When I wrote about SPH Reit two years ago, SPH Reit only has two assets in its portfolio which are Paragon and The Clementi Mall. Back then, there was news that SPH Reit will add Seletar Mall to its portfolio but till date, it has not actualize. As of today, SPH Reit has include two new properties in its portfolio, which is The Rail Mall and Figtree Grove Shopping Centre.

The Rail Mall

SPH Reit acquired The Rail Mall on 28th June 2018 at S$63.2 million. Based on what I have gathered, 40% of the tenants are F&B restaurant operators, 20%are supermarkets and the rest consist of services providers such as spa and massage parlours and tuition centres.

The Rail Mall has 41.5% of its leases expiring in FY19.

Figtree Grove Shopping Centre

SPH Reit acquired Figtree Grove Shopping Centre on 21st Deccember 2018 at a purchase consideration of A$206.0 million. The shopping centre consists of a strong and tailored mix of non-discretionary and service-based retailers. Major anchor tenants include a 24-hour Kmart, Coles and Woolworths supermarkets.

Gross Revenue

Based on the 1QFY19 financial results presentation, we can see that the majority of the Reit’s gross revenue comes from Paragon, followed by The Clementi Mall. Revenue from The Rail Mall at this point in time looks insignificant.

Rental Reversions

Rental reversion is one of key indicators investors look at to assess the health of leasing activity of the Reits. Negative rental reversion rates mean that new tenants are paying less than older tenants. Positive rental reversion rates mean that new tenants are paying more rent than older tenants which is good news for Reits as this translates to higher gross revenue.

Based on the 1QFY19 financial results, Paragon delivered a positive rental reversions of 10.1%. This was the mall’s first positive rental uplift since 9MFY17.

The Clementi Mall and The Rail Mall rental reversions were 4.5% and 7.9% respectively.

Debt

Gearing currently stood approximately at 30% post acquisition of Figtree Grove Shopping Centre. I still consider this ratio relatively low as compared to other retail Reits. Thus, I believe SPH Reit still have room for further acquisitions.

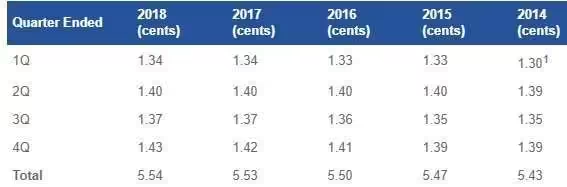

Dividend Yield

Based on a distribution of 5.54 cents in FY2018 and the current price of S$1.03 (as of 22 Feb 2019), this translates to a dividend yield of 5.38%.

If we based on a share price of S$0.99 (22 Nov 2018), this translates to a dividend yield of 5.60%.

The annual distribution per unit (DPU) of Capitamall Trust is 11.86 cents and based on the share price of S$2.44 (22 Feb 2019), this translates to a dividend yield of 4.86%. Thus, at this moment, it will make more sense to invest in SPH Reit if you are looking into buying Retails Reits.

Catalyst

If you have followed the news, you would have read about the major revamp of Orchard Road jointly by Singapore Tourism Board (STB), Urban Redevelopment Authority (URA) and National Parks Board (NParks).

There will be a one year trial by Orchard Road Business Association (Orba) to organize activities such as retail and food and beverage pop-ups and arts and entertainment events to the pedestrian walkways along the street.

Such major revamp could give retail REITs that have assets in Orchard road such as SPH Reit and Starhill Global Reit a boost.