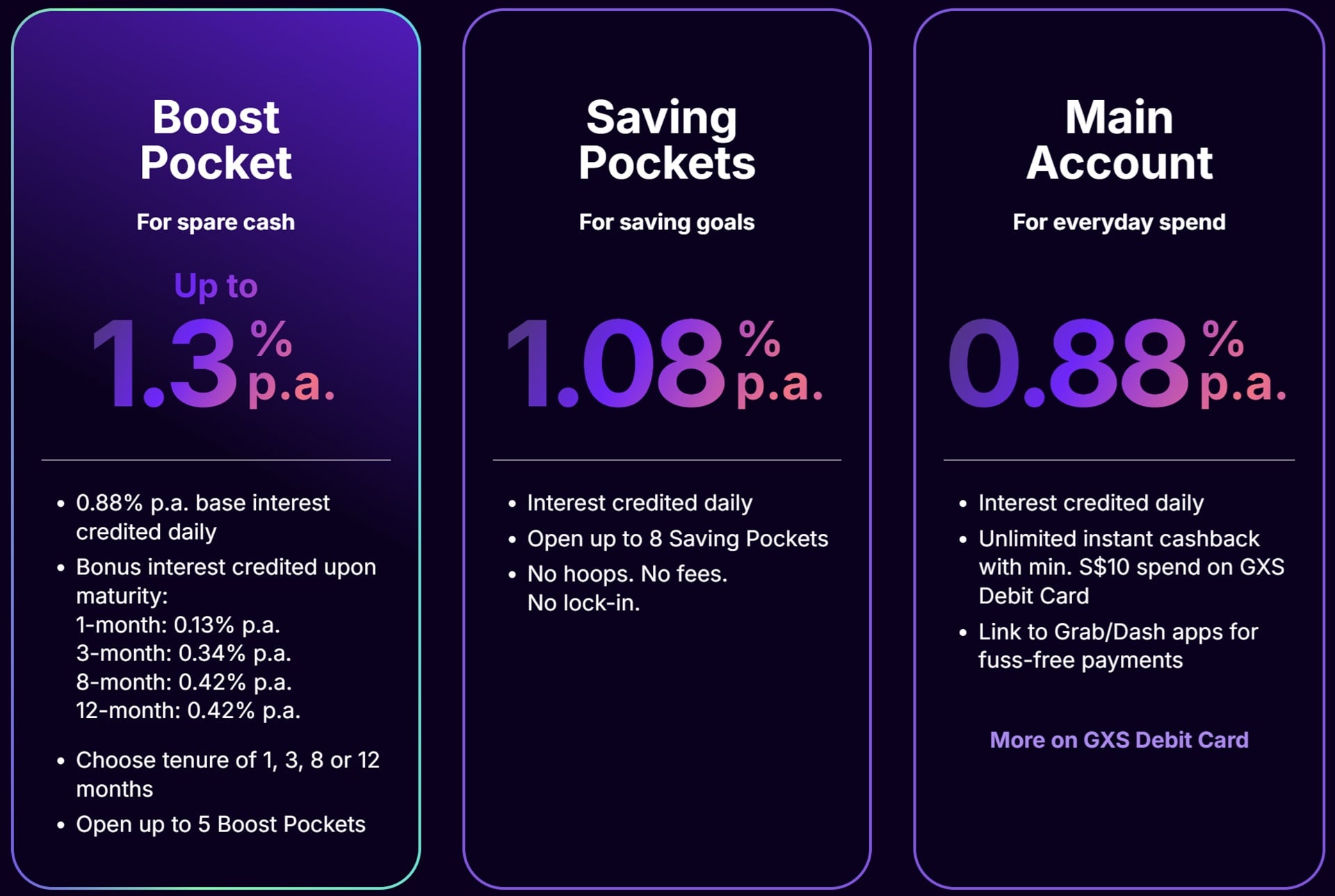

GXS Bank is a digital bank in Singapore designed to make saving simple, organised and rewarding. Instead of relying on traditional fixed deposits, GXS uses a pocket‑based system. Your main Savings Account holds your core balance, while Savings Pockets help you organise money for different goals. Boost Pockets are special pockets that offer promotional rewards for a fixed tenure, functioning like short‑term locked savings with bonus incentives. They are easy to set up and ideal for customers who want predictable returns without the complexity of investment products.

In April 2026, GXS launched the April Boost Campaign, a limited‑time promotion running from 8 April to 20 April. The campaign allows eligible customers to earn up to S$225 in cashback by opening specific Boost Pockets and depositing fresh funds. Both new and existing GXS Savings Account holders can participate, as long as they have not previously closed a GXS account and reopened a new one.

The campaign revolves around three April Boost Pocket tenures: three months, eight months and twelve months. Each tenure offers a different cashback reward. A customer who opens a three‑month April Boost Pocket and deposits at least S$20,000 in fresh funds can earn S$15. The eight‑month tenure offers S$60 with the same minimum deposit, while the twelve‑month tenure offers S$150. Completing all three pockets allows a customer to earn the full S$225.

To qualify for any cashback, the customer must open a brand‑new Boost Pocket named “April Boost” or “APRIL BOOST” during the campaign period. Renaming an existing pocket does not count. The customer must also maintain the Boost Pocket until it matures. Throughout the entire tenure, the customer’s total day‑end balance across the main account and all pockets must not fall below the balance recorded on the day the April Boost was opened. Fresh funds must come from outside GXS and must represent an increase over the customer’s total balance as of 31 March 2026.

If a customer opens multiple April Boost pockets but does not deposit enough fresh funds to meet all minimum requirements, GXS will allocate the funds starting from the shortest tenure first. This means that the three‑month pocket is fulfilled before the eight‑month pocket, and the eight‑month pocket before the twelve‑month pocket. To earn the full S$225, a total of S$60,000 in fresh funds is required.

Cashback is credited only after each Boost Pocket matures. The three‑month cashback will be paid by 31 August 2026, the eight‑month cashback by 31 January 2027 and the twelve‑month cashback by 31 May 2027. The customer’s GXS Savings Account must remain active and in good standing until the cashback is credited. If the account is closed early or the Boost Pocket is not maintained until maturity, any pending cashback will be forfeited. The campaign is limited to the first 1,000 successful customers, and each customer can earn only one cashback per tenure.

The April Boost Campaign becomes more interesting when viewed through the lens of annualised returns. Based on the minimum S$20,000 deposit required for each tenure, the three‑month pocket provides S$15, which works out to a 0.075 percent return over three months. Annualised, this is approximately 0.30 percent per year. The eight‑month pocket provides S$60, which is a 0.30 percent return over eight months, translating to roughly 0.45 percent per year. The twelve‑month pocket provides S$150, which is a 0.75 percent return over a full year, making it the highest‑yielding option among the three.

When compared with fixed deposits in Singapore, the picture becomes clearer. As of early 2026, most major banks offer fixed deposit rates ranging from about 1.30 to 1.45 percent per year for tenures between six and twelve months. Even promotional FD rates tend to stay within this range. Against these benchmarks, the April Boost returns are significantly lower. The twelve‑month Boost Pocket’s annualised return of 0.75 percent is only a fraction of what fixed deposits typically offer. The shorter‑tenure Boost Pockets fall even further behind.

The comparison with Singapore Treasury Bills is even more striking. Six‑month T‑bills in 2026 have generally been yielding between 1.39 and 1.47 percent per year, depending on auction demand. These instruments are backed by the Singapore Government and are considered extremely low risk. When placed side by side, the April Boost returns are modest. The three‑month and eight‑month pockets do not come close to matching T‑bill yields, and even the twelve‑month pocket remains far below.

GXS Savings Account April Boost Campaign

Despite this, the April Boost Campaign still has a place for certain savers. The cashback is guaranteed as long as the conditions are met, and the funds remain fully liquid within the GXS ecosystem. There are no lock‑in penalties beyond maintaining the required balance, and the process is entirely digital. For customers who prefer simplicity, do not wish to manage auction applications, or want a small bonus on top of their existing GXS savings, the campaign provides a straightforward, risk‑free boost. It is not meant to compete with fixed deposits or T‑bills on yield, but rather to reward customers who are already using GXS as their primary savings platform.

Since the promotion is capped at 1,000 successful customers and runs for a short period, early participation is essential for those who wish to secure the rewards.