![]()

This is my first personal analysis for the year 2018. Silverlake Axis has always been on my watchlist. It is a complex company for me to analyse and with my limited knowledge, I decide to do my best in analyzing this company and hope to make the right decision on whether to dive into this stock.

Business Overview

Silverlake Axis is a Fintech company that was founded in 1989 with track records of core banking implementations. Silverlake Axis was listed on Singapore’s Stock Exchange (SGX) SESDAQ in 2003 and moved up to SGX Mainboard in 2011. The company call the core banking solution they have developed themselves “Silverlake Integrated Banking Solution” or SIBS in short. Although the strength of Silverlake Axis is in core banking, they have ventured into other business segments such as insurance, retail, payment and logistics. The main markets are in South East Asia, but Silverlake Axis also have customers in Japan, Sri Lanka, Central Europe, Middle East, Africa, Australia, and New Zealand.

Silverlake Axis classified their businesses into the following categories. This is also how they classified their revenue which I shall drill deeper in the next section.

- Software licensing

- Software project services

- Maintenance and enhancement services

- Sale of software and hardware products

- Credit and cards processing

- Insurance processing

Management

Mr Goh Peng Ooi was the founder and Group Executive Chairman for Silverlake Axis. A simple search reveals Mr Goh started his career in IBM Malaysia before leaving IBM in 1989 to set up Silverlake Axis. His last position with IBM was as a Marketing Manager for Banking and Finance Industry. I heard about Mr Goh’s craze about mathematics and having read his speech as Chairman, I got lost in his world of ‘mathematically Group Theory’, ‘sigma transformation’ and ‘collective intelligence’.

Dr. Kwong Yong Sin is the current Chief Executive Office (CEO) and Group Managing Director for Silverlake Axis. He started as a senior systems analyst in Pacific Power (Australia) before moving on to be Senior Manager and Head of IT Consulting for Coopers and Lybrand (South East Asia). It is noteworthy to know that he was also Partner/Vice President of Ernst & Young Global Consulting and Cap Gemini Ernst and Young for 11 years.

I am expecting either Silverlake Axis founder or CEO to be a banker in their previous positions but it turns out not be so. However, both Mr Goh and Dr Kwong have over 30 years of experience in Information Technology. Among Silverlake Axis’s Board of Directors, I noticed Mr Tan Sri Dato’ Dr Lin See Yan was the only banker. He was a professional banker for most of his professional life. Prof. Lin is also Malaysia’s first UK Chartered Statistician and he was advisor to all Prime Ministers and Finance Ministers of Malaysia. Impressive!

The company has been performing share buy back frequently which shows their confidence in the company.

Financial

Market Capitalization

Revenue

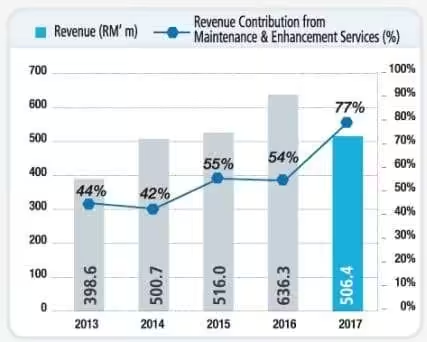

Found on Silverlake Axis website’s FAQ page, for FY2017, about 77% of Silverlake Axis’s revenue is derived from maintenance and enhancement services and 6% from insurance processing which are recurrent.

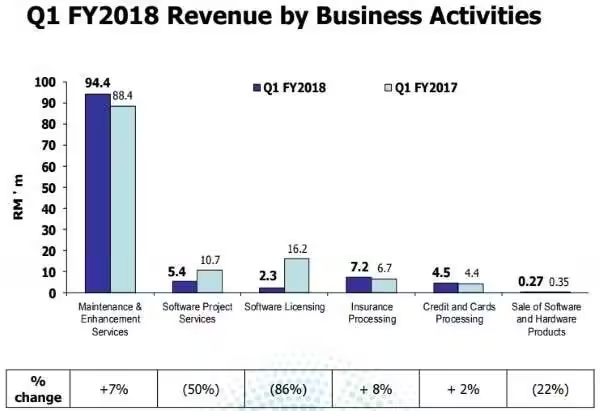

From the below, we can see that Revenue is up year on year however it fell 20% in 2017. Earnings are expected to be lumpy for companies such as Silverlake Axis whereby they engage in project based implementation work. This fact is validated by a quick glance of the revenue for Q1FY2018 where revenue declined 10% from RM 126.7 million to RM 114 million mainly due to lower contribution from project related revenue segments.

However, the revenue contribution from maintenance services cushion the impact during times where there are less projects implementation. 89% of the total revenue in 1QFY2018 is contributed by recurrent revenue segments.

Although net profit declined 81% from RM 168.7 million to RM 31.7 million, if we take away the one off gain of RM 143.7 million from the sale of GIT shares in Q12017 and taxes involved when comparing with Q12018 results, net profit of RM 31.7 million in Q1 FY2018 was 24% lower compared with the RM 41.6 million recorded in Q1 FY2017.

Cash Flow

As we can see, cash flow from operating activities is pretty lumpy with ups and downs. Cash flow improved slightly in FY2017. This reflects improved collection from customers.

| RM$’m | FY2013 | FY2014 | FY2015 | FY2016 | FY2017 |

| Net cash generated from operating activities | 184.0 | 280.4 | 305.5 | 209.1 | 216.9 |

Debt

As of 30th September 2017, Silverlake Axis has a debt of RM$191 million. This can be easily paid off by their cash balance of RM$632 million.

Dividends

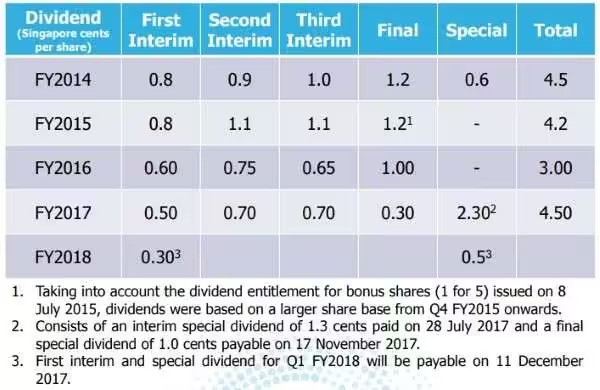

Silverlake Axis has a dividend policy to pay out not less than 40% of the Group’s net profit as dividends. Below is taken from the investors presentation slides which more or less summarizes the dividend payout over the past few years.

The total normal dividends paid in FY2017 is 2.2 cents. At the current stock price of S$0.58, this translates to a dividend yield of 3.79%. If we include the special dividend payout of 2.3 cents, this translates to a dividend yield of 7.76%.

Thus, the worst case if they maintain their normal dividend payout, we should be expecting at 3.5% to 3.79% dividend yield. The best case if they payout special dividends which makes up total dividends paid similar to FY2014, we should be expecting a yield of 7.76%.

Current Valuation

Based on FY17 annualized distribution of 4.5 cents and current price of $0.58, the dividend yield is 7.76%.

As of 30th September 2017, the earnings per share is 31.95 (sen). The Price to Earnings ratio (P/E) is estimated to be 6.6. I consider Silverlake Axis to be fairly valued at current price of S$0.58.

Strength and Catalyst

1. Over 40% of the Top 20 Largest Banks in South-East Asia run on SIBS.

2. Long Lasting Maintenance Contracts

3. Lucrative Licensing Model

4. Insurance Processing

Investment Risks

#1 Catching up with Technology

As Silverlake Axis is a technology company, they will need to frequently catch up with the fast paced technologies. Otherwise, they may be outpaced by their competitors. The risk can also be a catalyst for Silverlake Axis as existing customers look at technology upgrade to their SIBS system as well.

#2 Competitors

Oracle, TEMENOS, Infosys Technologies are some of the bigger giants that also provide core banking systems. Silverlake Axis has a strong presence in Southeast Asia however should the giants decided to expand into asia, this can pose a challenge for Silverlake Axis.

#3 Cut of spending in Technology by Financial Institutions

Silverlake Axis presented this graph on the spending on Technology in Asian FSIs. We can clearly see that FSIs are cutting down on spending from 2014 to 2017. This continues to impact Silverlake Axis where their main markets are in Southeast Asia.

#4 Technology Companies are Cylindrical in Nature

I considered Silverlake Axis as a Information Technology company. By nature, such stocks are cyclical in nature.

Conclusion

I will feel uncomfortable to enter into Silverlake Axis at current price of S$0.58 although it is considered fair valued. Another reason is that given technology stocks are cyclical in nature, earnings can be lumpy which also means the dividends may not always maintain at current yield. Given the short term weak earnings reported by Silverlake Axis, there is a possibility of special dividends being cut. Without special dividends, the dividend yield is less than 4%.

For such cyclical stock, I prefer more margin of safety. Thus, I shall be keeping Silverlake Axis in my watchlist and probably take a second look at it in the event the price hits S$0.48.

HI,

Thanks for the interesting analysis.

I am also not currently interested in investing in this company due to the declining numbers.

However I am not sure that if the directors of a company buy back shares on behalf of the company in the market, that this is a sign of confidence. Only if the directors are personally buying shares would it be such an indication.

In the States there has been a trend since Bernanke dropped the interest rates to almost zero for companies to borrow and buy back shares. Basically it has been cheaper to borrow money more cheaply than the cost of the dividends paid out. This results in a higher share price which is often very beneficial to the directors, who have share options and are also remunerated according to the share performance.

I think we would have to look more closely why the cash in SA is being used to buy back shares rather than invested in developing the company or being returned to the owners, namely the shareholders, as a special dividend.

It is certainly a question I would love to ask at the AGM.

My feeling is that in every case where the directors are authorising the buy back of company shares in the market, the directors themselves have a vested personal interest. There is one exception, and that is if there is an employee share purchase scheme and the company is required to deliver shares to the participating employees.

Have a great 2018!

Thanks Roman for sharing! Have a great 2018 too!

Do u mean cyclical company? Not sure what is ‘cylindrical’?

Also. Silverlake market cap is definitely not small. It’s at least s$1.5b, going by the number of shares stated above and market price of $0.58.

Hi Jacky, yes. Apologies for the typo. I meant “cyclical company”.

Are you sure the Market Cap is $191 million Ringgit?

Hi raj, thanks for spotting my mistake! The market cap is S$1.54 billion. It is a mid cap stock.

Roman

Your view on Director buying back shares on behalf of the co ,is a good point. Share price performance is one of the kpis to reward director performance. Managing the EPS with Company share buyback can have a positive effect on share price. Tks