The merger between OUE Commercial REIT and OUE Hospitality Trust seems to be beneficial. On 30th January 2020, OUE Commercial REIT announced its first financial results (4Q2019) after the merger with OUE Hospitality Trust.

Gross Revenue improved 80.7% to S$86.8 million and Net Property Income (“NPI”) increased by 92.6% to S$70.6 million. These are good financial figures that can never be achieved by OUE Hospitality Trust alone.

Higher net property income and the drawdown of OUE Downtown Office’s income support was partially offset by higher interest expenses in 4Q 2019 from higher borrowings which resulted in amount available for distribution of S$46.6 million.

As S$1.1 million was retained by the manager for working capital purposes, S$45.1 million was available for distribution. This translates to a Distribution Per Unit (“DPU”) of S$0.84 cents which was 12% higher compared to 4Q2018.

4Q2019 Financial Results

| 4Q2019 (S$’mil) |

4Q2018 (S$’mil) |

Change | |

| Gross Revenue | 86.8 | 48.0 | 80.7% |

| Net Property Income | 70.6 | 36.6 | 92.6% |

| Amount available for Distribution | 46.6 | 21.5 | 116.9% |

| Amount to be Distributed (After Retention) | 45.1 | 21.5 | 109.9% |

| Distribution Per Unit (“DPU”) (cents) | 0.84 | 0.75 | 12.0% |

FY2019 Financial Results

| FY2019 (S$’mil) |

FY2018 (S$’mil) |

Change | |

| Gross Revenue | 257.3 | 176.4 | 45.9% |

| Net Property Income | 205.0 | 138.2 | 48.3% |

| Amount available for Distribution | 124.7 | 71.3 | 74.9% |

| Amount to be Distributed (After Retention) | 123.2 | 71.3 | 72.8% |

| Distribution Per Unit (“DPU”) (cents) | 3.31 | 3.48 | (4.9)% |

While the 4Q2019 financial results were all positive, the full year financial results was not. The full year distribution per unit was 4.9% lower at 3.31 cents as compared to 3.48 cents in FY2018.

Debt

Gearing ratio stood at 40.3% which was high in my opinion.

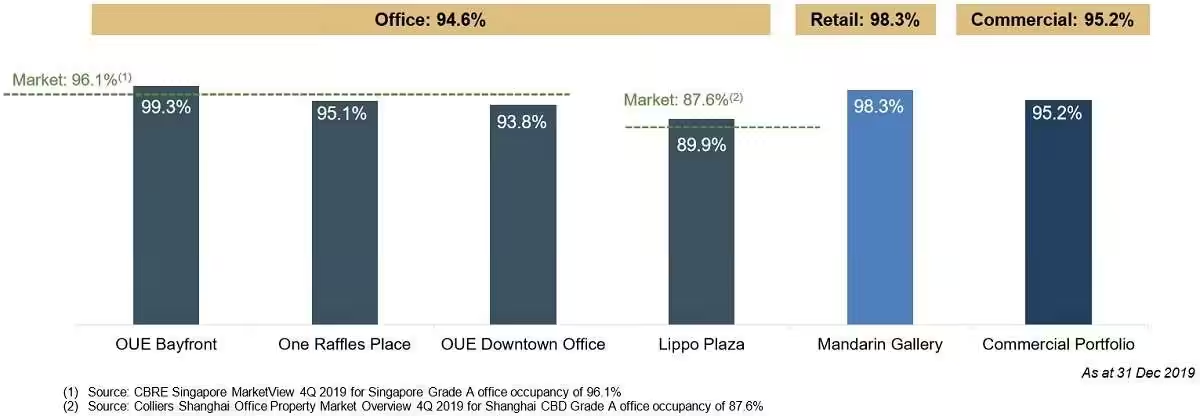

Occupancy

The commercial portfolio occupancy stood healthy at 95.2% as of 31 December 2019.

Average Passing Rent

As you can see below, the average passing office rent for all three Singapore office properties improved as at 4Q 2019 due to consecutive quarters of positive rental reversions. On the other hand, the passing rent for Lippo Plaza (Shanghai) and Mandarin Gallery continues to be depressed.

RevPar

RevPAR improved by 1.9% to S$216 on the back of higher room rates and stronger demand at Crowne Plaza Changi Airport. This was supported by increased tourist arrivals and strong line-up of major events during the quarter on the back of a benign supply environment.

Crowne Plaza Changi Airport continued to improve its operating performance and achieved a 9.9% increase in RevPAR of S$198 for 4Q 2019, on the back of higher room rates and increased demand from the corporate and wholesale segments.

Mandarin Orchard Singapore maintained a relatively stable operating performance on the stronger demand amidst a competitive trading environment and achieved a RevPAR of S$226 for 4Q2019.

Summary

While OUE Commercial REIT has released a good set of financial results after its merger, I believe most investors are worried about the impact of the Wuhan virus on OUE Commercial REIT as we all know that Singapore tourism is being hit as there are significantly less China tourists. In 2019 alone, China tourists makes up 22% of tourists arrival in Singapore. We can imagine the impact on the hospitality sector.

I would say the merger came at the right time. As you can see below, 69% of the revenue comes from the commercial segment while 31% makes up the hospitality segment. Of course there will be some form of impact to the overall revenue but the commercial segment can help to offset the lower revenue from the hospitality segment.

Even though RevPar has improved in 4Q2019, I will expect RevPar to be lower in upcoming quarters due to the impact of the Wuhan (2019-nCoV) virus on tourism.

Currently, OUE Commercial REIT only makes up 3% of my entire stock portfolio. Thus, I shall keep calm and collect dividends.