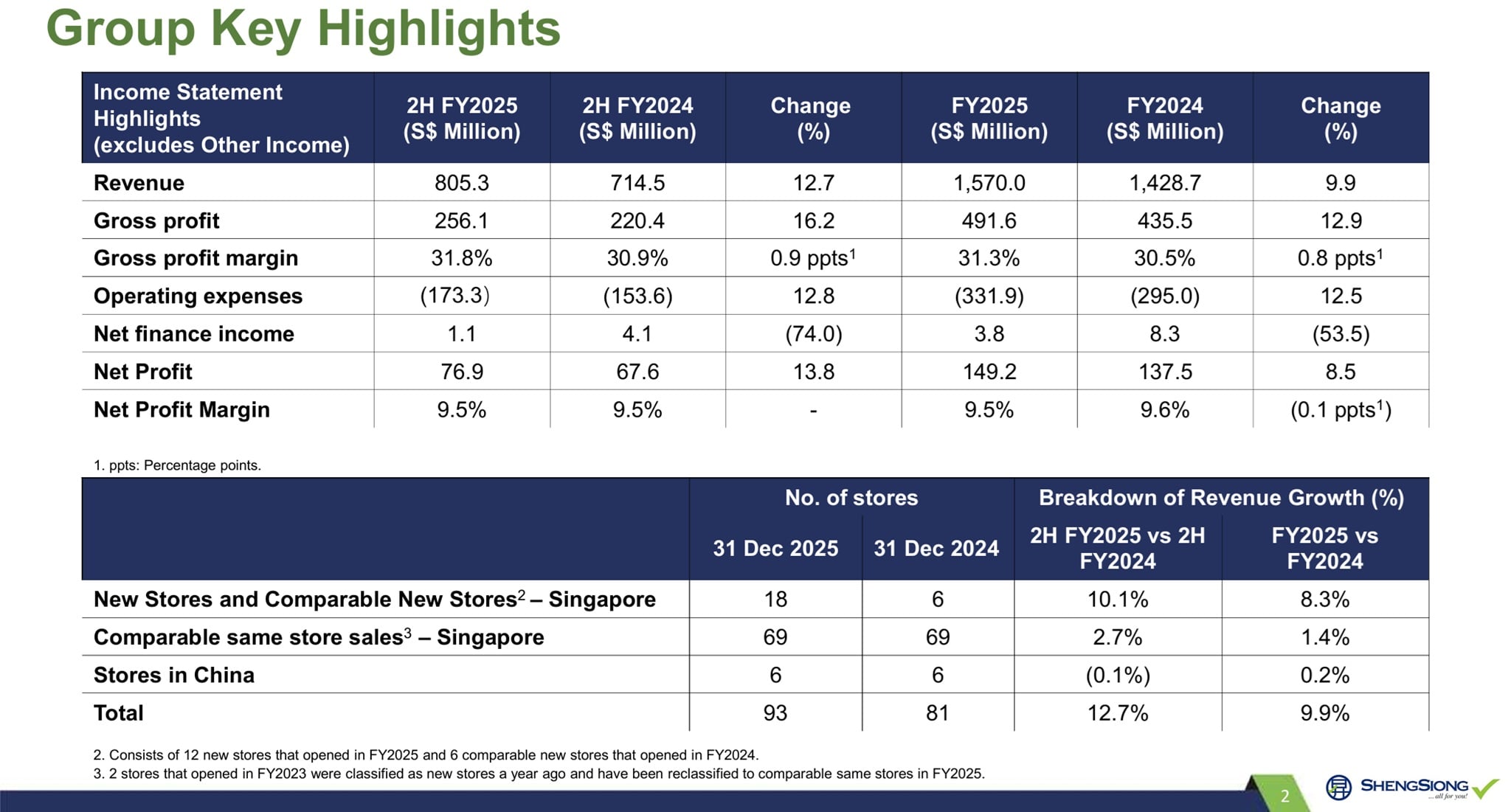

Sheng Siong Group delivered a solid set of results for the second half of FY2025, supported by strong revenue growth, disciplined cost management, and an expanding retail footprint across Singapore. Despite a cautious consumer environment and rising operating costs, the supermarket operator maintained stable profitability and strengthened its financial position, reinforcing its reputation as one of Singapore’s most resilient grocery retailers. Sheng Siong announced a final dividend of 3.80 cents per share, making up a total dividend of 7.00 cents per share for FY2025.

Revenue for 2H FY2025 rose 12.7 percent year‑on‑year to S$805.3 million, compared to S$714.5 million in the same period last year. For the full year, revenue increased 9.9 percent to S$1.57 billion. This performance was supported by contributions from twelve new stores opened in FY2025 and six comparable new stores opened in FY2024, which together lifted Singapore sales by 10.1 percent in the second half. Comparable same‑store sales also improved by 2.7 percent, reflecting steady demand from existing outlets.

Margins Remain Stable as Gross Profit Strengthens

Gross profit for 2H FY2025 increased to S$256.1 million, up from S$220.4 million a year earlier. Gross margin improved to 31.8 percent, compared to 30.9 percent previously. Net profit rose 13.8 percent to S$76.9 million, maintaining a net margin of 9.5 percent. While net finance income declined due to lower interest rates, the core supermarket business continued to demonstrate strong operational resilience.

Retail Network Expands to 93 Stores

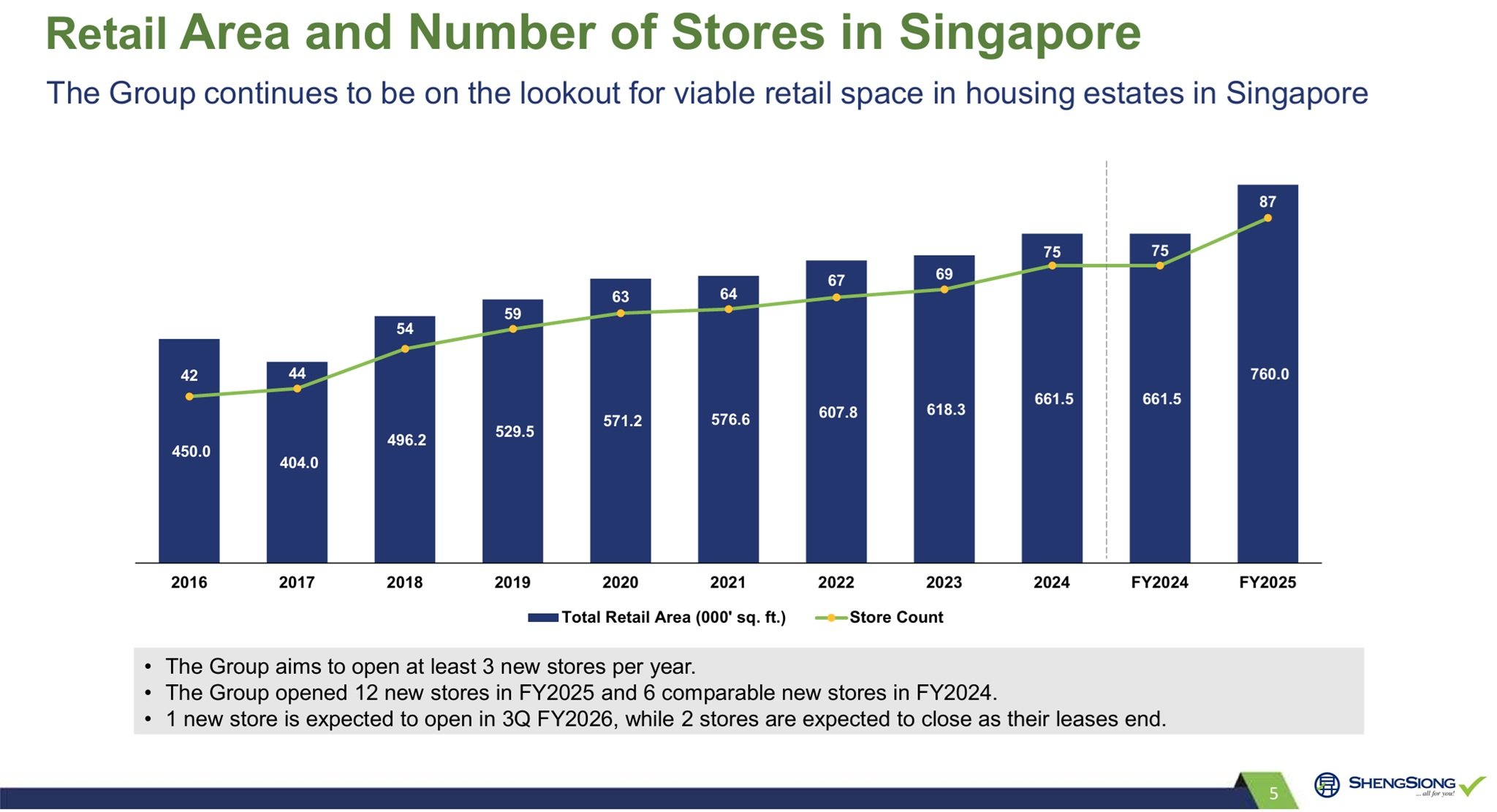

Sheng Siong ended FY2025 with ninety‑three stores, up from eighty‑one the year before. Six stores in China remained unchanged. Total retail area grew to 760,000 square feet, the largest footprint in the company’s history. The Group continues to pursue new opportunities in HDB estates, with four stores pending results, three currently open for bidding, and two more expected to open for tender in the second half of 2026. Two stores, at Elias Mall and Thomson Imperial Court, will close in 2026 as their leases expire.

Revenue Productivity Remains Healthy Despite Rapid Expansion

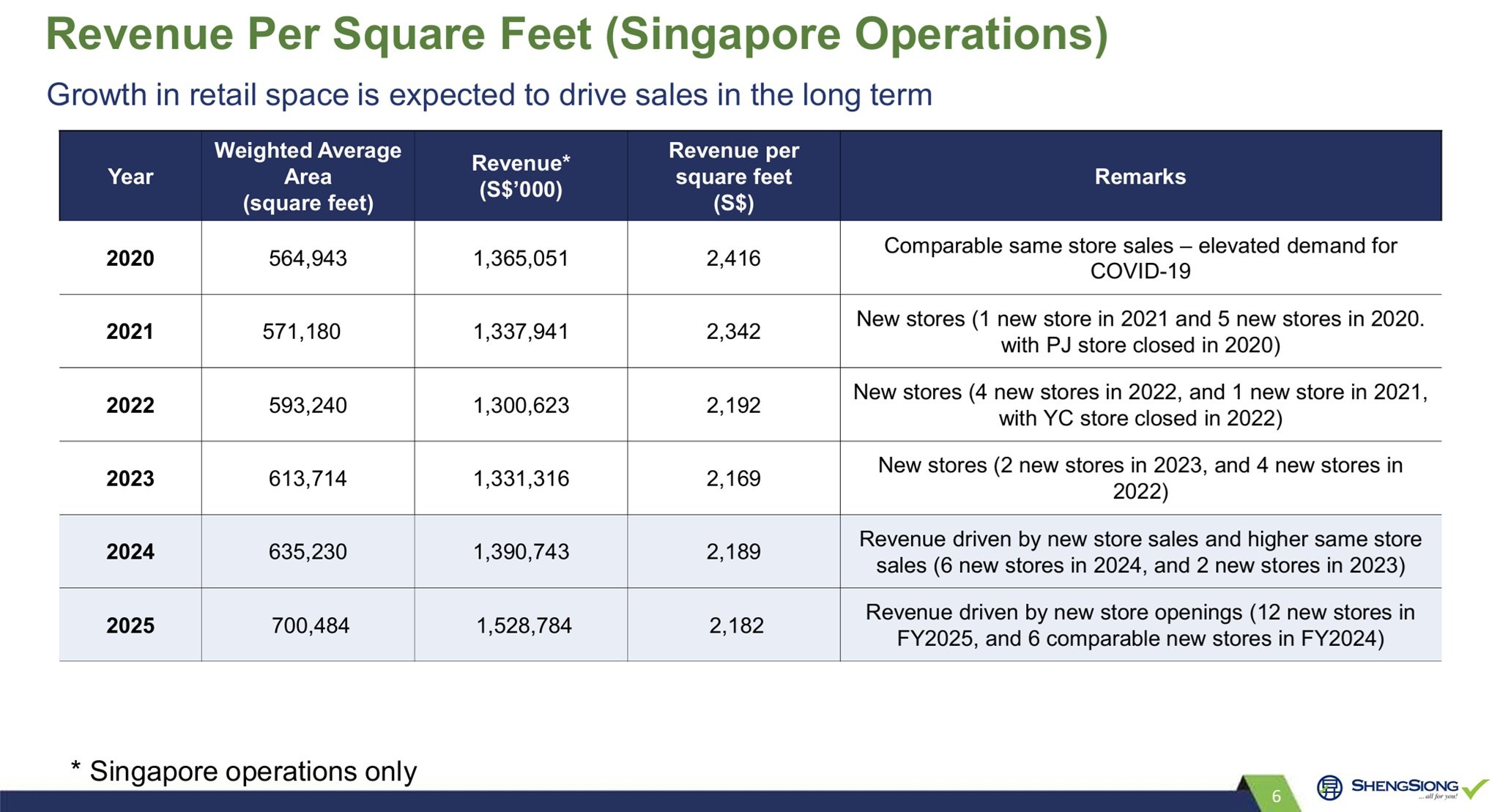

Revenue per square foot for Singapore operations remained stable at S$2,182 in FY2025. This reflects the Group’s ability to ramp up new stores efficiently while maintaining strong sales momentum across its network. The increase in retail area is expected to support long‑term revenue growth as new stores mature.

Balance Sheet Strengthened by High Cash Reserves and Zero Borrowings

Sheng Siong continues to operate with no borrowings and a strong cash position. Cash and cash equivalents rose to S$353.4 million in FY2025, up from S$324.4 million the previous year. Net assets increased to S$591.1 million, underscoring the Group’s financial resilience and capacity to fund future expansion.

China Operations Remain Modest but Strategic

China contributed 2.4 percent of total revenue in FY2025. The segment recorded a deficit due to higher operating expenses from the sixth store, which opened in FY2024. The Group remains committed to nurturing its presence in Kunming and building brand recognition in the region.

Outlook for 2026: Expansion, Efficiency, and Margin Protection

Looking ahead, Sheng Siong expects consumer spending to remain cautious amid high living costs, though Budget 2026 support measures should help sustain demand for essential goods. The Group plans to enhance its sales mix by increasing the range of higher‑margin products and expanding its house‑brand offerings. Ongoing automation initiatives and the new Sungei Kadut distribution centre, which can support up to 120 supermarkets, are expected to improve operational efficiency and support long‑term growth.

Summary of Sheng Siong 2HFY2025 Results

Sheng Siong’s 2HFY2025 results highlight a business that continues to execute well despite macroeconomic challenges. With strong cash reserves, stable margins, and a robust pipeline of new stores, the Group is well‑positioned to deliver sustainable growth in the years ahead. Its disciplined approach to expansion and operational efficiency remains a key competitive advantage in Singapore’s highly competitive supermarket landscape.

Based on the Sheng Siong’s business updates, the pros are:

- Strong revenue growth driven by new store openings, with 2H FY2025 revenue rising 12.7% year‑on‑year and full‑year revenue reaching S$1.57 billion.

- Improved gross margin, increasing to 31.8% in 2H FY2025 from 30.9% a year earlier, showing effective cost and product mix management.

- Healthy net profit growth, with 2H FY2025 net profit up 13.8% to S$76.9 million while maintaining a stable 9.5% net margin.

- Aggressive store expansion, ending FY2025 with 93 stores and a record 760,000 sq ft of retail space, strengthening long‑term revenue potential.

- Strong balance sheet with zero borrowings and a high cash balance of S$353.4 million, providing flexibility for future expansion.

- Stable revenue productivity, with revenue per square foot at S$2,182 despite rapid network growth.

- Operational efficiency initiatives such as automation and the new Sungei Kadut distribution centre, which can support up to 120 stores.

The cons are:

- Lower net finance income, declining sharply due to reduced interest rates, which softened overall profit growth.

- China operations remain loss‑making, with higher operating expenses from the sixth store dragging performance despite contributing 2.4% of total revenue.

- Rising operating expenses, including staff costs and promotions, continue to pressure margins in a competitive supermarket landscape.

- Cautious consumer sentiment expected to persist in 2026 due to high living costs, potentially limiting same‑store sales growth.

- Two store closures planned for 2026 (Elias Mall and Thomson Imperial Court) due to lease expiries, slightly offsetting expansion momentum