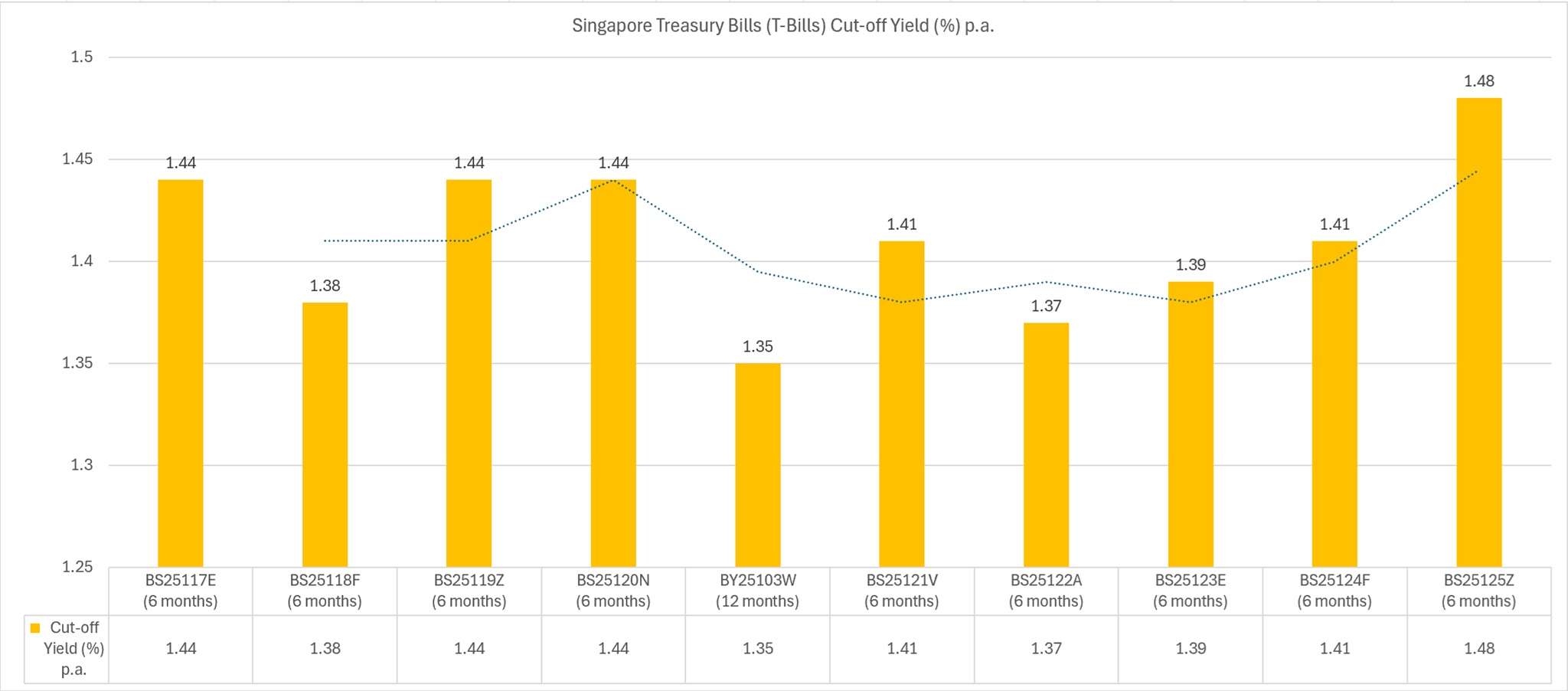

The latest Singapore 6‑Month Treasury Bill (T‑bill) auction, issued under the code BS25125Z, has drawn significant attention from investors looking for safe, short‑term returns. With global interest rates shifting and local fixed deposit promotions fluctuating, many Singaporeans have been watching T‑bill yields closely to decide where to park their cash. The December auction delivered a pleasant surprise. The cut‑off yield rose to 1.48% per annum, the highest in recent months. For a short‑term, government‑backed instrument, this is a meaningful bump, especially for those using CPF or SRS funds.

The latest Singapore 6‑Month Treasury Bill (T‑bill) auction, issued under the code BS25125Z, has drawn significant attention from investors looking for safe, short‑term returns. With global interest rates shifting and local fixed deposit promotions fluctuating, many Singaporeans have been watching T‑bill yields closely to decide where to park their cash. The December auction delivered a pleasant surprise. The cut‑off yield rose to 1.48% per annum, the highest in recent months. For a short‑term, government‑backed instrument, this is a meaningful bump, especially for those using CPF or SRS funds.

Do you know what are Singapore Treasury Bills? Singapore Treasury Bills are short-term debt instruments issued by the Singapore government to raise funds for its financing needs. These bills are typically sold at a discount from their face value and mature in 3, 6, or 12 months. They are considered a safe investment as they are backed by the Singapore government’s creditworthiness.

Investors can purchase these bills directly from the Singapore government or through designated financial institutions. Treasury Bills are often used by investors as a low-risk, liquid investment option with a fixed return.

In this article, I will break down the results of the BS25125Z auction, explore why yields have risen, and share why I personally invested S$10,000 of my SRS funds into this tranche. If you are evaluating whether T‑bills still make sense in today’s environment, this deep dive will help you understand the dynamics behind the numbers.

The auction for BS25125Z took place on 18th December 2025, with the issue date on 23rd December 2025 and maturity on 23rd June 2026. The headline figure was the cut‑off yield of 1.48%, a noticeable increase from the previous 6‑month T‑bill’s 1.41%. This upward movement reflects shifting demand and market expectations, and it has made this tranche particularly attractive for investors seeking stability.

The total amount of applications reached S$14.9 billion, lower than the S$16.3 billion submitted in the previous auction. With S$7.9 billion issued, the bid‑to‑cover ratio came in at 1.88, also lower than the earlier 2.03 ratio. Lower demand often translates into higher yields, and that dynamic played out clearly here.

Non‑competitive bidders enjoyed full allocation, as the total non‑competitive applications of S$1.4 billion fell within the allowable limit. Competitive bidders who bid exactly at the cut‑off yield of 1.48% received around 73% allocation, while those who bid below the cut‑off received full allotment.

The median yield came in at 1.37%, and the average yield at 1.27%, both higher than the previous auction’s figures. This suggests that investors were collectively pricing in higher short‑term rates, which aligns with the recent bounce in government bond yields observed in the weeks leading up to the auction.

Why the Yield Rose to 1.48%

The rise in yield for BS25125Z can be attributed to several factors, but the most immediate driver was the decline in demand. Total applications fell by more than S$1.4 billion compared to the previous auction, and competitive bids dropped as well. When demand softens, yields naturally rise to attract buyers.

Another factor is the broader movement in the Singapore Government Securities (SGS) market. The 6‑month SGS benchmark yield had climbed to 1.46% in the days leading up to the auction, up from 1.39% earlier in the week. T‑bill yields tend to track these benchmark rates closely, and the 1.48% cut‑off reflects this upward trend.

Market sentiment also plays a role. With global central banks signalling a more cautious stance and inflation stabilising, short‑term yields have been adjusting accordingly. Investors may also be shifting funds into other instruments, such as fixed deposits or money market funds, which can temporarily reduce T‑bill demand and push yields higher.

Why I Invested S$10,000 Using My SRS Funds

For this auction, I decided to invest S$10,000 using my SRS (Supplementary Retirement Scheme) funds. T‑bills have long been one of the most efficient ways to deploy SRS balances, especially when yields are attractive. Since SRS funds earn a negligible default interest rate, leaving them idle is rarely optimal. A 6‑month T‑bill at 1.48% offers a safe, government‑backed return that is significantly better than the alternative.

The short maturity period also fits well with my SRS strategy. I prefer to keep my SRS funds relatively liquid so I can reinvest them into future T‑bill auctions or other opportunities that may arise. A 6‑month duration strikes the right balance between yield and flexibility.

Another reason I chose to invest in this tranche is the stability of T‑bills. Unlike market‑linked products, T‑bills are not subject to price volatility once held to maturity. The return is fixed, predictable, and backed by the Singapore Government. In a period where global markets remain uncertain, this level of safety is valuable.

Finally, the rising yield trend made this auction particularly appealing. With the cut‑off yield climbing from 1.41% to 1.48%, it signalled improving returns for short‑term government securities. While yields can fluctuate, locking in a higher rate now ensures that my SRS funds are working harder for the next six months.

How BS25125Z Compares to Other Options

When evaluating T‑bills, it is natural to compare them with alternatives such as fixed deposits, money market funds, and high‑yield savings accounts. According to market commentary, the median and cut‑off yields for BS25125Z were higher than the best 6‑month fixed deposit rates available at the time. This reinforces the value proposition of T‑bills, especially for investors who prioritise safety and guaranteed returns.

Money market funds remain competitive, but they carry slight fluctuations in daily NAV and do not offer the same certainty of return as a T‑bill held to maturity. High‑yield savings accounts can be attractive, but their promotional rates often come with conditions such as salary crediting or minimum spending.

In contrast, T‑bills require no such commitments. You simply apply, get your allocation, and wait for maturity.

My Thoughts on BS25125Z 6-Month T-bill

The Singapore 6‑Month T‑bill BS25125Z stands out as one of the more attractive short‑term government securities issued in recent months. With a cut‑off yield of 1.48%, full allocation for non‑competitive bidders, and a favourable demand‑supply dynamic, this tranche offered a compelling opportunity for investors seeking stability and predictable returns.

For me, investing S$10,000 of my SRS funds into this T‑bill was a straightforward decision. The yield was strong, the risk was minimal, and the 6‑month duration aligned perfectly with my SRS strategy. As yields continue to fluctuate, I will be watching upcoming auctions closely to see whether this upward trend continues.

If you are considering where to park your cash or SRS funds next, the T‑bill market remains one of the most reliable and transparent options available. With each auction offering fresh insights into investor sentiment and market conditions, staying informed can help you make smarter, more confident financial decisions.