Mapletree Industrial Trust has a portfolio that comprises of 87 industrial properties in Singapore and 27 data centres in North America (through the joint ventures with Mapletree Investments Pte Ltd).

In my previous post, I mentioned that some analysts considered Mapletree Industrial Trust as an alternative data center play even though data centre only makes up 31.6% of the portfolio value.

Today, Mapletree Industrial Trust has announced their proposed acquisition of the remaining 60% interest in the 14 data centres located in the United States of America.

With the acquisition, this will increase their data centre exposure from 31.6% to 39.0% in terms of Assets Under Management (“AUM”).

What are the benefits of the proposed acquisition?

I believe investors will be keen to understand the rationale or benefits of the proposed acquisition. Below are the rationale and benefits listed in their presentation slides. I have highlighted the points that I felt important in green.

#1 Increases MIT’s Exposure to the Resilient Data Centres Segment

I agree with Mapletree Industrial Trust that the COVID-19 crisis has provided a favourable tailwinds for the data centres segment. Cloud providers have reported strong demand for data centre space during the pandemic.

The global revenue for cloud computing is expected to grow at a compounded annual growth rate (“CAGR”) of 14% from 2018 to 2024F. An accelerated growth may be expected as a result of the pandemic.

Data centres were identified as essential infrastructure in North America during the pandemic and had remained open during the lockdown period.

#2 Enhances Income Stability of the Enlarged Portfolio

81.6% of the Mapletree Redwood Data Centre Trust’s portfolio comprises of powered shell data centres. If you do not know what are powered shell data centres, they are facilities with exterior construction completed, available power and connectivity, but with the interior left as raw space to be finished by the customer.

All the tenants are on triple net lease structures whereby all maintenance, tax and insurance charges are borne by the tenants. 97.8% of the Mapletree Redwood Data Centre Trust’s portfolio has annual rental escalations of 2.0% and above, providing stable and growing cash flows.

The acquisition will augment Mapletree Industrial Trust’s tenant base with higher exposure to resilient data centre tenants. As you can see below under Post-Acquisition, it also diversifies Mapletree Industrial Trust’s tenant base and reduces exposure to any single tenant from 8.0% to 7.2%.

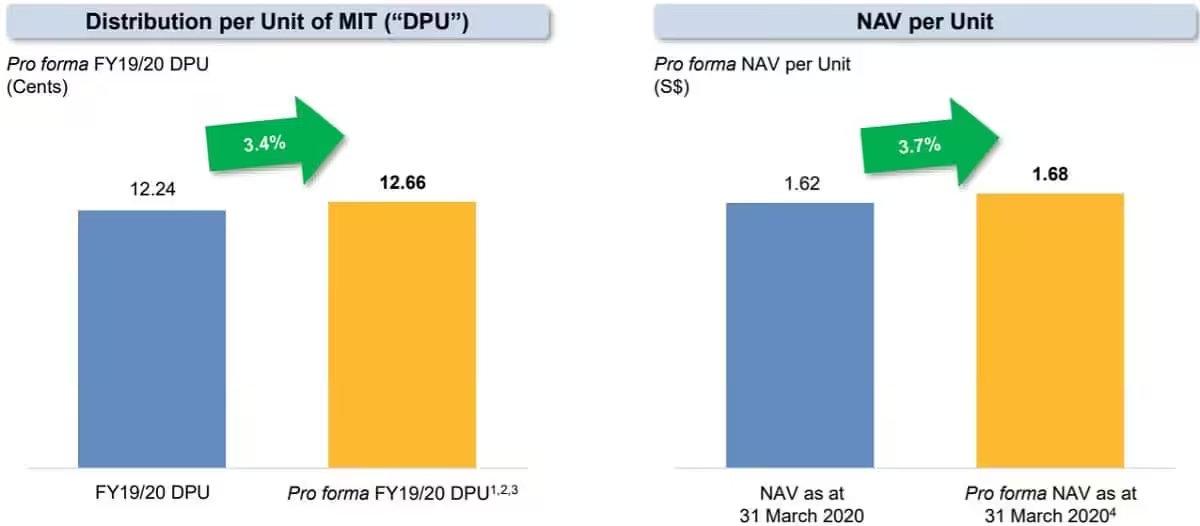

#3 DPU and NAV Accretive to Unitholders

Post acquisition, the distribution per unit (“DPU”) is expected to increase 3.4% from 12.24 cents to 12.66 cents.

Net Asset Value (“NAV”) is expected to increase from S$1.62 to S$1.68.

#4 Strong Support from the Sponsor

As at 31 March 2020, the Sponsor owns and manages S$60.5 billion worth of properties across Asia Pacific, Europe, the United Kingdom and the U.S., of which S$12.5 billion of properties are located in North America.

Mapletree Industrial Trust will continue to leverage on the Sponsor’s local market experience to manage the Mapletree Redwood Data Centre Trust’s portfolio.

Right of first refusal was granted to Mapletree Industrial Trust over future sale of 50.0% interest in Mapletree Rosewood Data Centre Trust (“MRODCT”).

Acquisition to be fully funded by equity

The acquisition will be fully funded by equity with excess proceeds to be used for debt repayment, future acquisitions and/or general corporate and/or working capital purposes.

This will be done via a private placement to raise gross proceeds of no less than approximately S$350.0 million.

| Funding Requirements | |

| Purchase Consideration | US$210.9 million (approximately S$299.5 million) |

| Transaction Cost | US$2.2 million (approximately S$3.1 million) |

| Acquisition Fee | US$4.9 million (approximately S$7.0 million) |

| Total Acquisition Outlay | US$218.0 million (approximately S$309.6 million) |

Pro Forma Dividend Yield

Based on the current share price of S$2.84 and pro forma distribution per unit of 12.66 cents, this translates to an estimated dividend yield of 4.46%.

I wish I had bought into Mapletree Industrial Trust during the stock market crash.