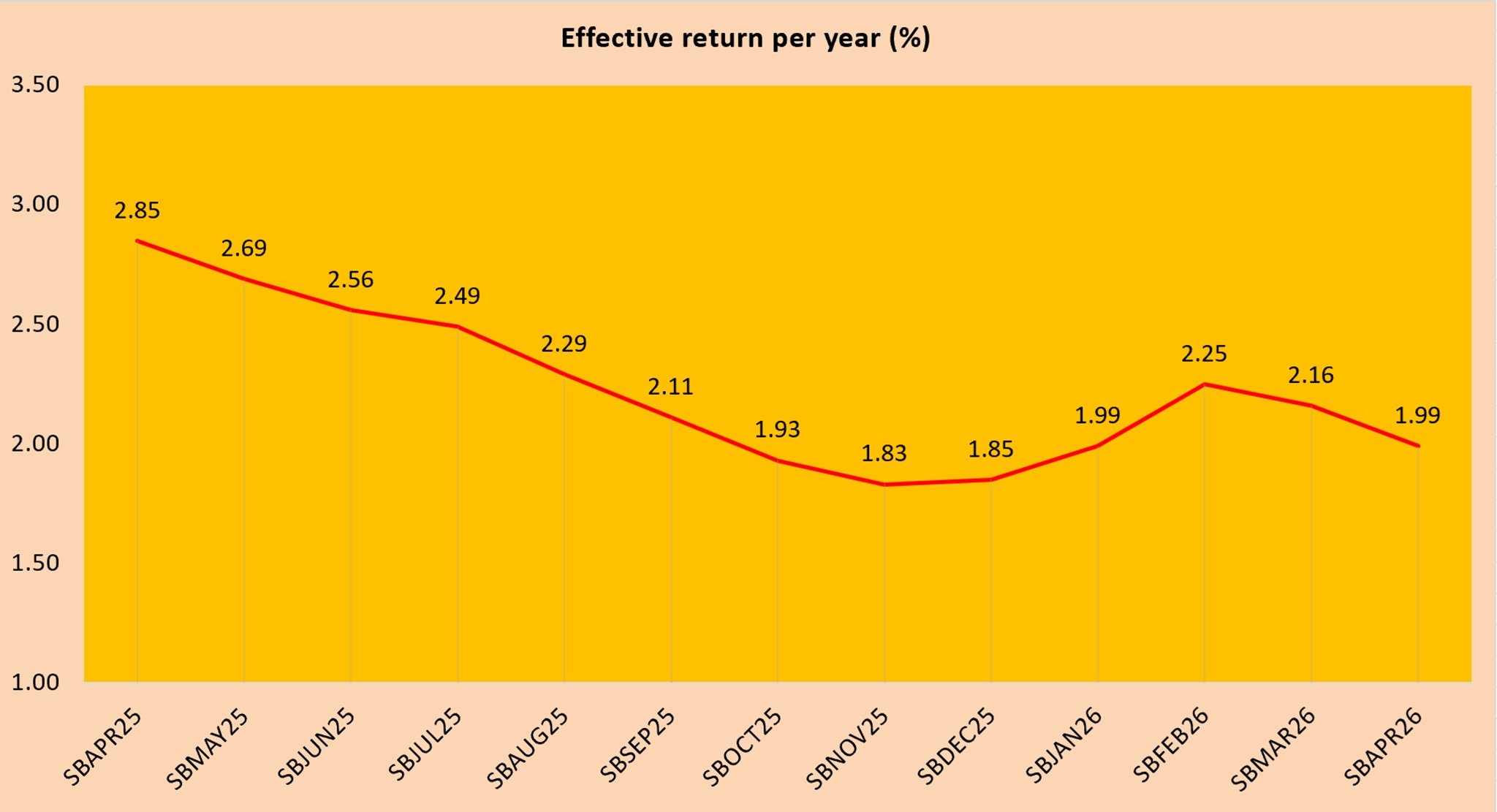

The effective interest rate for the Singapore Savings Bond interest rate SBAPR26 GX26040E is 1.99% if I hold it to maturity over 10 years. If I sell SBAPR26 after one year, Singapore Savings Bond interest rate is 1.36% per annum. Investing in Singapore Savings Bond is unlike chasing promotional bank rates that change every few months. Singapore Savings Bond offers predictability. I know exactly what I will get if I hold it, and the “step‑up” feature means my returns grow the longer I stay invested. It is almost like being rewarded for patience, a trait that aligns perfectly with how I have approached retirement planning.

With just $500 as the entry point, it feels accessible. And for me, it is not just about the numbers. It is about building a disciplined savings journey, one step at a time. Adding SBMAR26 to my portfolio is not just another investment decision, it is a way of reinforcing the long‑term plan my wife and I have been nurturing for years: steady growth, predictable income, and the peace of mind that comes with knowing our retirement savings are on track.

What are the Benefits of Investing in Singapore Savings Bonds?

Despite relatively modest yields, SSBs are low-risk investments, perfect for conservative investors seeking steady growth. The longer you hold them, the higher your effective return. Each individual can invest up to S$200,000, inclusive of both cash and SRS contributions.

In the next section, we will walk through how to calculate your potential returns using the MAS SSB Calculator.

How to Buy Singapore Savings Bonds Online

Buying Singapore Savings Bonds is a straightforward process, and everything can be done digitally once you have an individual CDP account with the Central Depository. This account is essential because it serves as the place where your SSB holdings will be kept. After your CDP account is set up, you can apply for SSBs through the online banking platforms of DBS/POSB, OCBC or UOB, or by using their ATMs. Simply log in to your bank account, navigate to the Singapore Government Securities section and follow the on‑screen instructions to submit your application.

The minimum investment amount is $500, and you can increase your subscription in multiples of $500, up to a maximum of $200,000 per SSB issuance. A new bond is released every month, and its interest rates are updated annually based on prevailing market conditions. Once your application is successful, interest will be paid to you twice a year, and your full principal will be returned at the end of the ten‑year term.

Where Can I Check the Latest Interest Rates for Singapore Savings Bonds?

The latest Singapore Savings Bond interest rates are published on the Monetary Authority of Singapore’s Singapore Savings Bond Portal. Each monthly issuance comes with a full schedule of rates across the ten‑year term, making it easy for investors to review and compare returns. MAS also provides a Singapore Savings Bonds Calculator, which allows you to estimate your total interest earnings based on your investment amount and holding period.

For instance, an investment of S$10,000 in the SBAPR26 (GX26040E) tranche held to maturity would generate a total of S$2,017.00 in interest. Below is the breakdown of the annual payouts for SBAPR26 (GX26040E) across its ten‑year duration.

| Year from issue date | Interest % | Average return per year %* |

| 1 | 1.36 | 1.36 |

| 2 | 1.36 | 1.36 |

| 3 | 1.51 | 1.41 |

| 4 | 1.76 | 1.50 |

| 5 | 1.94 | 1.58 |

| 6 | 2.08 | 1.66 |

| 7 | 2.26 | 1.74 |

| 8 | 2.45 | 1.82 |

| 9 | 2.63 | 1.91 |

| 10 | 2.82 | 1.99 |

*At the end of each year, on a compounded basis.

How To Track Singapore Savings Bonds?

You can monitor your Singapore Savings Bonds by visiting the Monetary Authority of Singapore (MAS) website, which offers up-to-date information on bond issuance and performance.

![]() I use Stocks Café to track my SSB Singapore purchases. If you like to know more about Stocks Cafe, please read up my previous review of Stocks Cafe.

I use Stocks Café to track my SSB Singapore purchases. If you like to know more about Stocks Cafe, please read up my previous review of Stocks Cafe.

Should I Consider SBAPR26 (GX26040E)?

The SBAPR26 Singapore Savings Bond stands out as a steady, low‑risk option at a time when fixed‑deposit and savings‑account rates are gradually easing. Its effective return of 1.99 percent per annum over ten years, along with a shorter‑term return of 1.36 percent per annum, may not be headline‑grabbing, but it offers something increasingly rare in today’s environment: stability. The predictable step‑up structure and government‑backed security make it a dependable choice for investors who prefer certainty over volatility.

With some spare cash available, I see SBAPR26 (GX26040E) as a practical addition to my long‑term retirement portfolio. It allows me to lock in consistent returns while complementing my broader investment strategy, providing a disciplined and low‑maintenance way to grow my savings over time.