On 23rd April 2025, Mapletree Logistics Trust announced their 4QFY24/25 financial results. Last year, the manager of Mapletree Logistics Trust adopted the strategy to divest assets with older specifications and of limited redevelopment potential as part of their portfolio rejuvenation. This is the 4th quarter financial results, which makes up the full year. How has Mapletree Logistics Trust performed in FY24/25?

Mapletree Logistics Trust 4QFY24/25 Financial Results

In 4QFY24/25, Mapletree Logistics Trust’s gross revenue was lower mainly due to lower contribution from China and the absence of revenue contribution from divested properties. Another reason was the currency weakness (mainly KRW, HKD, and JPY) which were mitigated by higher contribution from Singapore, Australia, and Hong Kong SAR and from the contribution from acquisitions completed in 1Q FY24/25. The impact of currency weakness was partially mitigated through the use of foreign currency forward contracts to hedge foreign-sourced income.

Property expenses increased due to higher utilities, property maintenance expenses, and

contribution from acquisitions completed in 1Q FY24/25. These were partly offset by absence of property expenses from divested properties and currency weakness.

Borrowing costs rose 4.0% year-on-year to S$38.7 million. This was due to higher average interest rate on existing debts and incremental borrowings to fund acquisitions in 1QFY24/25.

Notwithstanding the weakness, a distributable income of S$104.6 million and Distribution Per Unit (“DPU”) of 1.955 cents for 4QFY24/25 was announced. Distribution Per Unit fell 11.6% year-on-year.

| 4QFY24/25 (S$’000) |

4QFY23/24 (S$’000) |

% Change | |

| Gross Revenue | 179,613 | 180,981 | (0.8) |

| Property Expenses |

(26,812) | (25,668) | 4.5 |

| Net Property Income | 152,801 | 155,313 | (1.6) |

| Borrowing Costs | (38,692) | (37,217) | 4.0 |

| Amount Distributable | 104,639 | 116,472 | (10.2) |

| Distribution Per Unit (“DPU”) (cents) | 1.955 | 2.211 | (11.6) |

Mapletree Logistics Trust Full Year FY24/25 Financial Results

The reasons for the decline in Gross Revenue are similar to what was shared above. Thus, I shall not be repeating them.

Mapletree Logistics Trust’s full year Distribution Per Unit (DPU) for FY24/25 fell 10.6% to 8.053 cents as compared to 9.003 cents in FY23/24.

| FY24/25 (S$’000) |

FY23/24 (S$’000) |

% Change | |

| Gross Revenue | 727,026 | 733,889 | (0.9) |

| Property Expenses |

(101,733) | (98,945) | 2.8 |

| Net Property Income | 625,293 | 634,944 | (1.5) |

| Borrowing Costs | (156,893) | (145,905) | 7.5 |

| Amount Distributable | 430,628 | 471,489 | (8.7) |

| Distribution Per Unit (“DPU”) (cents) | 8.053 | 9.003 | (10.6) |

Debt

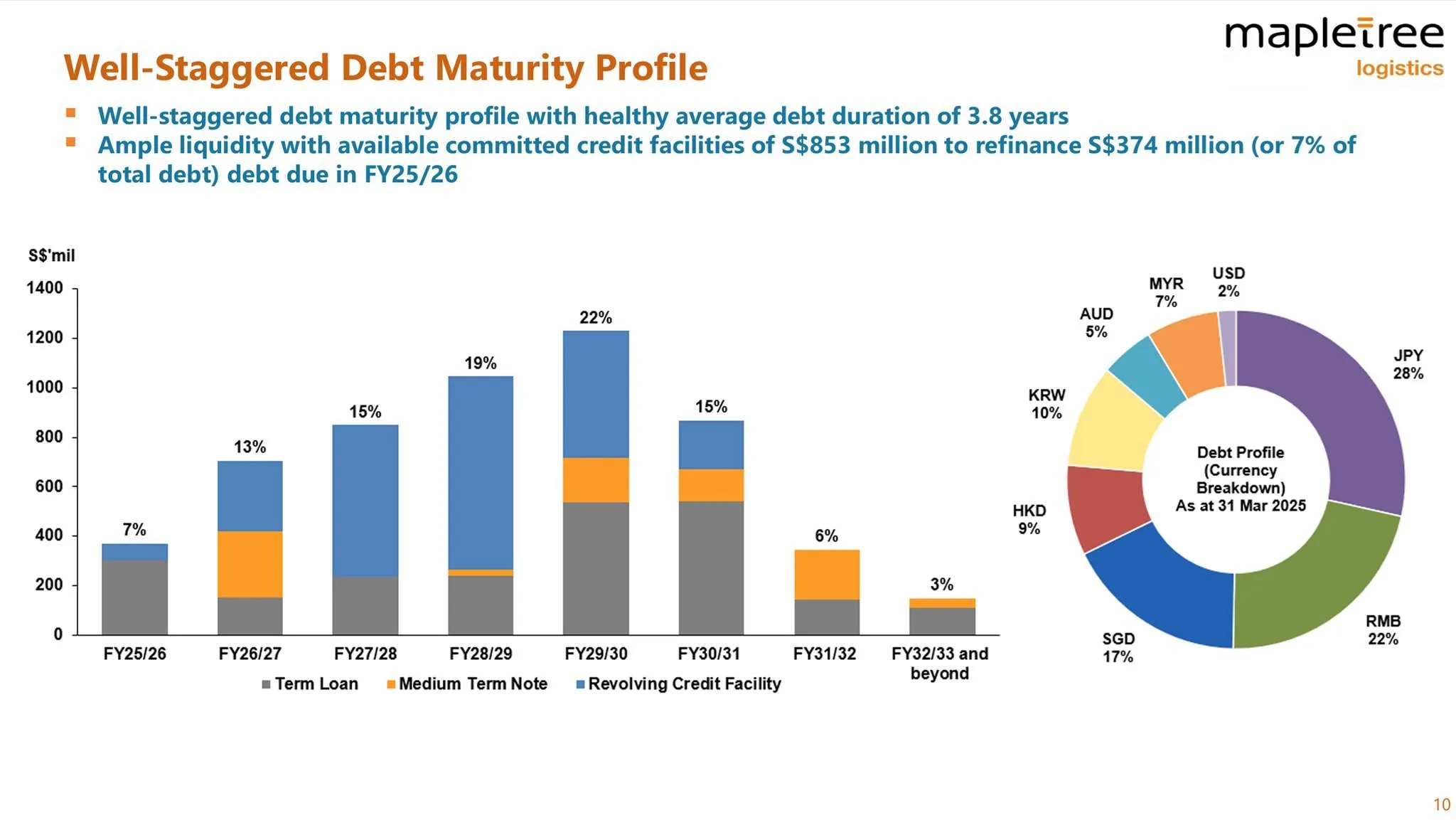

As of 31st March 2025, Mapletree Logistics Trust’s aggregate leverage stood at a high of 40.7%. Despite a high aggregate leverage, Mapletree Logistics Trust’s debt maturity profile remains well-staggered with healthy average debt duration of 3.8 years. The manager assured that there is ample liquidity with available committed credit facilities of S$853 million to refinance S$374 million (or 7% of total debt) debt due in FY25/26.

What are the benefits of having a well-staggered debt maturity profile? Having a well-staggered debt maturity profile is crucial for REITs to manage their debt obligations effectively. By spreading out debt repayments over different time periods, REITs can avoid liquidity crunches and reduce the risk of default.

Furthermore, a well-staggered debt maturity profile allows REITs to take advantage of changes in interest rates. For example, if interest rates drop, REITs with debt maturing in the future can refinance at lower rates, reducing their interest expenses.

Overall, maintaining a well-staggered debt maturity profile is a sound financial strategy that can help ensure the long-term sustainability of the REIT’s finances.

Occupancy

Mapletree Logistics Trust’s portfolio overall occupancy stood at 96.2%. Occupancy was slightly higher in Japan and China.

One of the good news is that Mapletree Logistics Trust maintained its positive rental reversions across all markets except China. The bad news is that the negative rental reversion in China is expected to continue.

Do you know what is rental reversion? Rental reversion refers to the change in rental rates when leases are renewed. A positive rental reversion means the new rental rate is higher than the previous rate. A negative rental reversion happens when the new rental rate is lower than the previous rate. Whether the rental reversion is positive or negative depends on the market demand and supply.

Lease Expiry

Weighted average lease expiry for the portfolio stood at approximately 2.8 years. As you can see from the chart above, overall lease expiry remains well staggered.

Mapletree Logistics Trust Share Price and Dividend Yield

Mapletree Logistics Trust share price closed at S$1.13 on Friday. Based on Mapletree Logistics Trust’s FY24/25 full year distribution of 8.053 cents and current share price of S$1.13, this translates to a current dividend yield of 7.13%.

Do you know how to calculate the current dividend yield? The formula for calculating the current dividend yield is straightforward. It is calculated by dividing the annual dividends per share by the current market price per share. Here is the formula in mathematical terms:

Summary of Mapletree Logistics Trust 4QFY24/25 Financial Results

In my opinion, Mapletree Logistics Trust’s current quarter result remained negative. Let me summarize the pro and cons.

The pros are:

- Healthy average debt duration of 3.8 years with ample liquidity with available committed credit facilities of S$853 million to refinance S$374 million (or 7% of total debt) debt due in FY25/26.

- Portfolio occupancy remained resilient at 96.2%.

- Excluding China, portfolio rental reversion was positive 6.9%. Lease expiry remains well staggered

- Because of falling share price, current dividend yield is high at 7.13%.

The cons are:

- Gross Revenue and Net Property Income fell 0.8% and 1.6% year-on-year respectively.

- Distribution Per Unit fell 11.6% year-on-year. Full year distribution fell 10.6%.

- High gearing ratio of 40.7% and it grew 0.4% as compared to previous quarter.

Again, with every portfolio rejuvenation, it will take time to see value delivered to unitholders. Having said that, I seriously hope Mapletree Logistics Trust can take a look at managing its growing aggregate leverage.