Alibaba has released its financial results for the quarter ended 31st December 2025, offering one of the clearest snapshots yet of how the company is reshaping itself around artificial intelligence, cloud computing, and a more disciplined approach to its sprawling commerce ecosystem. While headline revenue growth was modest, the underlying story is far more dynamic: a company leaning aggressively into AI infrastructure, rebuilding its commerce engines for efficiency, and navigating the financial impact of strategic divestments and reinvestments.

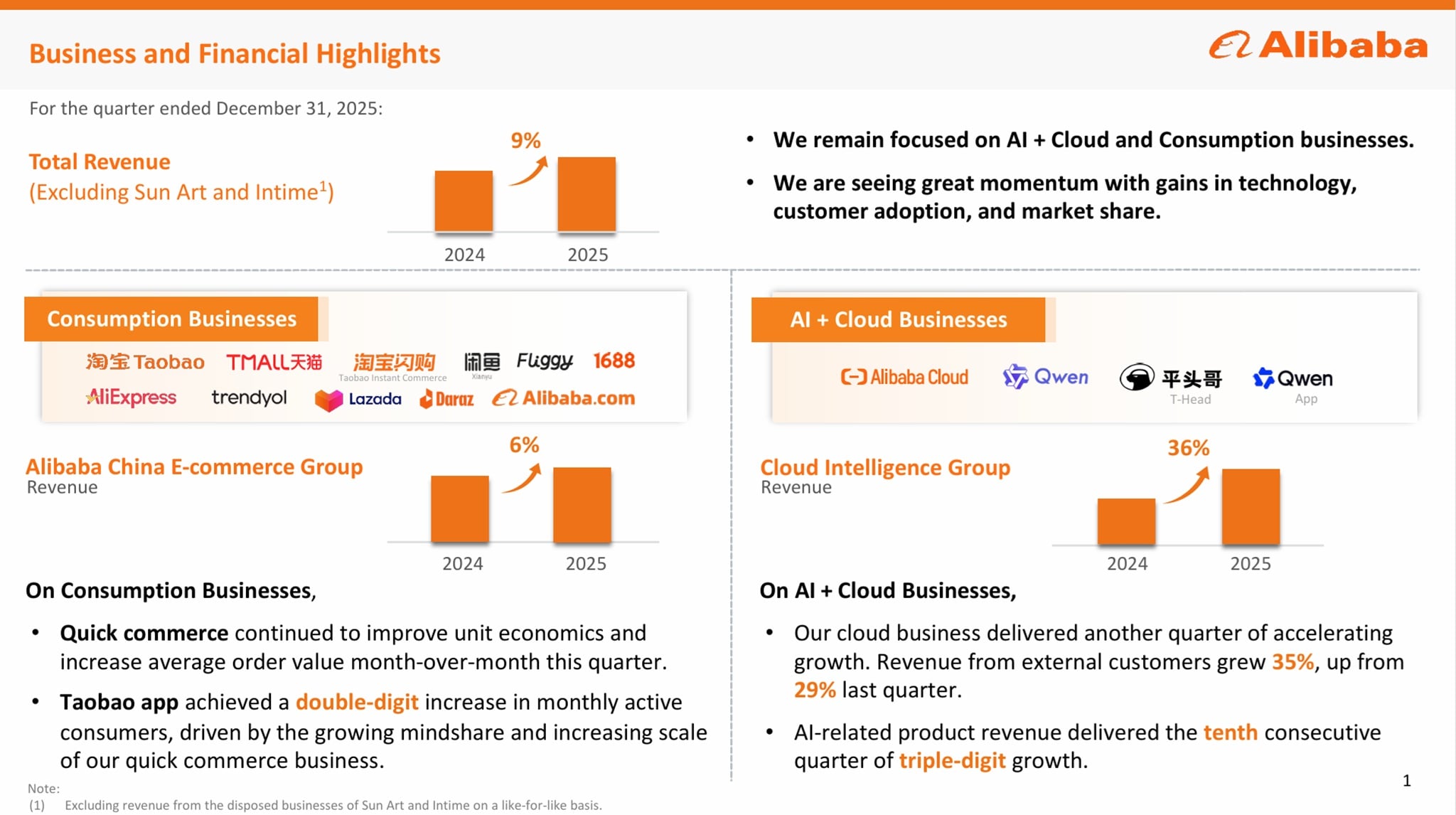

The quarter’s consolidated revenue reached RMB284,843 million, a year‑over‑year increase of 2%. Although this top‑line growth appears muted, it reflects a period of transition marked by the disposal of Sun Art and Intime, a slowdown in certain commerce segments, and a surge in AI‑driven cloud demand. The company’s own commentary underscores this shift, noting that it remains “focused on AI + Cloud and Consumption businesses,” with momentum visible in technology adoption and market share gains.

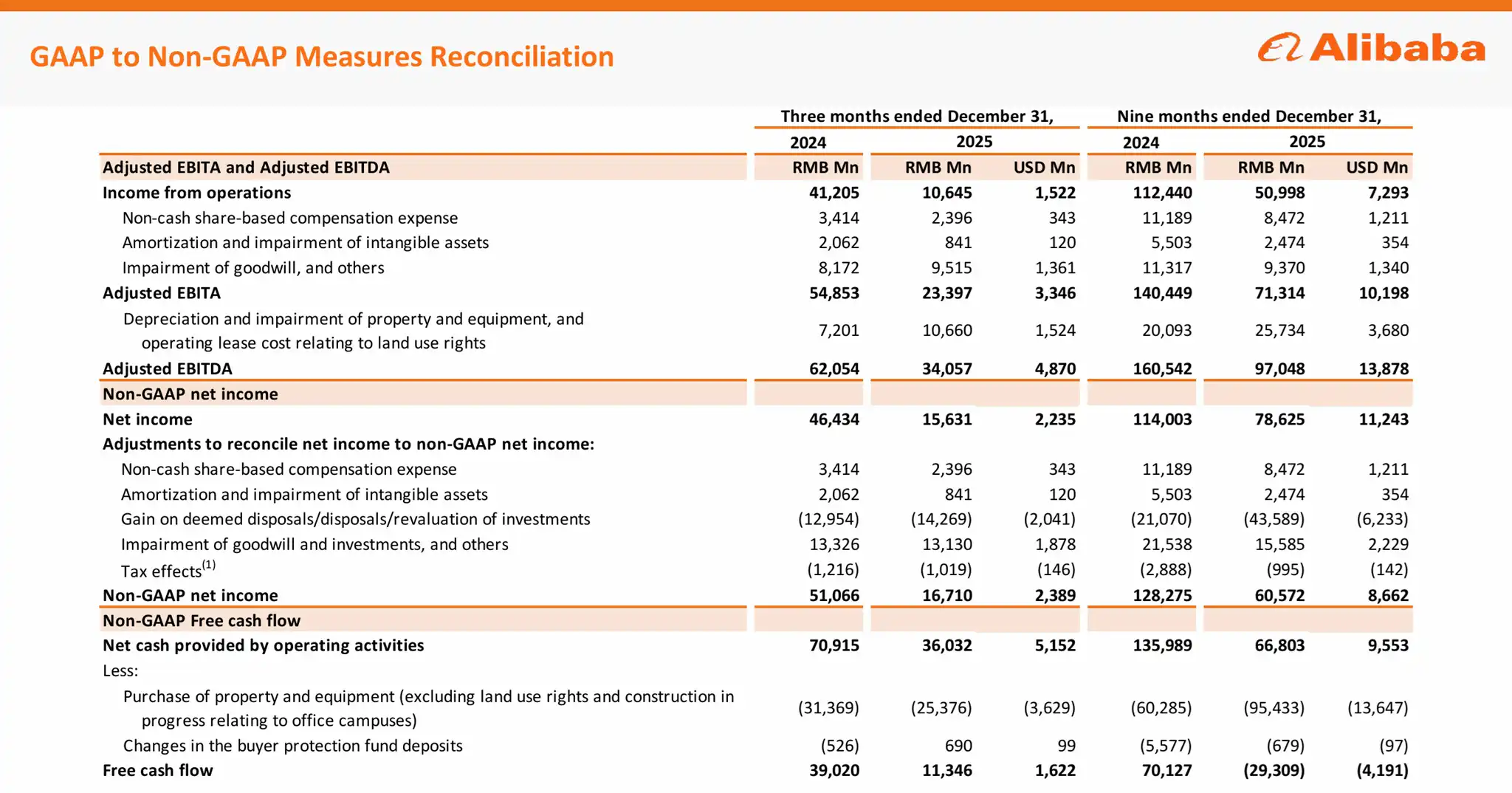

Yet profitability tells a more challenging story. Income from operations fell sharply to RMB10,645 million, a 74% decline from the previous year. Net income also dropped 66% to RMB15,631 million. The decline is tied to heavier investments in quick commerce, technology, and AI infrastructure, as well as the absence of gains from divested assets that had previously boosted results. As the report states, adjusted EBITA for the quarter fell 57% to RMB23,397 million, reflecting the cost of building the next phase of Alibaba’s growth engine.

Still, beneath these headline declines lies a company undergoing a deliberate strategic pivot, one that is beginning to show signs of traction, especially in cloud and AI.

Cloud Intelligence Group: The New Growth Engine

The standout performer of the quarter was Alibaba’s Cloud Intelligence Group. Revenue surged 36% year‑over‑year to RMB43,284 million, marking an acceleration from previous quarters. The company highlights that revenue from external customers grew 35%, up from 29% in the prior quarter, underscoring rising demand for public cloud and AI‑related services.

One line from the report captures the momentum clearly: “AI‑related product revenue delivered the tenth consecutive quarter of triple‑digit growth.” This is a remarkable streak, and it reflects Alibaba’s deepening integration of AI across its cloud offerings from model training and inference services to distributed storage, networking, and cloud operating systems.

Alibaba Cloud’s leadership position in China remains intact. The company notes that it has been named a Leader in the Gartner Magic Quadrant for Cloud Database Management Systems for six consecutive years. It also maintains the top spot in China’s financial cloud market with a 43% share, according to IDC. These recognitions reinforce Alibaba’s strategic advantage: a full‑stack AI cloud ecosystem that spans chips, models, infrastructure, and applications.

The launch of Alibaba Cloud Linux, a next‑generation AI infrastructure operating system capable of supporting trillion‑parameter model training, signals the company’s ambition to compete at the frontier of global AI infrastructure. Meanwhile, the expansion to 92 availability zones across 29 regions highlights its continued push for international relevance.

Adjusted EBITA for the cloud segment rose 25% to RMB3,911 million, driven by scale efficiencies and revenue growth, though partially offset by continued investments in customer acquisition and technology innovation. The cloud business is clearly becoming the company’s most important long‑term profit engine.

Qwen, T‑Head, and the Rise of Alibaba’s AI Ecosystem

Alibaba’s AI strategy is anchored by the Qwen model family, which the company describes as “the world’s most widely used open‑source model family,” surpassing one billion cumulative downloads on Hugging Face. The launch of Qwen3.5 in February marks another leap in multimodal reasoning, coding, and agentic task execution. The report emphasizes that Qwen3.5 delivers “higher inference efficiency and broader global accessibility,” positioning Alibaba as a serious competitor in the global open‑source AI landscape.

The integration of Qwen into real‑world applications is accelerating. The Qwen app, powered by Qwen3.5, has become a flagship consumer AI product. On January 15, 2026, Alibaba announced a major upgrade that deeply integrates the app with Taobao, Tmall, Taobao Instant Commerce, Amap, Fliggy, and Alipay. This integration transforms the app into what Alibaba calls “the first AI assistant capable of executing large‑scale, real‑world complex tasks in China.”

The results have been immediate. By the end of February, approximately 140 million users had experienced AI‑driven shopping through the Qwen app, and monthly active users surpassed 300 million across platforms. This level of adoption suggests that Alibaba’s AI strategy is not merely theoretical, it is reshaping consumer behaviour at scale.

T‑Head, Alibaba’s chip design subsidiary, is another pillar of this ecosystem. Its proprietary GPU has entered mass production, supporting end‑to‑end AI workloads. By combining T‑Head’s hardware with Qwen models and Alibaba Cloud, the company is building a vertically integrated AI stack that could significantly reduce long‑term infrastructure costs while enhancing performance.

China E‑commerce: Stabilizing the Core While Investing in Quick Commerce

Alibaba’s China commerce segment remains its largest revenue contributor, generating RMB159,347 million in the quarter, a 6% increase year‑over‑year. Within this segment, the traditional e‑commerce business grew just 1%, reflecting a mature market and softer transaction activity. Customer management revenue also grew 1%, reaching RMB102,664 million. The report attributes the slowdown to “weaker transaction activities and phase‑out of the impact of software service fee implementation.”

However, the bright spot is quick commerce. Revenue from this segment surged 56% to RMB20,842 million, driven by the rollout of Taobao Instant Commerce, the rebranded Ele.me platform. Alibaba notes that the quick commerce business “continued to improve unit economics and increase average order value month‑over‑month,” supported by logistics efficiency and strong customer retention.

The Taobao app itself saw a double‑digit increase in monthly active consumers, fuelled by the growing mindshare of quick commerce. Meanwhile, the 88VIP membership base surpassed 59 million, continuing its double‑digit growth trajectory. This high‑spending cohort remains a critical pillar of Alibaba’s consumer ecosystem.

Despite these operational improvements, adjusted EBITA for the China commerce segment fell 43% to RMB34,613 million. The decline reflects heavy investment in quick commerce, user experience, and technology investments that Alibaba views as essential to long‑term competitiveness.

International Commerce: Narrowing Losses and Expanding Global Reach

Alibaba International Digital Commerce Group (AIDC) delivered RMB39,201 million in revenue, a 4% increase from the previous year. Retail commerce revenue grew 3%, while wholesale commerce revenue rose 10%, driven by cross‑border value‑added services.

The most encouraging development is the significant narrowing of losses. Adjusted EBITA improved from a loss of RMB4,952 million to a loss of RMB2,016 million, a 59% improvement. The report attributes this to “logistics optimization and investment efficiency enhancement,” as well as improved unit economics in AliExpress’ Choice business.

AIDC is also expanding its global product offerings. The joint venture with Shinsegae in South Korea has broadened to include distribution of Korean products across Lazada and other platforms. Meanwhile, AliExpress’ Brand+ program accelerated brand onboarding and delivered substantial quarter‑over‑quarter sales growth.

All Others: Impact of Divestments and Technology Investments

The All Others segment saw revenue decline 25% to RMB67,340 million, primarily due to the disposal of Sun Art and Intime, as well as lower revenue from Cainiao. This was partially offset by growth in Freshippo and Alibaba Health. Adjusted EBITA losses widened to RMB9,792 million, driven by increased investment in technology businesses, though results improved for Cainiao and Hujing Digital Media.

Cash Flow and Balance Sheet: A More Conservative Financial Posture

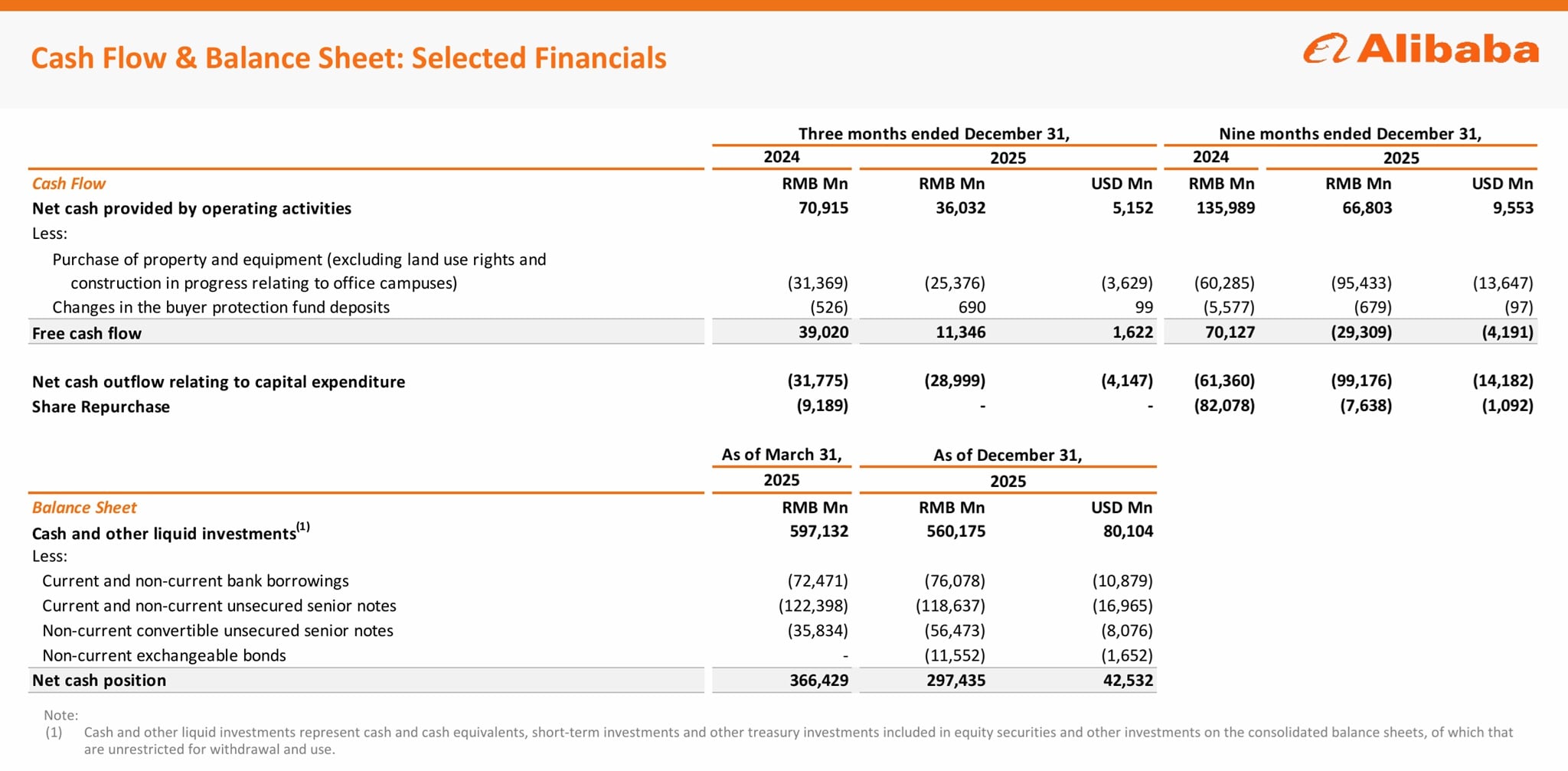

Operating cash flow for the quarter fell to RMB36,032 million from RMB70,915 million a year earlier. Free cash flow dropped to RMB11,346 million, reflecting higher capital expenditure and lower operating cash generation. For the nine‑month period, free cash flow turned negative at RMB29,309 million, compared to a positive RMB70,127 million the previous year.

Alibaba’s net cash position declined to RMB297,435 million from RMB366,429 million as of 31st March 2025. The company continues to maintain a strong liquidity base with RMB560,175 million in cash and liquid investments, though borrowings and senior notes remain substantial.

Share repurchases slowed significantly, with no buybacks recorded in the quarter compared to RMB9,189 million in the same period last year.

A Company in Strategic Transformation

Alibaba’s December quarter results reflect a company in the midst of a profound transformation. Revenue growth is modest, and profitability has compressed sharply. Yet these numbers mask the deeper strategic shift underway: a pivot toward AI, cloud infrastructure, and next‑generation commerce experiences.

The cloud and AI businesses are scaling rapidly, with triple‑digit AI product growth and accelerating cloud revenue. The Qwen ecosystem is gaining real‑world traction at a pace few expected. Quick commerce is becoming a major growth engine, even as it weighs on short‑term profitability. International commerce is becoming more efficient and more globally integrated.

Alibaba is trading short‑term margin pressure for long‑term strategic positioning. The company is building the infrastructure, models, chips, and applications that will define the next decade of digital commerce and AI‑driven consumer experiences.

The numbers tell a story of transition. The narrative behind them tells a story of reinvention.