lower occupancy rates in Hong Kong SAR and South Korea.

Malaysia, Vietnam, Australia and India have maintained near-full or 100% occupancy rates.

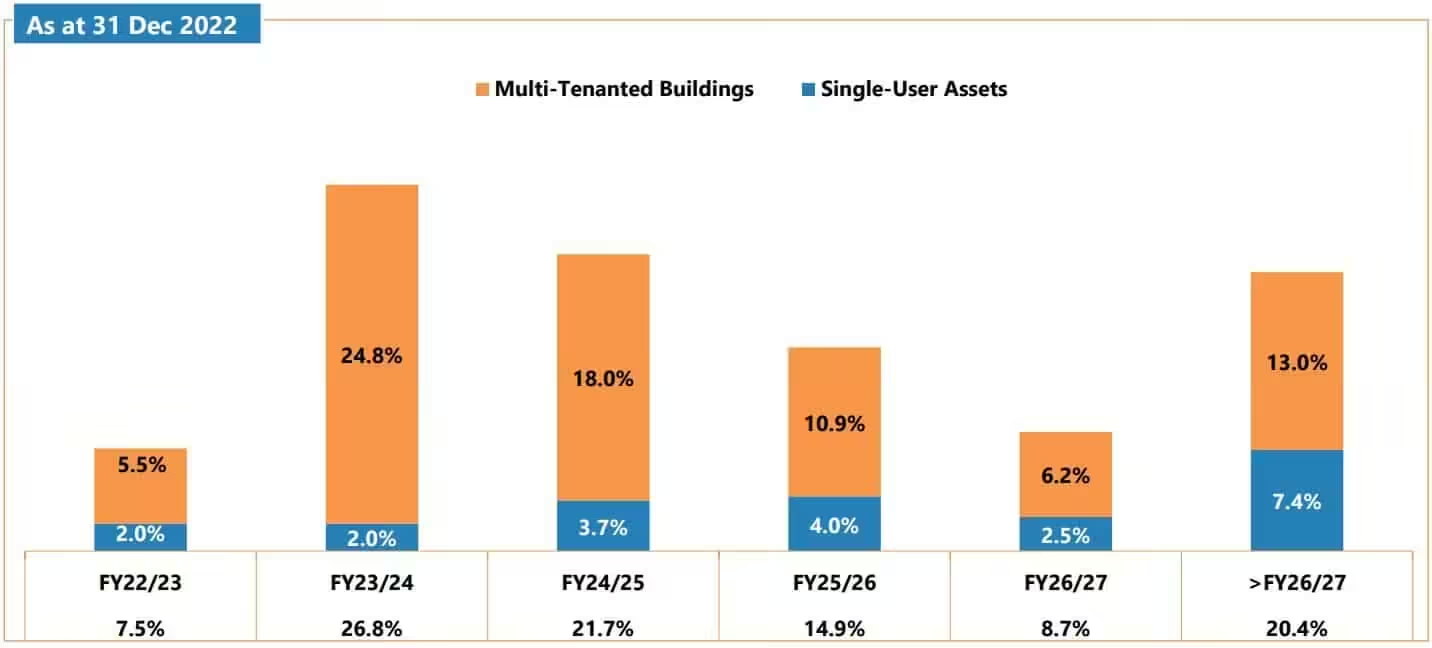

Lease expiry profile with weighted average lease expiry (by NLA) stood at 3.2 years.

Current Dividend Yield

Based on the current closing price of S$1.64 and FY21/22 full year DPU of 8.626 cents, this translate to a current dividend yield of 5.26%.

The share price is on the recovery since November 2022 and thus current dividend yield has declined.

In my opinion, the current dividend yield of 5.26% is still attractive to make an entry if you have not done so.

Summary of Mapletree Logistics Trust 3Q FY22/23 Financial Results

In summary, Mapletree Logistics Trust 3Q FY22/23 overall financial results have been positive.

- Revenue grew 8.0% year-on-year.

- Distribution Per Unit (DPU) grew 1.9% year on year to 2.227 cents.

- Gearing ratio stood at acceptable range of 37.4%.

- 83% of Mapletree Logistic Trust’s total debt is hedged or drawn in fixed rates.

- 79% of amount distributable in the next 12 months is hedged into or derived in SGD.

- Overall portfolio occupancy stood at 96.9%.

- Lease expiry profile with weighted average lease expiry (by NLA) stood at 3.2 years.

- Current dividend yield of 5.26%.