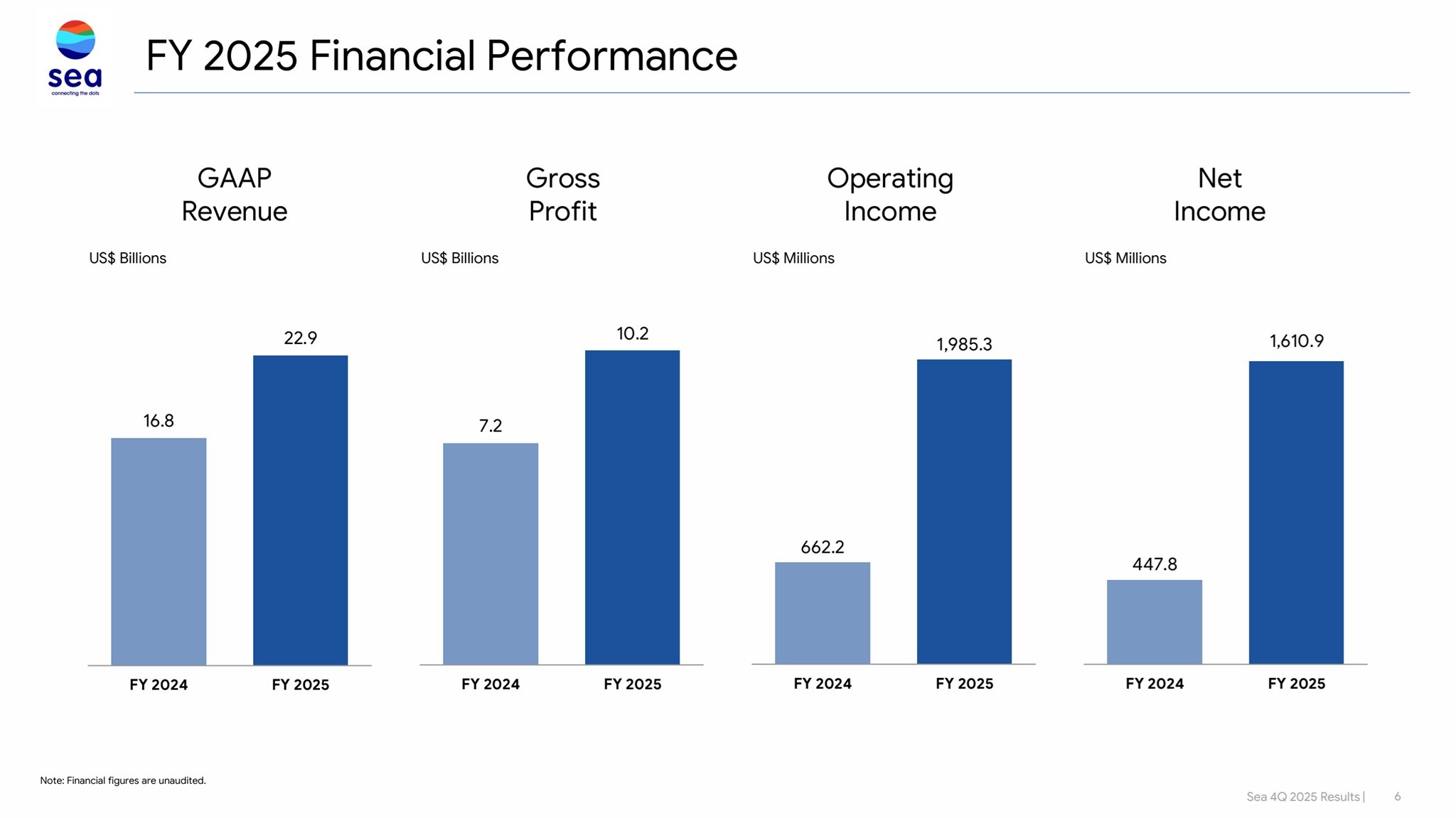

Sea Limited reported US$6.9 billion in Q4 revenue, up 38.4% year-on-year, and US$22.9 billion for the full year, a 36.4% increase. The company also delivered US$3.0 billion in Q4 gross profit and US$10.2 billion for the full year, reflecting strong operating leverage across its ecosystem.

Sea Limited reported US$6.9 billion in Q4 revenue, up 38.4% year-on-year, and US$22.9 billion for the full year, a 36.4% increase. The company also delivered US$3.0 billion in Q4 gross profit and US$10.2 billion for the full year, reflecting strong operating leverage across its ecosystem.

The company’s net income jumped dramatically, reaching US$410.9 million in Q4 and US$1.6 billion for the full year, compared to just US$447.8 million in 2024. This represents a 259.7% year-on-year increase, showing that Sea has transitioned decisively into a profitable, scaled business.

Shopee continued to anchor the group’s performance. The platform generated US$16.6 billion in GAAP revenue for 2025, up 33.4%, and delivered US$880.6 million in adjusted EBITDA, a massive improvement from US$155.8 million in 2024. The company highlighted that Shopee served 400 million active buyers and 20 million sellers in 2025, demonstrating its dominance in Southeast Asia and Brazil.

Monee, Sea’s digital financial services arm, also posted exceptional growth. Its GAAP revenue rose 60.1% to US$3.8 billion, while adjusted EBITDA exceeded US$1 billion. Loans outstanding reached US$9.2 billion, up 80.4%, with a stable 1.1% NPL90+ ratio, showing disciplined risk management even as the business scaled aggressively.

Garena, long seen as the company’s cash engine, delivered a strong rebound. Bookings grew 37.3% to US$2.9 billion, driven largely by Free Fire’s resurgence and new content collaborations. Quarterly paying users increased 15%, and average bookings per user rose from US$0.88 to US$1.06.

Across all segments, Sea’s total adjusted EBITDA doubled to US$3.4 billion, reflecting a business that is not only growing but doing so profitably.

If the Results Were So Strong, Why Did Sea’s Stock Price Crash?

Despite the impressive numbers, the market reacted negatively and the reasons lie in expectations, forward guidance, and the underlying cost structure.

Slower Growth Guidance for 2026

Sea guided Shopee’s 2026 GMV growth at around 25%, which is healthy but lower than the 27% to 30% range investors had hoped for. With e-commerce valuations heavily tied to growth momentum, even a slight deceleration can trigger a sell-off.

Rising Costs and Margin Pressure

While revenue grew strongly, several cost lines rose even faster:

- Sales and marketing expenses increased 29.4% for the full year to US$4.5 billion.

- Provision for credit losses surged 76.7% to US$1.4 billion, reflecting the rapid expansion of Monee’s loan book.

- Logistics costs for Shopee grew sharply, pushing cost of service up 32.6% for the year.

Investors worry that Sea may need to keep spending aggressively to maintain growth, especially in competitive markets like Brazil and Indonesia.

Garena’s Sequential Decline

Although Garena posted strong year-on-year growth, bookings fell 20% quarter-on-quarter in Q4. This raised concerns about sustainability, especially since Free Fire remains the primary driver of Garena’s performance.

Market Expectations Were Too High

Sea’s stock had rallied significantly ahead of earnings. When expectations are elevated, even strong results can disappoint if they don’t exceed the market’s bullish assumptions.

What This Means for Investors

Sea Limited is no longer the cash-burning growth story it once was. It is now a profitable, diversified tech ecosystem with strong positions in e-commerce, digital finance, and gaming. However, the stock’s volatility reflects the tension between its long-term potential and the near-term challenges of scaling sustainably.

Should You Invest in Sea Limited?

Sea Limited’s 2025 results show a company firing on all cylinders, but the market’s reaction highlights the risks that come with its aggressive expansion strategy. Here is a balanced view based on the latest financials:

The pros are:

Sea delivered strong revenue growth, expanding profitability, and robust performance across Shopee, Monee, and Garena. Shopee’s monetization improved significantly, Monee scaled while maintaining stable credit quality, and Garena showed renewed strength with Free Fire’s resurgence. The company also generated over US$3.4 billion in adjusted EBITDA, demonstrating real operating leverage.

The cons are:

The company faces rising costs, particularly in logistics, marketing, and credit provisions. Growth guidance for 2026 is solid but not spectacular, which disappointed investors expecting acceleration. Garena’s quarter-on-quarter decline raised questions about the durability of its gaming rebound. With competition intensifying in both e-commerce and fintech, Sea may need to keep spending heavily to defend market share.

Sea Limited remains a compelling long-term story, but investors should be prepared for volatility as the company balances growth, profitability, and competitive pressures.