On 13th August 2024, CICT (CapitaLand Integrated Commercial Trust) released their 1H2024 financial results. As an existing unitholder, I am happy to know that CICT’s 1H2024 distribution per unit (DPU) rose 2.5% to 5.43 cents.

Are you familiar with CICT (CapitaLand Integrated Commercial Trust)? The REIT owns and invests in assets primarily used for commercial (including retail and/or office) purpose, located predominantly in Singapore. CICT’s portfolio comprises of 21 properties in Singapore, 2 properties in Frankfurt, Germany, and 3 properties in Sydney, Australia.

Let us take a deeper look into CICT’s 1H2024 financial results below to see how the trust has performed.

CICT 1H2024 Financial Results

In 1H 2024, Gross Revenue grew 2.2% year-on-year to S$792.0 million due to higher gross rental income. However, this was partially offset by the absence of income from Gallileo which has been undergoing an asset enhancement initiative (AEI) since February 2024.

Asset Enhancement Initiative (AEI) refers to the process of improving and upgrading the value, functionality, and attractiveness of a real estate asset. The manager renovates the properties, keeping them up to date with modern designs or reconfiguring them for different commercial uses. By doing so, they enhance rental income potential and increase property value.

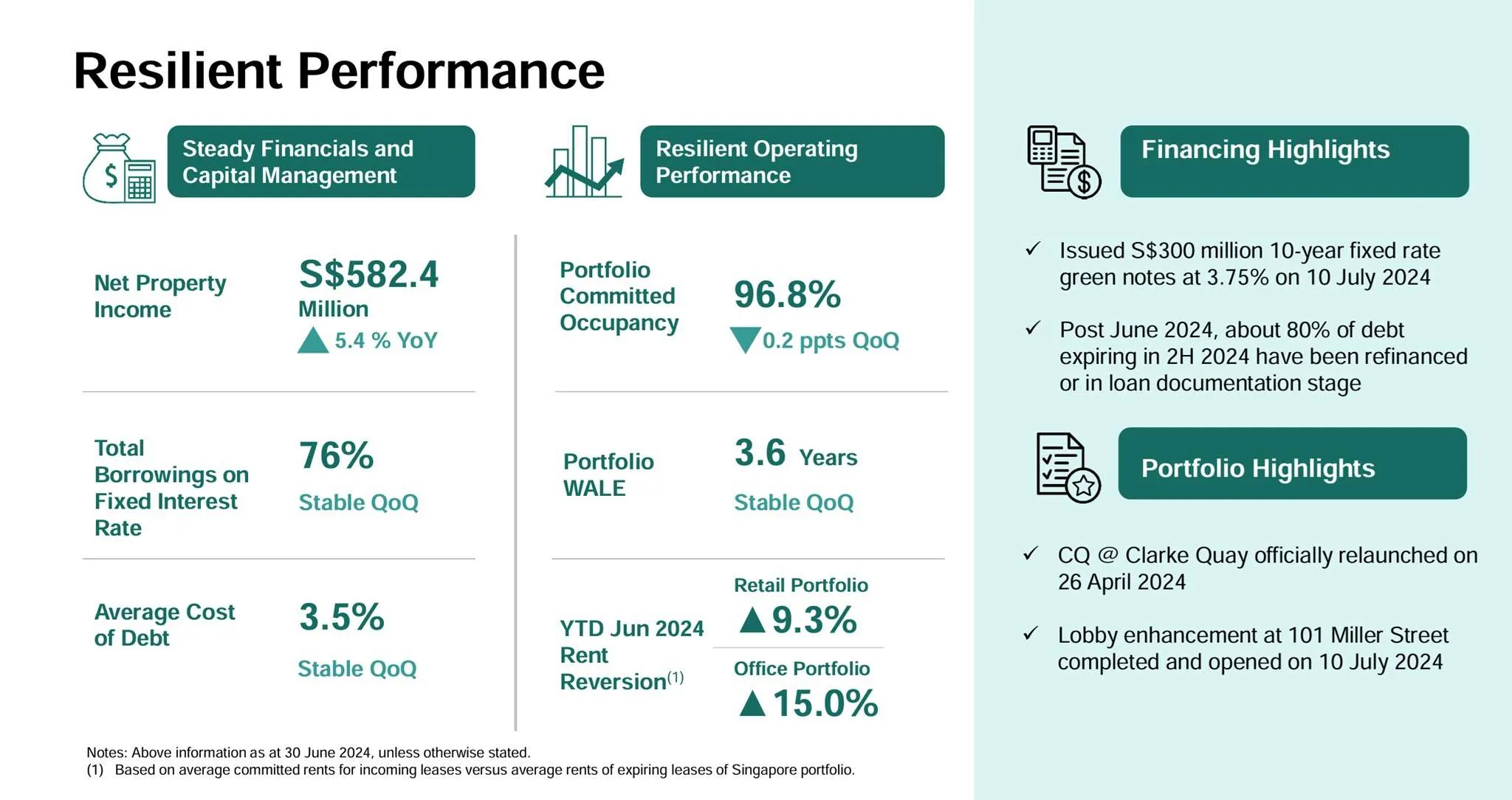

Net Property Income (NPI) also rose 5.4% year-on-year to S$582.4 million. This was mainly due to lower utility expenses and savings from property management reimbursements under the new property management agreement.

Distributable income increased 3.7% year-on-year as compared to the S$353.2 million for 1H 2023. Similarly, distribution per unit (DPU) rose 2.5% to 5.43 cents.

| 1H2024 (S$’000) |

1H2023 (S$’000) |

Change (%) | |

| Gross Revenue | 791,961 | 774,777 | 2.2% |

| Net Property Income | 582,364 | 552,337 | 5.4% |

| Amount Available for Distribution |

370,704 | 358,983 | 3.3% |

| Distributable Income |

366,479 | 353,245 | 3.7% |

| Distribution Per Unit (“DPU”) (cents) | 5.43 | 5.30 | 2.5% |

Debt

As of 30th June 2024, CICT’s aggregate leverage stood slightly below my threshold of 40% at 39.8%. Aggregate Leverage is also known as “gearing” and is a financial ratio used to assess a company’s reliance on debt. CICT’s aggregate leverage indicates how much debt a REIT holds relative to its property value.

Average cost of debt remained at 3.5%, with 76% of its total borrowings on fixed interest rates. Debt maturity profile is well-staggered across various tenures, with an average term-to-maturity of 3.5 years.

Occupancy

CICT’s overall portfolio occupancy stood healthy at 96.8%. Retail, office and integrated development portfolios recorded 99.0%, 95.3% and 98.8% occupancy rate respectively. The Singapore retail and office portfolios achieved positive rent reversions of 9.3% and 15.0% respectively, based on the average rent of signed leases in 1H 2024.

Asset enhancement initiatives at IMM Building (Retail) in Singapore and Gallileo (Office) in Germany are progressing well and are expected to complete in 2H 2025. Including leases under negotiation,

phases 1 and 2 of IMM Building’s AEI have achieved a high committed occupancy of 98.7%, while Gallileo’s committed occupancy stands at 96.7%.

As you can see from the above, lease expiries are well spread. The manager of CICIT shared that the majority of the leases expiring in 2024 are pending signing of agreements.

CICT Share Price and Current Dividend Yield

CICT’s share price closed at S$2.11 on Friday, 16th August 2024. As you can see from the above chart, CICT share price was on an uptrend since July. Based on CICT’s share price of S$2.11 on FY23 full year DPU of 10.75 cents, this translates to a current dividend yield of 5.09%.

Summary of CICT 1H2024 Financial Results

Based on the above financial results, let me summarize the pros and cons if you are planning to invest in CICT (CapitaLand Integrated Commercial Trust). The pros are:

- Gross Revenue grew 2.2% year-on-year to S$792.0 million.

- Net Property Income (NPI) also rose 5.4% year-on-year to S$582.4 million.

- Distributable income increased 3.7% year-on-year.

- Distribution per unit (DPU) rose 2.5% to 5.43 cents.

- 76% of its total borrowings on fixed interest rates to mitigate against sudden interest rate hikes.

- Overall portfolio occupancy stood healthy at 96.8%.

- Singapore retail and office portfolios achieved positive rent reversions of 9.3% and 15.0% respectively.

- Lease expiries are well spread.

- Current dividend yield of 5.09%.

The cons are:

- Aggregate leverage still remained high at 39.8%.

I would like to end this post by sharing my thought on what will be the catalyst for CICT. In my opinion, the catalyst will be the continued increase in shopper traffic and the positive rent reversions.

Why is positive rental reversion important? Positive rental reversions mean that there is an estimated increase in rent upon lease renewal, especially when the existing gross rent is below the estimated rental value. Positive rental reversions contribute to improved income and stability.

Comment below if you can think of other potential catalysts for CICT to increase their DPU.