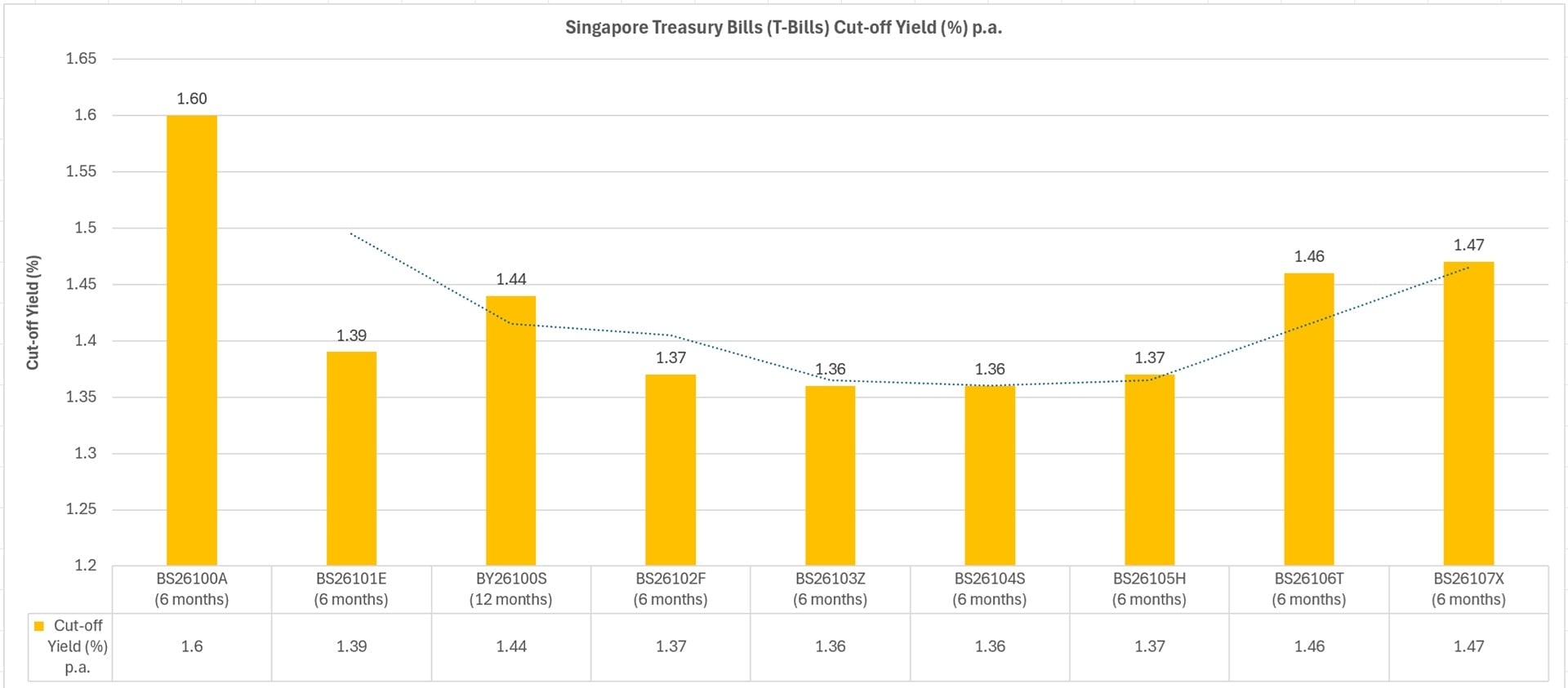

The latest 6‑month T Bill Singapore auction (BS26107X) closed with a cut‑off yield of 1.47% per annum, marking another step in the gradual upward drift in short‑term government securities. This rate reflects investors’ growing demand for safer instruments amid global uncertainty, as well as the spillover from rising international bond yields. Compared with earlier auctions this year where yields hovered around 1.36% to 1.39%, the 1.47% result signals a meaningful improvement in returns for cash‑management investors seeking stability without sacrificing too much yield.

For those new to T‑bills, Singapore Treasury Bills are short‑term government securities issued to meet the nation’s financing needs. They are sold at a discount and mature in 3, 6, or 12 months, making them a popular option for parking short‑term cash. Backed by the Singapore government’s strong credit rating, T‑bills are widely viewed as one of the safest low‑risk investments available to Singapore investors. In 2025, I collected a total passive income of $20,289.89. A small portion of my passive income comes from investing my spare cash into Singapore Treasury Bills (T bill).

Over the past few months, Singapore T‑bill yields have been edging higher in tandem with global rate expectations. For instance, the 6‑month T‑bill cut‑off yield climbed from 1.36% in late February to 1.46% in the 26 March auction, before reaching 1.47% in the most recent issue. These movements mirror shifts in US Federal Reserve expectations and geopolitical tensions, both of which have pushed global bond yields upward and filtered into Singapore’s risk‑free curve.

The upward trend is not limited to the 6‑month tenor. One‑year T‑bill yields have also strengthened, with recent closing yields around 1.44%, close to their latest auction levels. This consistency across tenors suggests that investors are pricing in a sustained period of elevated short‑term rates rather than a temporary spike. Elevated demand for T‑bills driven by their safety and liquidity has kept yields from rising even faster, but the general direction remains upward. With global uncertainty persisting and rate‑cut expectations shifting, Singapore T‑bills may continue to see firm demand and competitive yields in upcoming auctions.

Investors can buy Singapore Treasury Bills either directly from the Singapore government or through participating banks and financial institutions. As a low‑risk and highly liquid instrument, T‑bills are commonly used by investors who want a predictable, fixed return for short‑term cash management.

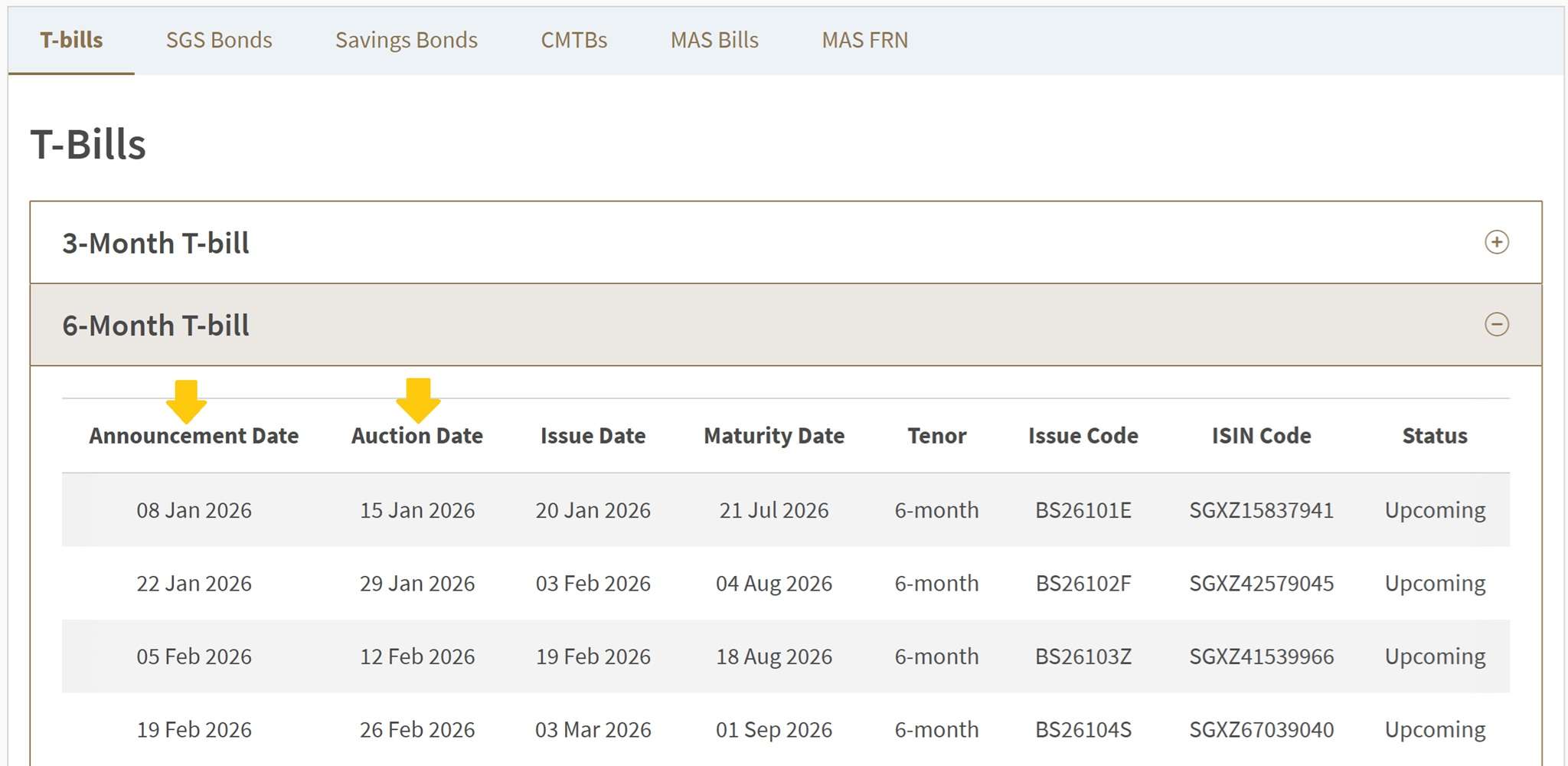

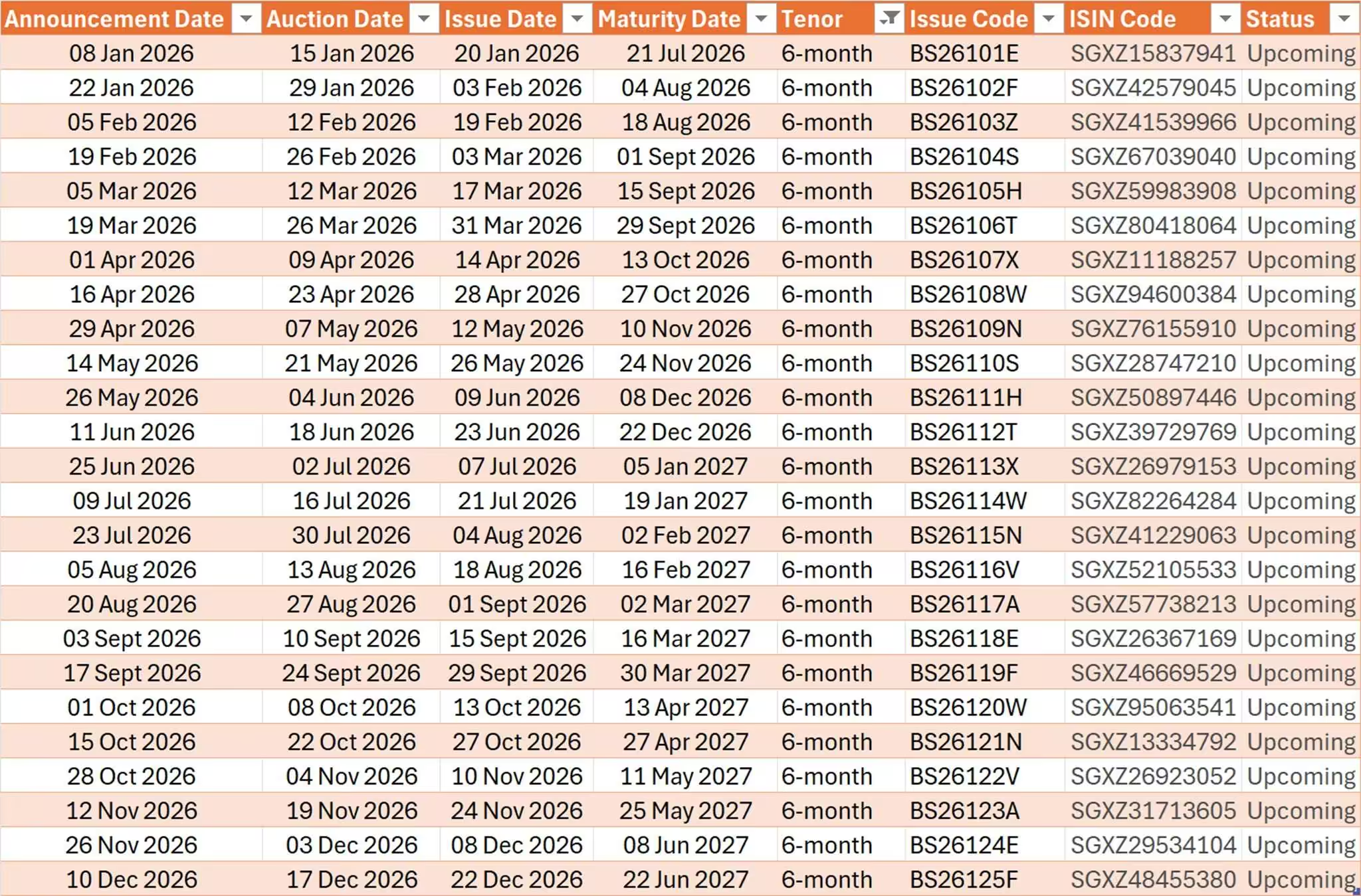

T Bill Singapore 2026 Calendar

Key dates, such as the announcement date and auction date for each T Bill Singapore issuance are published on the Monetary Authority of Singapore (MAS) website under the Auctions and Issuance Calendar.

For convenience, I am sharing the Singapore Treasury Bills (T-Bills) Auction and Issuance Calendar here. If you need the Treasury Bill results such as the status of each issuance, please refer to Treasury Bills at MAS website – Auctions and Issuance Calendar.

Six Months T Bill Calendar

One Year T Bill Calendar

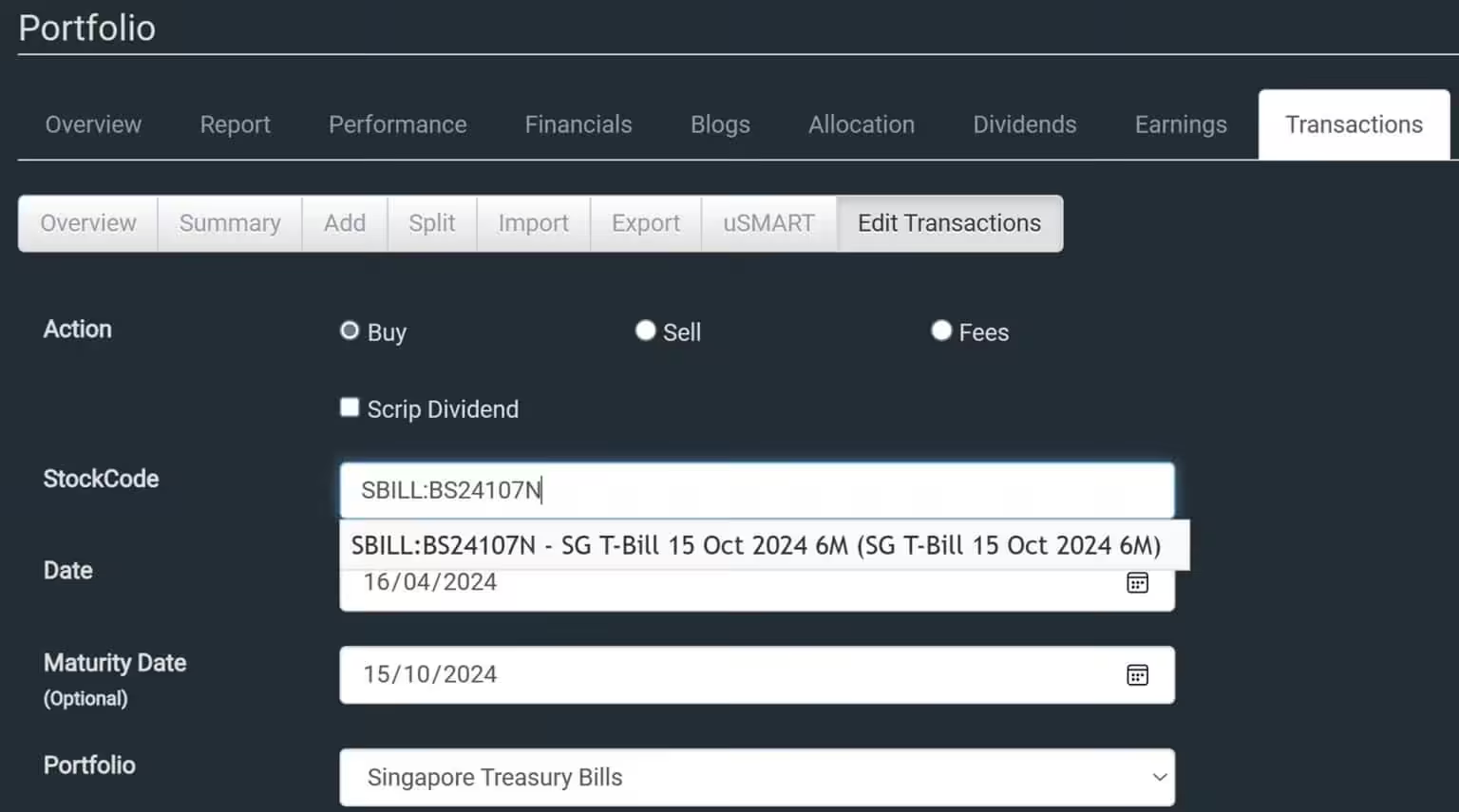

How I Track My Singapore Treasury Bills (T-Bills)

Stocks Café is probably the only software that I know which allows you to track your purchased Singapore Savings Bonds and Treasury Bills (T-Bills) all in one place together with your stock investments. This makes it easy to track your total net investments.

Stocks Café allows you to create portfolios. You can use portfolio to different your investments. For example, I created three portfolios in Stocks Café, namely Stocks, Singapore Savings Bonds and Treasury Bills. This allow me to categorize how much I allocate for each investment.

How To Buy T Bill Singapore?

Singapore Treasury Bills can be purchased either with cash, CPF Ordinary Account funds, or SRS savings, and the process is designed to be straightforward for individual investors. You begin by applying through internet banking with any of the three local banks DBS, OCBC, or UOB. You can also submit an application at an ATM if you prefer an offline method.

Applications must be submitted before each bank’s cut-off time, which is typically one business day before the auction. When you apply, you choose between a competitive bid, where you specify the yield, you are willing to accept, or a non-competitive bid, where you accept the eventual cut-off yield determined at auction. T bills are issued at a discount, meaning you pay less upfront and receive the full-face value at maturity.

Once the auction concludes, you can check your allocation results through your bank’s platform. If your bid is successful, the purchase amount is deducted from your bank account, CPF-OA, or SRS accordingly. The T-bill will then appear in your CDP account if purchased with cash, or in your CPF/SRS statement if purchased using those funds. At maturity, either six months or one year depending on the tenor, the government pays you the full-face value, and your return is simply the difference between what you paid and what you receive.

Banks like DBS also provide step-by-step guidance on their platforms to help you navigate the application process smoothly.

I Invest in T Bills Using My SRS

In December 2025, I deployed my entire SRS balance into Singapore Treasury Bills, using them as a stable and tax‑efficient anchor for my retirement planning. Since idle SRS funds earn just 0.05% per year, shifting them into T‑bills allows me to capture meaningfully higher short‑term yields backed by the Singapore Government’s top‑tier credit rating. This makes T‑bills an attractive low‑risk instrument that preserves capital while delivering predictable returns, ideal for investors who want steady growth without the volatility that comes with equities or long‑duration bonds.

A major advantage of using T‑bills within the SRS framework is the clarity and simplicity of the returns. Because T‑bills are issued at a discount and redeemed at face value, the gain is transparent and easy to calculate. This structure suits conservative investors and those who prioritise tax‑efficient planning, especially when building a retirement portfolio that emphasises stability over speculation.

Flexibility is another key benefit. Unlike long‑term investments that may lock up capital or expose you to market swings, six‑month and one‑year T‑bills allow for regular reinvestment based on prevailing interest rates. This rolling approach gives investors the agility to respond to changing market conditions while keeping risk low. It also aligns well with the deferred‑tax nature of SRS, where gains compound tax‑deferred and withdrawals in retirement may be taxed at a lower effective rate.

By pairing the tax relief from SRS contributions with the safety and yield of Singapore T‑bills, investors can build a disciplined, low‑risk strategy that steadily compounds over time. This combination strengthens the foundation of a retirement portfolio, maintains liquidity, and ensures that every dollar in the SRS account works harder instead of sitting idle.