On 25th April 2025, MPACT (Mapletree Pan Asia Commercial Trust) released their 4QFY24/25 financial results. MPACT is undergoing headwinds due to its underperforming assets in China and high finance costs due to higher interest rates on SGD, HKD and JPY borrowings. Mapletree Pan Asia Commercial Trust (MPACT) currently makes up 6.58% of my stock portfolio.

This is the 4th quarter financial results, which makes up the full year. How has Mapletree Pan Asia Commercial Trust performed in FY24/25? Let us find out below.

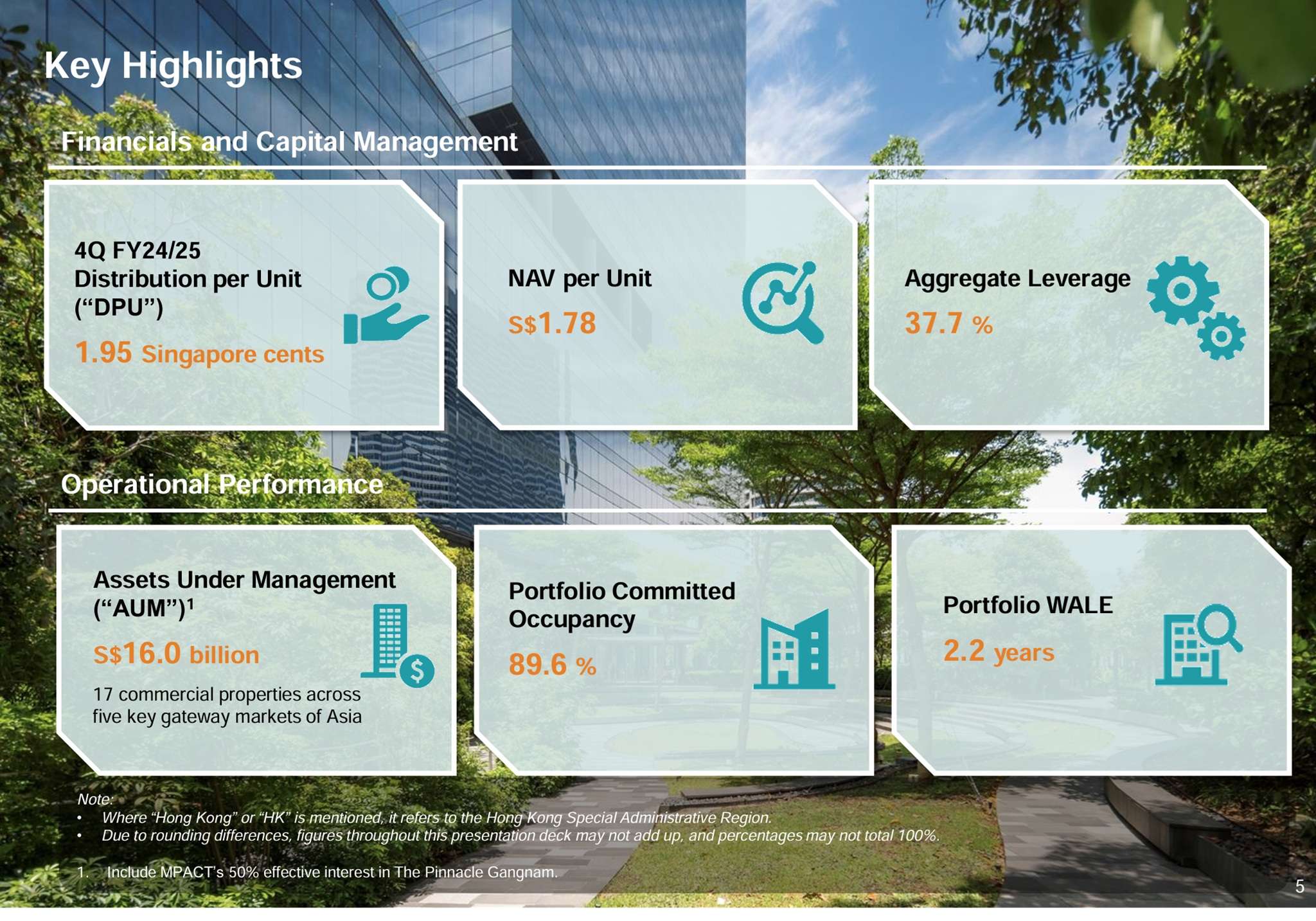

MPACT 4QFY24/25 Financial Results

In 4QFY24/25, MPACT’s Gross Revenue was 6.8% lower year-on-year. The decline was mainly attributed to the reduced contribution from Singapore properties due to divestment of Mapletree Anson on 31 July 2024 and lower overseas contributions.

Property expenses were lower also because of the divestment of Mapletree Anson, resulting in lower utility expenses.

Finance costs were lower as the net proceeds from Mapletree Anson’s divestment were deployed towards debt reduction. However, these were partially offset by higher interest rates on HKD and JPY borrowings.

Distribution Per Unit (DPU) was lower 14.8% year-on-year as a result of lower overseas contributions. These were mitigated by the stable contribution from MPACT’s Singapore properties.

| 4QFY24/25 (S$’000) |

4QFY23/24 (S$’000) |

% Change | |

| Gross Revenue | 222,894 | 239,222 | (6.8) |

| Net Property Income | 169,545 | 183,135 | (7.4) |

| Property expenses |

(53,349) | (56,087) | 4.9 |

| Net Finance Costs |

(51,123) | (56,434) | 9.4 |

| Amount Distributable to Unitholders | 103,620 | 120,522 | (14.0) |

| Distribution Per Unit (“DPU”) (cents) | 1.95 | 2.29 | (14.8) |

MPACT Full Year FY24/25 Financial Results

The reasons for the decline in Gross Revenue are similar to what was shared above. Thus, I shall not be repeating them.

MPACT’s full year Distribution Per Unit (DPU) for FY24/25 fell 10.0% to 8.02 cents as compared to 8.91 cents in FY23/24.

| FY24/25 (S$’000) |

FY23/24 (S$’000) |

% Change | |

| Gross Revenue | 908,841 | 958,088 | (5.1) |

| Net Property Income | 683,537 | 727,929 | (6.1) |

| Property expenses |

(225,304) | (230,159) | 2.1 |

| Net Finance Costs |

(218,382) | (225,482) | 3.1 |

| Amount Distributable to Unitholders | 423,022 | 468,569 | (9.7) |

| Distribution Per Unit (“DPU”) (cents) | 8.02 | 8.91 | (10.0) |

Debt

As of 31st March 2025, MPACT’s aggregate leverage stood at 37.7%. Aggregate leverage, also known as gearing ratio, refers to the ratio of a real estate investment trust’s (REIT) debt to its total assets.

As you can see from the above chart, MPACT has a well-distributed debt maturity profile with no more than 23% debt due in any financial year. There is also ample liquidity of estimated S$1.2 billion of cash and undrawn facilities.

What are the benefits of having a well-staggered debt maturity profile? Having a well-staggered debt maturity profile is crucial for REITs to manage their debt obligations effectively. By spreading out debt repayments over different time periods, REITs can avoid liquidity crunches and reduce the risk of default.

Furthermore, a well-staggered debt maturity profile allows REITs to take advantage of changes in interest rates. For example, if interest rates drop, REITs with debt maturing in the future can refinance at lower rates, reducing their interest expenses.

Overall, maintaining a well-staggered debt maturity profile is a sound financial strategy that can help ensure the long-term sustainability of the REIT’s finances.

Occupancy

MPACT’s overall portfolio occupancy stood at 89.6%. While occupancy at China Properties crept up, the occupancy at Japan Properties fell to 79.8%.

Next, let us take a look at the rental reversion. Do you know what is rental reversion? Rental reversion refers to the change in rental rates when leases are renewed. A positive rental reversion means the new rental rate is higher than the previous rate. A negative rental reversion happens when the new rental rate is lower than the previous rate. Whether the rental reversion is positive or negative depends on the market demand and supply.

Despite negative rental reversions at its China and Japan properties, MPACT’s overall portfolio achieved a positive rental reversion of 3.6%.

Lease Expiry

Lease expiry remained well-staggered. The weighted average lease expiry (WALE) was 2.2 years for the retail segment and 2.3 years for the office/business park segment, resulting in an overall portfolio WALE of 2.2 years.

MPACT Share Price and Dividend Yield

Based on MPACT’s FY24/25 full year distribution of 8.02 cents and current share price of S$1.23, this translates to a high current dividend yield of 6.52%.

Summary of MPACT 4QFY24/25 Financial Results

The above information may be overwhelming for you. As usual, let me summarize the pros and cons of MPACT.

The pros are:

- Property expenses and net finance costs improved by 4.9% and 9.4% year-on-year respectively attributed to the divestment of Mapletree Anson.

- Gearing remained healthy at 37.7%.

- Positive rental reversion of 3.6%.

- Lease expiry remained well-staggered.

- Acceptable current dividend yield of 6.52% based on S$1.23 per unit.

The cons are:

- Gross revenue was 6.8% lower year-on-year.

- Lower overseas contributions.

- DPU fell 14.8% year-on-year to 2.00 cents. Full year DPU fell 10.0% to 8.02 cents.

- Overall portfolio occupancy fell to 89.6%, dragged down by overseas properties such as China and Japan.

Since 1QFY24/25, MPACT continued to face headwinds due to its underperforming oversea assets.