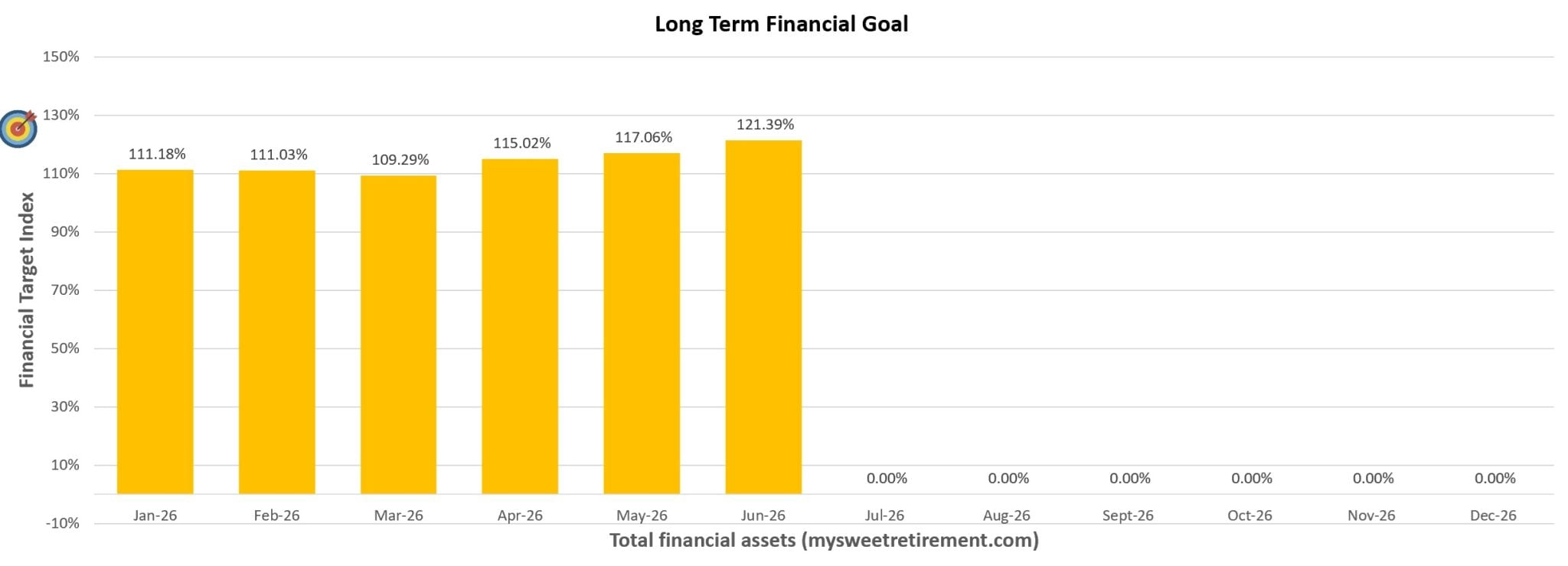

Financial planning has been the foundation of my journey toward achieving long-term financial stability, and June 2026 marks another meaningful step forward in my financial goals progress. This month, the total value of my financial assets increased by 4.33% compared to May, driven mainly by the rise in cash on hand from selling Boustead stock and receiving my annual performance bonus. These gains reinforce the importance of disciplined financial planning for retirement, especially as I continue building a diversified and resilient portfolio.

My financial assets today include insurance savings, savings accounts, fixed deposits, Singapore Savings Bonds, Singapore Treasury Bills, the current market value of my stocks, and the funds in my Supplementary Retirement Scheme (SRS) account. Each component plays a strategic role in my broader financial planning framework, helping me stay aligned with the long-term target I set for myself five years ago.

In July 2025, I achieved the financial goal I had been working toward for half a decade. Throughout those years, I focused heavily on financial planning for retirement by investing in dividend-paying stocks, accumulating Singapore Savings Bonds, and building passive income streams. These efforts gave me clarity, purpose, and motivation to make smarter financial decisions. With clear objectives, I could track my progress, adjust my strategies, and steadily strengthen my financial foundation. My long-term goal remains unchanged: to accumulate sufficient wealth that allows me to retire early in Singapore.

How to Set Achievable Financial Goals Through Financial Planning

Save 20 Percent of My Salary

One of the most effective financial planning habits I developed was saving 20% of my salary every month. GXS Bank’s savings pockets made this process simple and consistent. The moment my salary is credited, I transfer 20% into a dedicated pocket. This routine has helped me build a strong cash buffer, an essential part of financial planning for retirement because it provides stability and liquidity when opportunities arise.

Contribute to SRS

The Supplementary Retirement Scheme (SRS) is a powerful tool for financial planning. It complements CPF and encourages individuals to save more for retirement. To stay consistent, I created a savings pocket in GXS Bank and transferred funds into it monthly. In December 2025, I moved the accumulated amount and interest into my actual SRS account to maximise tax relief. I invested these funds in Singapore Treasury Bills and Singapore Savings Bonds to enhance returns. This disciplined approach strengthens my financial planning for retirement by combining tax benefits with stable, low-risk income.

Reinvest Dividends Collected from My Dividend Stock Portfolio

Compounding is one of the most important principles in financial planning. Since 2012, I have reinvested every dividend received from my stocks and REITs. Instead of treating dividends as spending money, I accumulate them and reinvest into more dividend-paying assets. Over time, this creates a snowball effect that accelerates wealth growth. This long-term discipline is a cornerstone of financial planning for retirement because it builds passive income that supports future financial independence.

Side Hustle

In April 2025, I expanded my financial planning strategy by starting a side hustle. I began selling stock investment and personal finance books on my blog. Reading investment and finance books has helped me improve my financial literacy, sharpen my decision-making, and avoid common mistakes. This side hustle not only generates additional income but also reinforces my financial planning mindset by keeping me engaged with wealth-building knowledge.

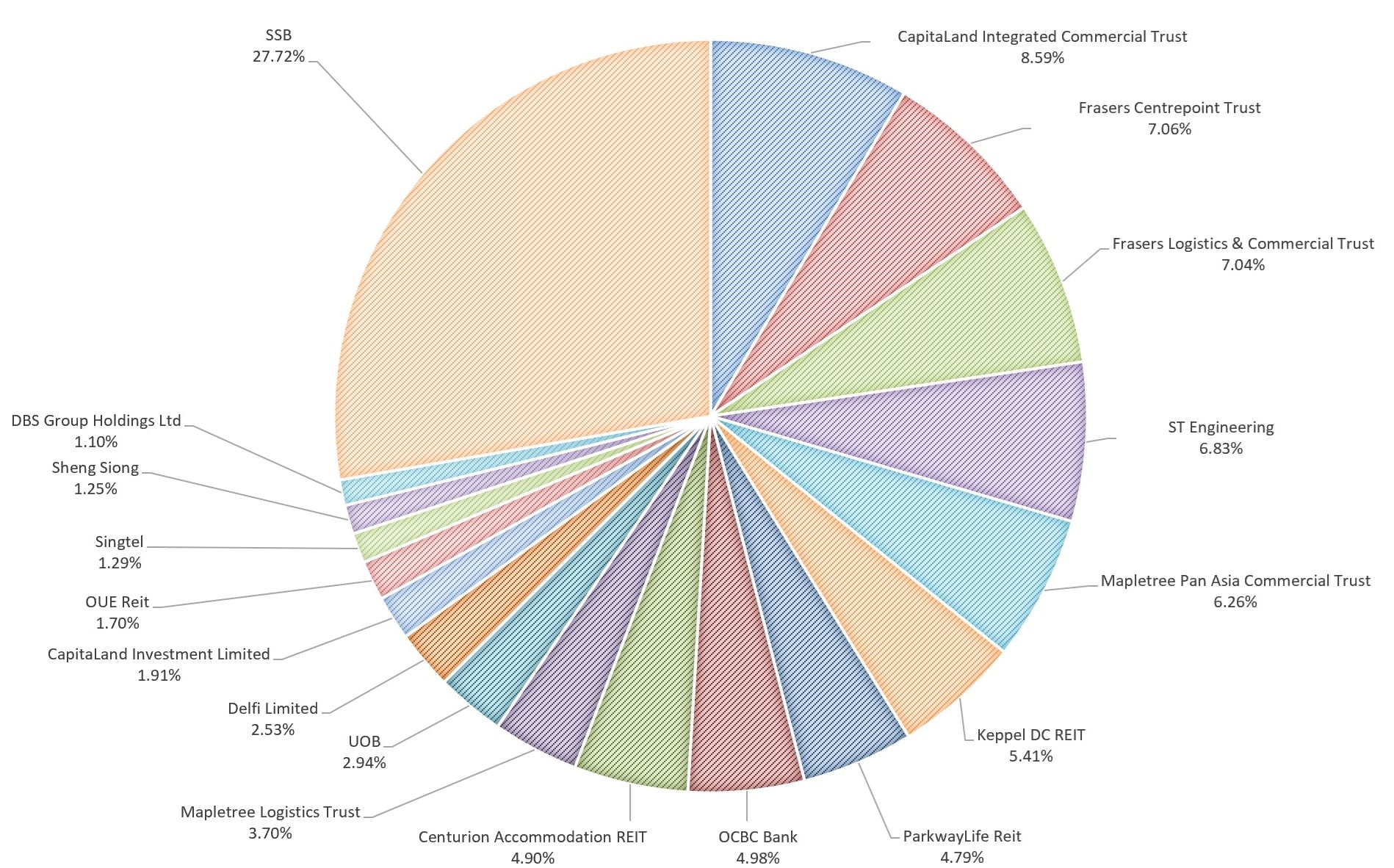

My Dividend Stock Portfolio

My Singapore dividend stock portfolio reflects a disciplined financial planning approach. In 2025, I collected a total dividend of $20,289.89 from the stocks in my portfolio. REITs such as CapitaLand Integrated Commercial Trust and Frasers Centrepoint Trust provide reliable distributions, while companies like OCBC, UOB, and ST Engineering add stability and long-term value. This mix ensures a dependable passive income stream that strengthens my financial planning for retirement.

In June, I added more Singapore Savings Bond to my stock portfolio which increase my passive income further.

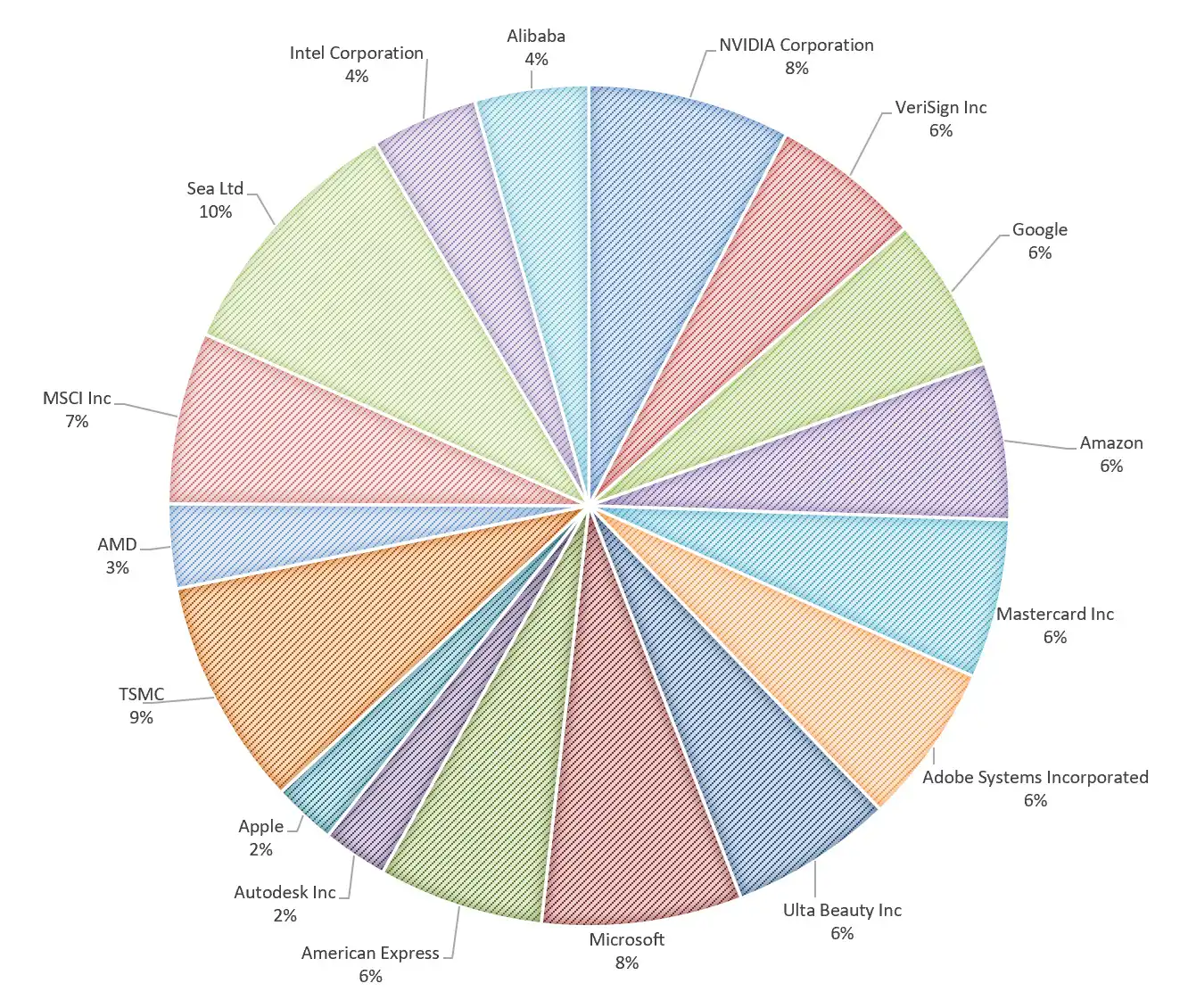

My US stock portfolio complements this strategy with long-term growth companies such as Microsoft, NVIDIA, TSMC, Amazon, and Google. These businesses operate in industries with durable demand and global reach. Their long-term capital appreciation plays a crucial role in my financial planning for retirement, allowing me to build wealth beyond dividends and fixed-income instruments.

Summary of Financial Goals Progress for June 2026

Despite the increase in my total financial assets, I continue to remind myself to stay cautious. Global political tensions, especially between the US and Iran, could trigger market volatility. The rapid rise of artificial intelligence also presents risks if innovations fail to translate into real business value. These uncertainties highlight why financial planning is essential, particularly financial planning for retirement, where long-term stability matters more than short-term excitement.

For now, my focus remains clear: stay invested, stay disciplined, and continue building my savings. Many financial bloggers call this a “war chest”, a pool of capital ready to deploy when opportunities arise. Strengthening this war chest is a key part of my financial planning strategy, ensuring I can take advantage of future market dips rather than fear them.

How are you working towards your financial goals today?