Mapletree Industrial Trust had released their 4QFY19/20 financial results on 27th April 2020. The manager had declared a Distribution Per Unit (“DPU”) of 2.85 cents. This was a decline of 7.5% as compared to 4QFY18/19 despite releasing a good set of financial results. The reason for the decline was also due to the retention of capital for COVID-19 pandemic. Without the retention of capital, the DPU for this quarter is estimated to be 3.15 cents which is an increase of 2.3% as compared to 4QFY18/19.

This quarter, Gross Revenue grew by 3.0% to S$101.8 million and Net Property Income grew by 3.2% to S$78.3 million. Distributable amount increased 15.4% to S$69.2 million. In view of the uncertainty from the COVID-19 pandemic, tax-exempt income (distributions relating to joint ventures) of S$6.6 million has been withheld in 4QFY19/20 for greater flexibility in cash management.

I am expecting more distributable income to be withheld in next few quarters as Mapletree Industrial Trust had committed to support tenants with a COVID-19 Assistance and Relief Programme of up to S$13.7 million.

Below are the 4QFY19/20 financial results.

4QFY19/20 Financial Results

| 4QFY19/20 (S$’000) |

4QFY18/19 (S$’000) |

YoY(%) | |

| Gross Revenue | 101,801 | 98,822 | 3.0% |

| Net Property Income | 78,256 | 75,850 | 3.2% |

| Distributable Amount | 69,153 | 59,936 | 15.4% |

| Distribution Per Unit (“DPU”) (cents) (Before Capital Retention) | 3.15 | 3.08 | 2.3% |

| Distribution Per Unit (“DPU”) (cents)(After Capital Retention) | 2.85 | 3.08 | (7.5)% |

FY19/20 Full Year Financial Results

Without the retention of estimated 0.30 cents in 4QFY19/20, annualized Distribution Per Unit (“DPU”) would have been 12.54 cents which is an increase of 3.13% as compared to a year ago.

| FY19/20 (S$’000) |

FY18/19 (S$’000) |

YoY(%) | |

| Gross Revenue | 405,858 | 376,101 | 7.9% |

| Net Property Income | 318,069 | 287,770 | 10.5% |

| Distributable Amount | 265,337 | 231,759 | 14.5% |

| Distribution Per Unit (“DPU”) (cents) (Before Capital Retention) | 12.54 | 12.16 | 3.13% |

| Distribution Per Unit (“DPU”) (cents)(After Capital Retention) | 12.24 | 12.16 | 0.7% |

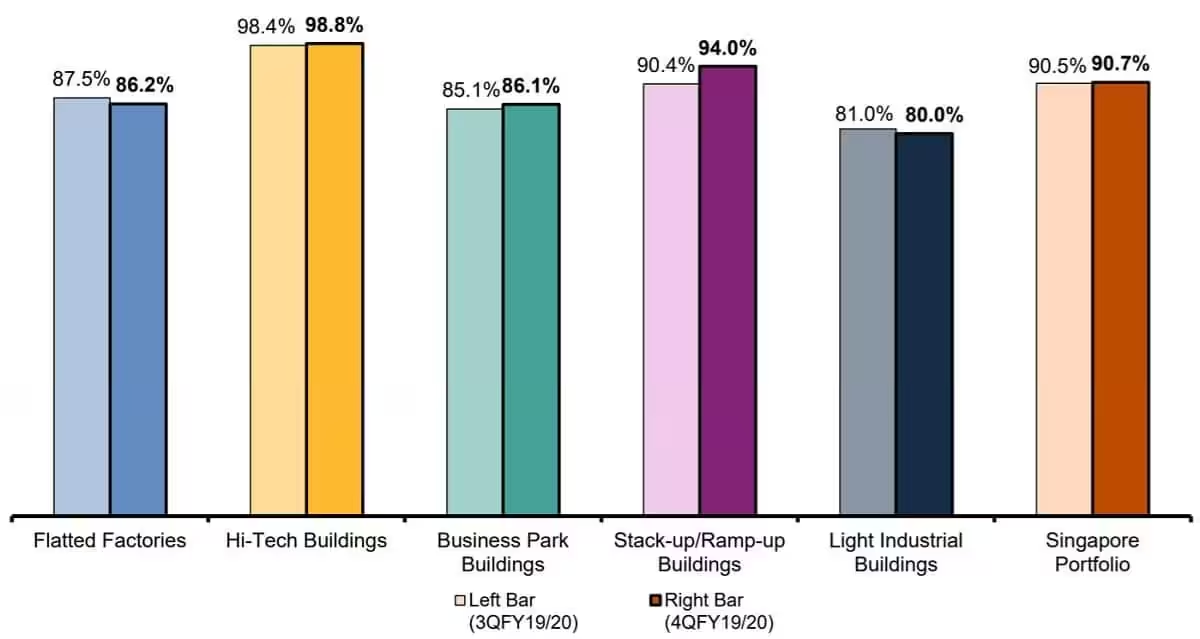

Occupancy

Overall portfolio occupancy stood at 91.5%. I didn’t quite like the occupancy take up rate for flatted factories, business park buildings and light industrial buildings. I wonder how many percentage are single tenant versus multi-tenant?

Below are the top 10 tenants by gross rental income.

As you can see above, HP is the largest tenant contributing 8% of Mapletree Industrial Trust Portfolio’s Gross Rental Income. Based on past case studies, this poses a risk should the tenant decides to shift out of its properties. (Read more: Hewlett Packard Vacates Alexandra Technopark)

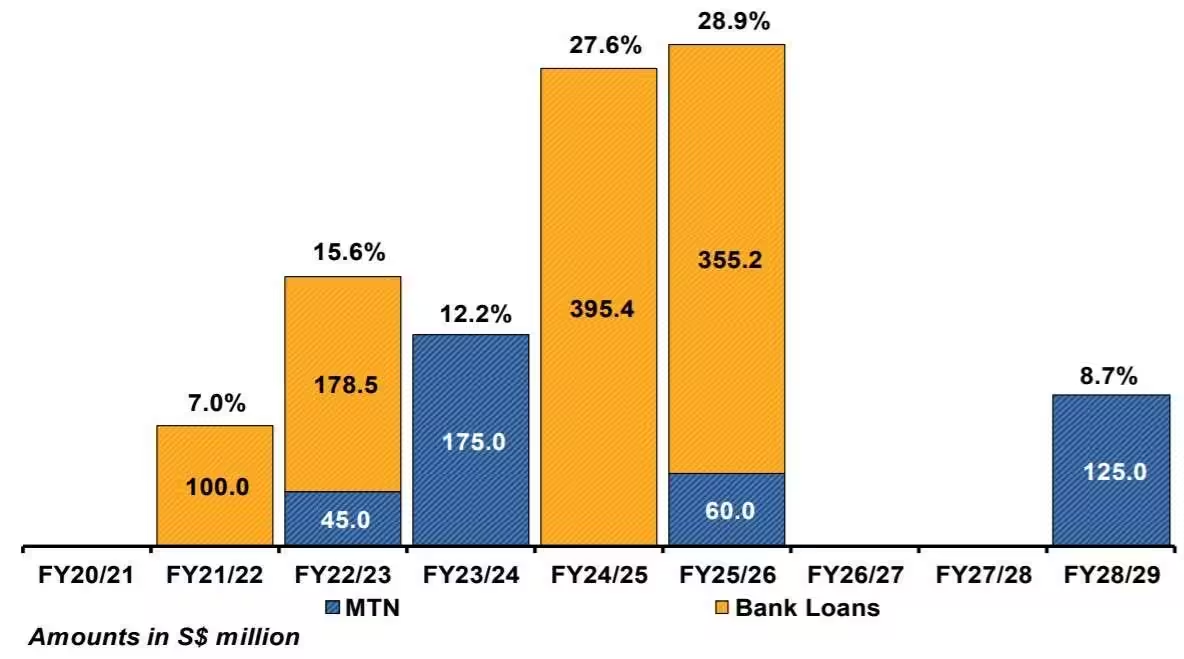

Debt

As of 31st March 2020, gearing ratio stood at 37.6% with no loans to refinance in FY20/21. For short term investment, this is a good thing as there is no debt to worry about. For longer term, we will have to monitor the COVID-19 pandemic situation.

Current Dividend Yield

Based on the current price of S$2.47 and FY19/20 full year DPU of 12.24 cents, this translate to a current dividend yield of 4.96%.

For an industrial REIT, I am expecting a dividend yield of 6% or more.

If you managed to catch Mapletree Industrial Trust at the low of S$1.91 during last month stock market crash, you will be getting a dividend yield of 6.41% which I think this should be the reasonable yield for an industrial REIT.

Summary

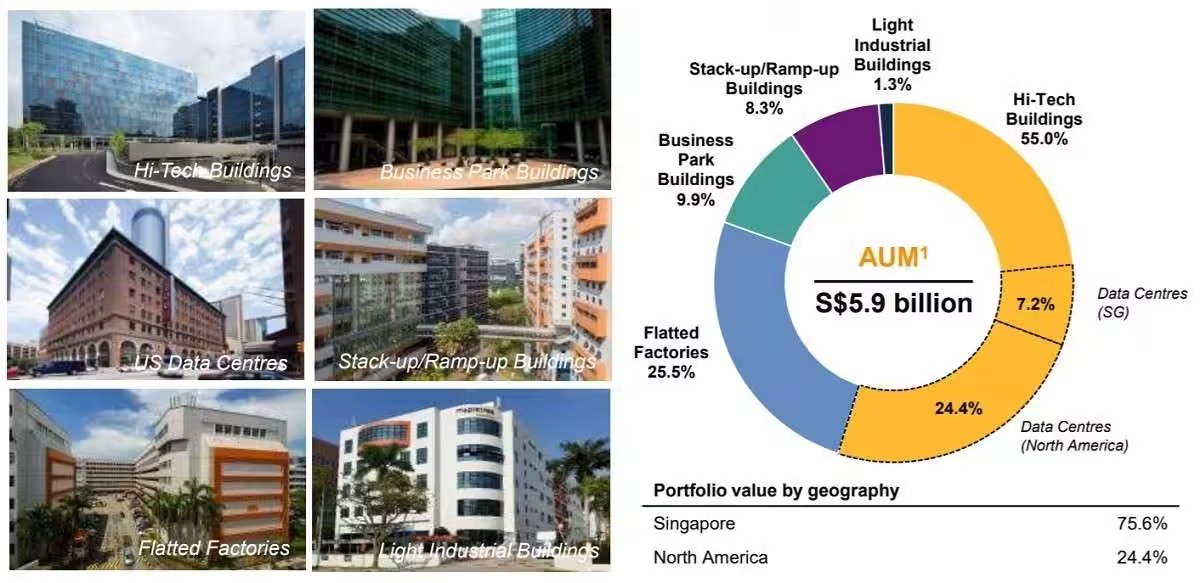

While I read about some analyst mentioning Mapletree Industrial Trust is an alternative data center play, data center only makes up 31.6% of the portfolio value. I will prefer Keppel DC REIT provided we enter at the right price.

I am expecting the share price of Mapletree Industrial Trust to come down as the manager had said that they have committed to support tenants with a COVID-19 Assistance and Relief Programme of up to S$13.7 million. This will eat into their distributable income.

As long the dividend yield is right above 6%, it will make sense to buy into Mapletree Industrial Trust.