Which is Singapore Best Savings Accounts in August 2025? Putting your money into a high-interest savings account in Singapore is a smart and low-risk way to grow your wealth while keeping it accessible. These savings products offer a significantly better return than regular savings accounts, which often yield less than 0.1%. High-interest savings accounts reward everyday financial activities like salary crediting, bill payments, and card spending by boosting your interest rates, effectively allowing your money to work harder without additional risk.

Which is Singapore Best Savings Accounts in August 2025? Putting your money into a high-interest savings account in Singapore is a smart and low-risk way to grow your wealth while keeping it accessible. These savings products offer a significantly better return than regular savings accounts, which often yield less than 0.1%. High-interest savings accounts reward everyday financial activities like salary crediting, bill payments, and card spending by boosting your interest rates, effectively allowing your money to work harder without additional risk.

High interest savings accounts ideal for building an emergency fund, saving for short to medium term goals, or simply parking idle cash in a place where it earns meaningful returns while remaining liquid and insured. In a rising interest rate environment, not taking advantage of these accounts means missing out on passive income with virtually no downside.

Below, I found some of the top high interest savings accounts in Singapore as of July 2025, helping you understand their features, requirements, and who they are best suited for. You may already own some of these high interest yielding savings account.

High interest yielding saving accounts incentivize specific banking behaviours to unlock higher rates. Common conditions include:

- Salary Crediting: Directing your monthly salary to the account.

- Credit Card Spending: Meeting a minimum monthly spend on an associated credit card.

- Bill Payments: Setting up recurring bill payments via GIRO.

- Balance Growth: Maintaining or increasing your average daily balance.

- Investments/Insurance: Purchasing investment or insurance products through the bank.

It is crucial to look beyond the “maximum advertised interest rate” and understand the effective interest rate (EIR) you can realistically achieve based on your banking habits.

Best Savings Accounts in Singapore in August 2025

Below, I have highlighted the potential maximum interest rates and typical requirements of some of the leading Singapore banks.

UOB Stash Savings Account

UOB Stash Account is my favourite savings account in Singapore because it is a simple, no-frills account whereby you do not need to fulfil multiple conditions to earn higher interests.

Maximum Interest Rate: Up to 2.04% per annum

Key Requirement: Maintain or increase your Monthly Average Balance (MAB).

Best For: Long-term savers who prefer a simpler approach and are good at consistently growing their savings without needing to meet transactional requirements.

OCBC 360 Savings Account

Maximum Interest Rate: Earn up to 2.45% a year on your first S$100,000 when you credit your salary, save and spend with OCBC. Earn an additional 3.00% a year when you insure and invest.

Key Requirements (to reach higher tiers):

- Salary credit (minimum S$1,800)

- Increase average daily balance (minimum S$500 increase monthly)

- Credit card spending (minimum S$500 on eligible OCBC cards)

- Optional: Insurance and/or investment purchases with OCBC.

Best For: Individuals who actively manage their finances, consistently credit their salary, and use OCBC credit cards for their daily spending. The tiered structure allows for good returns even if not all conditions are met.

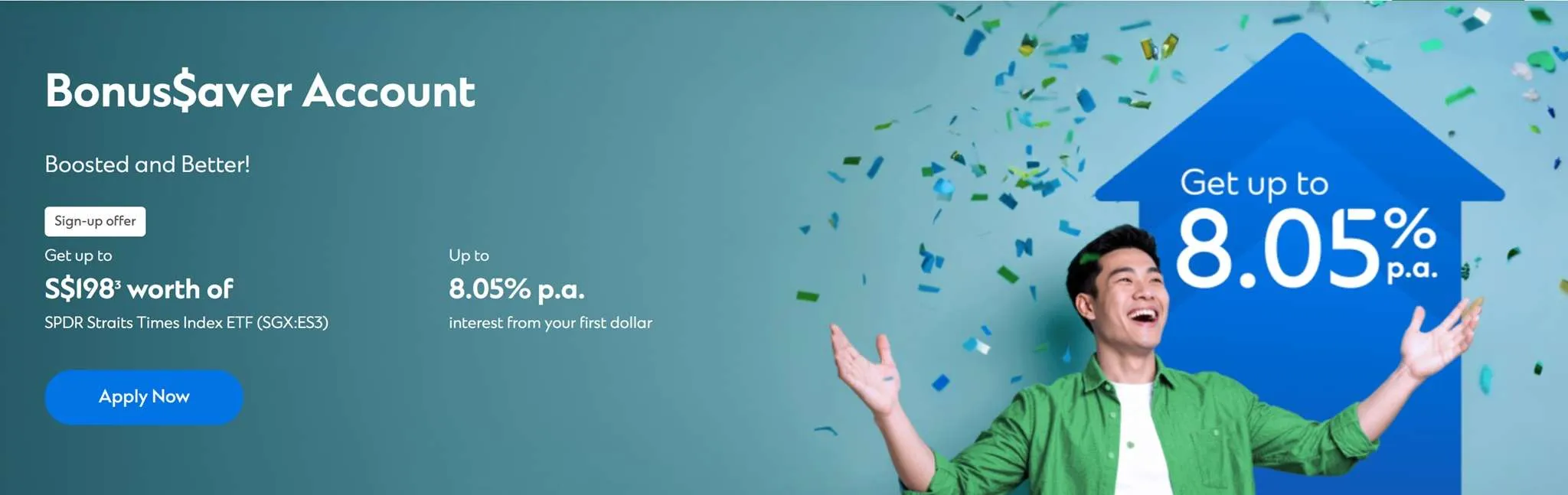

Standard Chartered Bonus$aver Savings Account

Maximum Interest Rate: Earn up to 8.05% per annum (on first S$100,000) when you credit your salary, spend, insure and invest with Standard Chartered.

Key Requirements (to reach higher tiers):

- Salary credit (minimum S$3,000)

- Credit card spending (minimum S$1000 on Bonus$aver Cards)

- Optional: Insurance and/or investment purchases with Standard Chartered.

Best For: High-income earners who are already investing or insuring through Standard Chartered or are looking to consolidate their banking and wealth management with one institution.

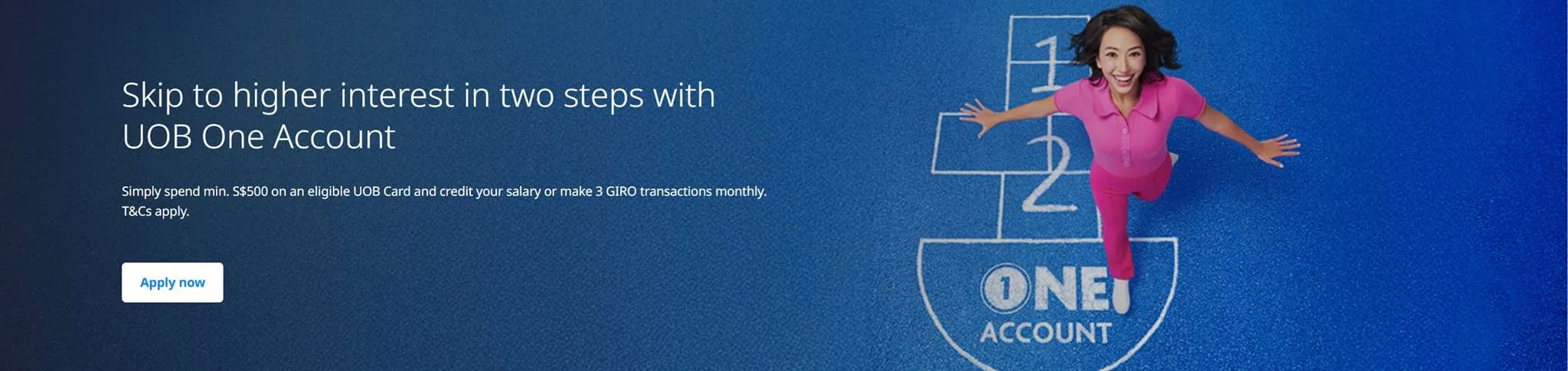

UOB One Savings Account

Maximum Interest Rate: Up to 5.30% per annum (on first S$150,000)

Key Requirements (to reach higher tiers):

- Salary credit (minimum S$1,600) or 3 GIRO payments monthly.

- Minimum S$500 spend on eligible UOB One Card or other UOB cards.

Best For: Salaried individuals who regularly use a UOB credit card for their expenses. It is known for having relatively straightforward conditions to unlock good interest rates.

DBS Multiplier Savings Account

Maximum Interest Rate: Up to 4.10% per annum (on first S$100,000)

Key Requirements (to reach higher tiers):

- Credit income (salary/dividends).

- Transact in at least one other category: Spend (DBS/POSB credit cards), Insure (selected products), Invest (selected products), or Home Loan.

Best For: Existing DBS/POSB customers who conduct multiple banking activities with the bank. Its flexibility across various transaction categories makes it accessible for many.

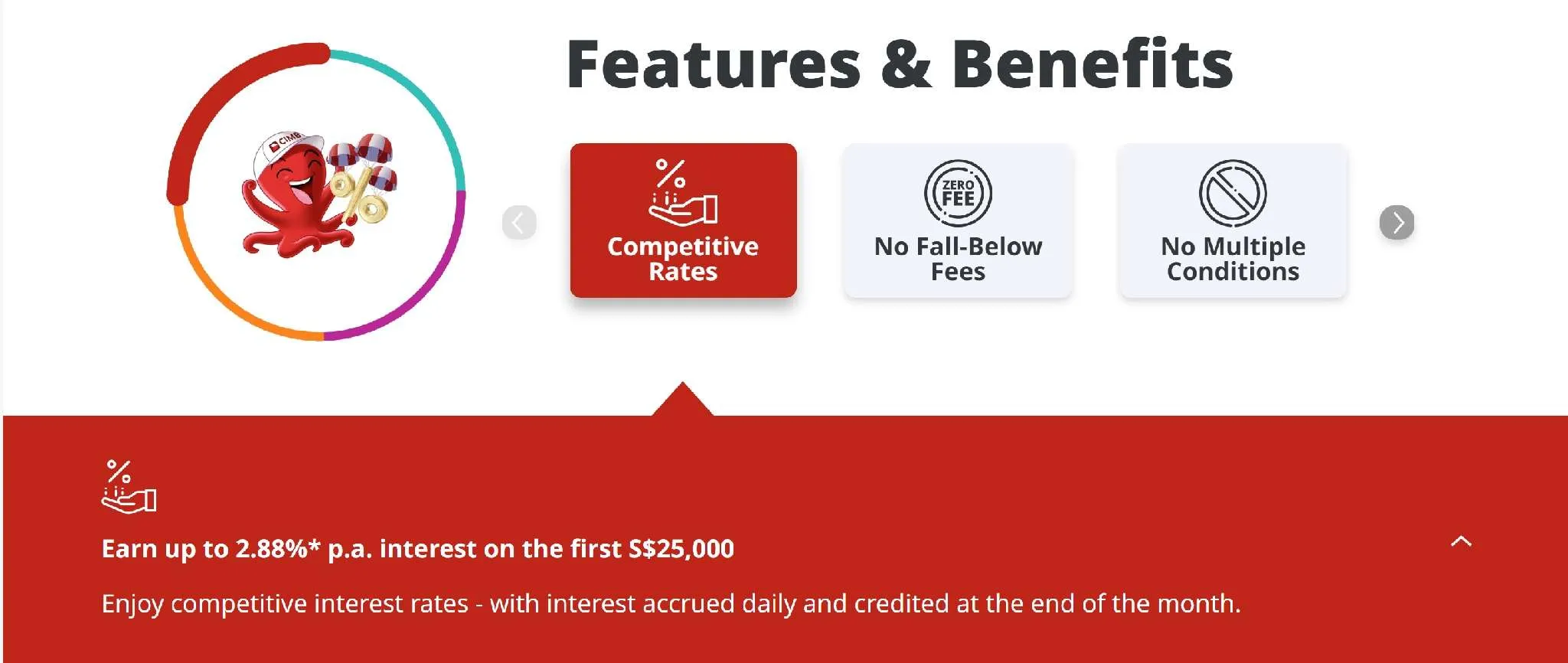

CIMB FastSaver Account

Maximum Interest Rate: Up to 2.88% per annum (on first S$25,000)

Key Features:

- Offers competitive base interest without needing to meet additional criteria.

- No fall-below fees.

- Additional interest can be earned with salary credit or recurring transfers, and credit card spend.

Best For: Those seeking a fuss-free savings account with a decent base interest rate, especially for smaller balances. It’s a good option if you prefer not to juggle multiple conditions.

Trust Savings Account

Maximum Interest Rate: Up to 2.0% per annum (on first S$1.2 million)

Key Requirements (to reach higher tiers):

- Base rate + Bonus for minimum card transactions (e.g., 5 x S$30 qualifying transactions).

- Bonus for maintaining minimum Average Daily Balance (ADB).

- Bonus for salary crediting.

Best For: Customers comfortable with digital banking and looking for an account that offers good returns on higher balances, coupled with benefits for FairPrice Group purchases.

Summary of the Best Savings Accounts in August 2025

High interest savings accounts in Singapore offer a compelling way to boost your savings in a relatively low-risk environment. By understanding your own financial habits and carefully comparing the offerings from various banks, you can choose a high interest bank account in Singapore that truly maximizes your returns.

You should consider the following factors when choosing a high interest bank savings account in Singapore from any of the above list.

Your Banking Habits: Honestly assess if you can consistently meet the requirements (salary crediting, spending, etc.) to unlock the higher interest tiers.

Deposit Amount: Some savings accounts offer the best rates on specific balance tiers (e.g. first S$100,000). Consider how much you plan to save.

“Realistic” vs. “Maximum” Interest: Focus on the Effective Interest Rate (EIR) you’re likely to achieve, not just the highest advertised rate, which often requires fulfilling all conditions.

Hidden Fees/Conditions: Check for fall-below fees, monthly service charges, or other caveats.

Ease of Management: Consider how easy it is to track your progress towards earning bonus interest (e.g. via mobile banking apps).

Bank’s Ecosystem: If you already use certain banks for credit cards, loans, or investments, leveraging their integrated savings accounts might be more convenient.

Out of the above list of high interest bank account in Singapore, I have DBS Multiplier, UOB Stash Account, CIMB Fast Saver and OCBC 360 Account. I am looking at opening a UOB One Savings Account to earn up to 5.30% per annum for the first S$150,000 I am going to deposit in.

As usual, I like to highlight that this is not a sponsored post and solely based on my own research and opinion. With falling interest rates, I believe everyone like me is looking for the best place to park your money to earn extra cash.

Last, remember to regularly review your account’s performance and the bank’s terms and conditions, as interest rates and requirements can change over time. Please help to share this post with your friends so that we can grow our savings together!

Yo, UOB 1 account nerf from 1 sept leh. And it is not 5.3% effective interest rate for first 150k. It is up to 5.3%.

Yo , UOB 1 account nerf from 1sept

Thanks for letting me know. I noted that the third tier will be revised to 4.5% per annum.