![]()

On 26 April 2018, Starhill Global REIT has released a set of disappointing 3QFY17/FY18 results. Gross Revenue, Net Property Income (“NPI”), Distributable Income and Distribution Per Unit (“DPU”) has all declined.

Despite the fact that distributable income has declined by 6.3%, the manager retained $1.6 million for working capital purposes, worsening the income to be distributed to unit holders. Distribution Per Unit (“DPU”) fell by 7.6%. This was unexpected of a Retail/Office REIT.

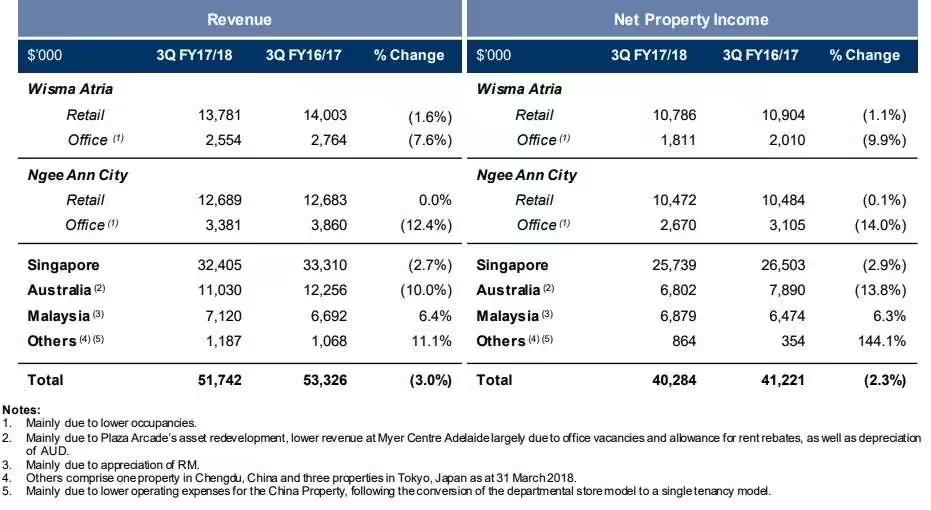

| 3QFY17/18 | 3QFY16/17 | Change | |

| Gross Revenue | $51.7 mil | $53.3 mil | (3.0%) |

| Net Property Income | $40.3 mil | $41.2 mil | (2.3%) |

| Distributable Income | $25.4 | $27.1 mil | (6.3%) |

| Income to be Distributed to Unitholders | $23.8 mil | $25.7 mil | (7.6%) |

| Distribution Per Unit (“DPU”) (cents) | 1.09 | 1.18 | (7.6%) |

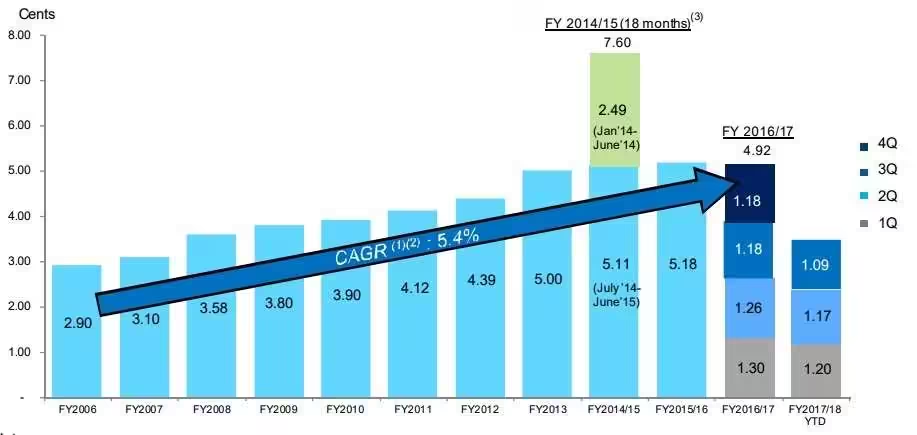

Distribution Per Unit

Comparing the Distribution Per Unit side by side between FY2016/17 and FY2017/18, we can see that DPU has declined quarter on quarter. Assuming the best scenario that Starhill Global REIT can maintain its DPU of 1.18 in 4QFY2017/18, the total DPU for FY2017/18 will be 4.64 cents. I am expecting the DPU for 4QFY2017/18 to be 1.09 cents which will make up a total DPU of 4.55 cents for FY2017/18.

Dividend Yield

Assuming Starhill Global REIT manages to pay out 4.55 cents for FY2017/18, based on the current price of S$0.72, this translates to an estimated projected dividend yield of 6.32%.

Where Is The Decline?

A picture speaks more than a thousand words. As we can see from the above, the office assets are not doing so well. Both revenue from the office segment for Wisma Atria and Ngee Ann City declined by 7.6% and 12.4% respectively. Revenue was lower at Myer Centre Adelaide (Australia) largely due to office

vacancies and allowance for rent rebates, as well as the depreciation of AUD against SGD. Impact of the office portfolio in Australia is small given it accounts for just 2.4% of the Australia portfolio’s revenue in 3Q FY17/18.

Positives That Can Help in Starhill Global REIT Recovery

- Handover of premises to anchor tenant UNIQLO who has commenced renovation works, with completion targeted in 2H 2018. Plaza Arcade’s revenue contribution is expected to improve with the completion of the asset redevelopment.

- Malaysia’s Starhill Gallery and Lot 10 property rejuvenation completed. The mall has created a new entry point for Lot 10 from the new MRT station exit which may improve shopper’s traffic to the mall.

- New anchor tenant Markor International Home Furnishings Co Ltd for its Chengdu Property which commenced operation on 28 March 2018.

Conclusion

I feel that the above positives are not strong enough to give Starhill Global REIT a boost in its earnings. Given the next rental review for Toshin is in June 2019, there is no catalyst at the moment for Starhill Global REIT. I am concern also about its office rent expiry for both Wisma Atria and Ngee Ann City in FY18/19 which is high at 27.1% and 40.7% respectively.

It is difficult to predict the bottom and there is a possibility Starhill Global REIT’s share price can go below $0.70. However, I believe Starhill Global REIT should be able to maintain its dividend yield of above 6% given the worst case scenario for its DPU I have assumed above.

Hi thanks for the analysis. I’m not sure why they are holding back $1.6M but based on the Annual Reports, seems like the staff were not paid performance bonus since 2016. Is it because they have been underperforming? Plus, Cortina pulling out is definitely not a good sign…

Hi K, if the REIT is not performing, I guess the staff does not deserve a performance bonus. Cortina is in the luxury watch business. I held The Hour Glass which is similar in nature. In my personal opinion, the luxury spending segment has not yet recovered to its prime and its hard for the company to maintain its physical stores when nobody is buying luxury watches. Probably that might be the reason for Cortina to be pulling out?

Losing one of the anchor tenants…selling assets but holding on to the cash…fat salary but no performance bonus…all these are signs of an incompetent management…

Hi

Thanks for replying to my comment. Do you see it making a comeback anytime soon?

Thanks

Hi K, in my opinion probably not in the next few quarters.

Already assume dividend to by 4.55 cents. The AEI will not be able to cover the continue drop in DPU. Qn is when will the leak stop? Luckily I am still in small green after getting rid of it today. Think better to get a more stable reit with slightly lower yield like CMT is better

Hi Layers, thanks for sharing. Yes, I already held CMT in my stock portfolio. A better and stable choice is CMT right now.